Ahead of the Easter break, investors were handed an escalating Iran conflict, a US$122 billion AI mega-round, aluminium prices at four-year highs, a $29 billion food distribution deal the market hated, and a reminder that the Strait of Hormuz has no single off-switch.

All the top moves, shakes, and chocolate bunny flakes from Azzet's editorial team are right here in your weekly business wrap every Friday (4 April 2026).

The Strait of Hormuz has been shut for five weeks now, and the best idea anyone in Washington can come up with is threatening to seize an Iranian oil island while simultaneously granting Moscow a sanctions waiver to sell more crude.

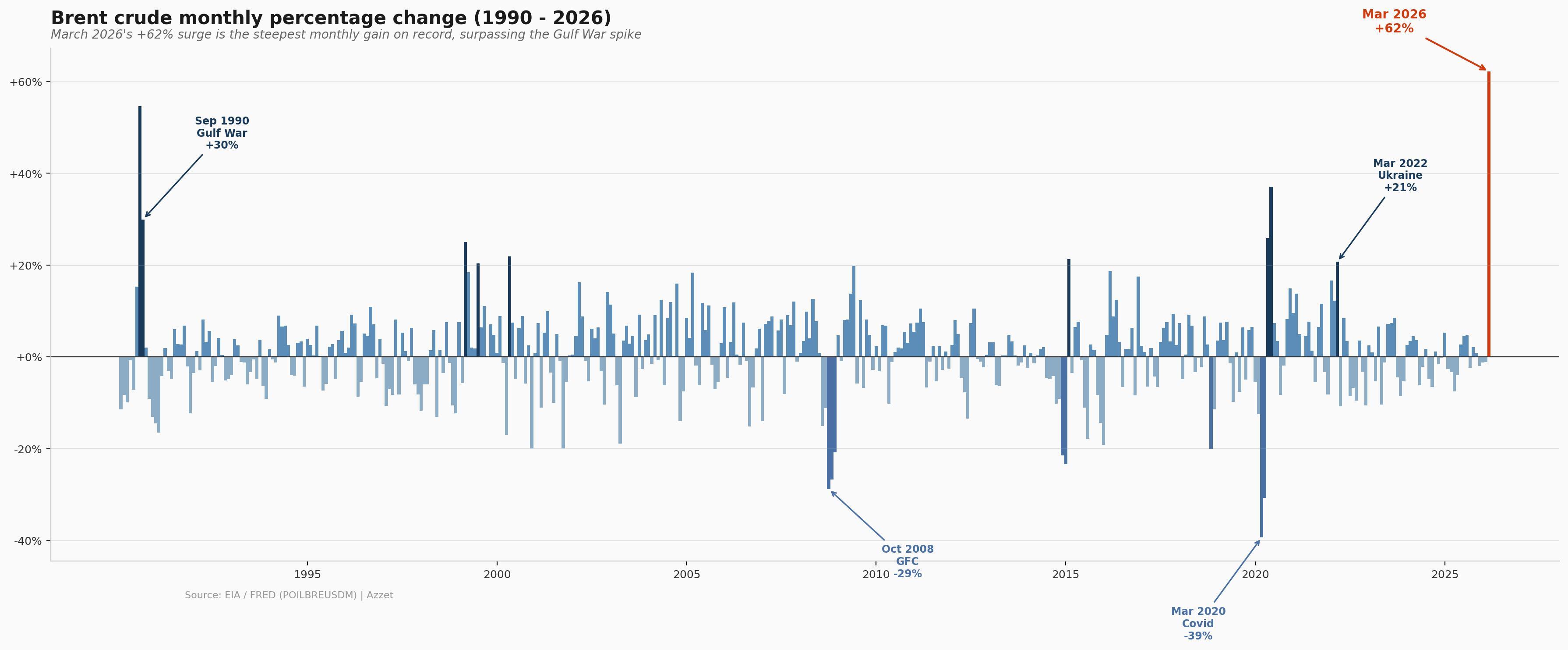

Subsequently, Brent Crude posted its steepest monthly gain on record during March.

The IEA logged an 8-million-barrel-per-day supply loss - worse, by its own assessment, than anything the oil market has previously recorded.

Gulf aluminium smelters took direct hits from Iranian strikes, and U.S. consumer sentiment slid to a three-month low.

None of which stopped OpenAI from raising $122 billion at an $852 billion valuation without ever having turned a profit, or SpaceX from filing for what looks like the decade's biggest IPO, or Oracle from sacking staff so it could spend more on artificial intelligence.

A Quinnipiac poll found a majority of Americans now expect AI to make their lives worse - but it seems corporate capex budgets disagree.

Monday

Crude ground higher on the open, and the broader Middle East war refused to hand anyone a clean narrative.

Pakistan offered to host ceasefire talks as the Iran conflict intensified - a diplomatic bid neither Washington nor Tehran appeared in any rush to accept.

Trump doubled down on the pressure campaign, declaring that the U.S. could take Iran's oil and seize Kharg Island - the export hub handling roughly 90% of the country's crude shipments - if Tehran refused to reopen the Strait of Hormuz.

Whether that constitutes a negotiating posture or a policy commitment depends on which hour of the news cycle you happened to catch.

Yemen's Houthi rebels attacked Israel and threatened to close the Red Sea to shipping, dragging a second critical maritime chokepoint into the war and giving shipping insurers another sleepless night.

Brussels and Washington advanced a trade deal with safeguards - rare constructive transatlantic news against a backdrop of geopolitical noise - while Ukrainian drones crashed in Finland during reports of Russian GPS jamming, a prompt that Europe's eastern war hasn't gone anywhere.

Eli Lilly struck a mega-deal with Insilico Medicine to deepen its AI drug discovery pipeline, betting computational biology can compress the decade-long path from molecule to market.

Carnival flagged a $500 million hit to profits from fuel costs, spelling out in hard numbers what the Hormuz dislocation means for energy-intensive consumer businesses.

Bank of America agreed to pay $72.5 million to settle claims linked to the Jeffrey Epstein case, joining the lengthening roster of financial institutions paying to close that chapter.

U.S. consumer sentiment fell to a three-month low, weighed by fuel prices and war jitters - not exactly a surprise to anyone who has filled up a car in America recently.

A U.S. housing bill hit a rift over investor limits as the legislation returned to the House, where a provision restricting institutional investors from buying newly built single-family homes has divided lawmakers and drawn warnings from housing economists that it could slash output by 40,000 units a year.

Trump introduced new measures to support American farmers, while Canberra halved the fuel excise to hand temporary relief to motorists as war-driven energy costs flow through to the bowser.

Tuesday

RBC Capital Markets' Helima Croft, one of Wall Street's most-cited commodity strategists, laid out a sobering assessment of the oil market, arguing the Iran conflict has no single off-switch.

Brent had surged more than 55% in March - the steepest monthly gain on record - while three temporary measures propping up global supply were all set to lapse within days of each other in mid-April.

Croft characterised the Strait of Hormuz shutdown as insurance-driven rather than military, noting Iran's drones and mines were enough to keep underwriters and carriers out of the corridor without a formal blockade.

IEA estimates put the damage at 8 million barrels per day of lost global oil supply in March, the largest single dislocation the market has recorded, and Trump again threatened Iran's oil sites over the Hormuz closure as diplomatic channels remained frozen.

Iranian strikes on major Gulf smelters drove aluminium toward a four-year high, with LME futures touching $3,492 per tonne (t) after weekend attacks on Emirates Global Aluminium's Al Taweelah smelter and Aluminium Bahrain's production facilities.

Macquarie Group reckoned the damage could strip ~20% of effective regional capacity, equating to 800,000t to 900,000t of lost output in 2026.

Chinese manufacturers warned of price hikes tied to the Iran war, as surging energy and shipping costs began filtering through the world's largest production base.

Elsewhere, institutional money positioned for China's next expansion cycle, with T. Rowe Price portfolio manager Wenli Zheng pointing to consumer platforms, AI-linked hardware and traditional industries entering a harvest phase as three themes worth tracking under Beijing's latest Five-Year Plan.

Sysco (NYSE: SYY) shares plunged 15% after unveiling a $29 billion acquisition of Jetro Restaurant Depot - a debt-heavy play for independent restaurant supply chains that investors clearly felt was too rich, funded via $21.6 billion in cash, backed by debt and 91.5 million new Sysco shares at a time when credit spreads are widening.

Nasdaq rolled out new rules to fast-track large-cap listings onto its main index, a structural tweak aimed at luring mega-IPO candidates - with SpaceX and OpenAI both circling the public markets.

EU economic and consumer confidence slipped, reflecting the energy price transmission now weighing on the continent's already fragile growth outlook.

South Korean chip designer Rebellions raised $400 million for its U.S. expansion, evidence that the semiconductor investment cycle is pulling in capital despite the geopolitical backdrop.

Micron (NASDAQ: MU) shares shed 10% as the memory chip shortage continued to cloud forward guidance and order visibility.

Australian housing profitability reached a 20-year high, underscoring the widening gap between property owners and those still trying to break in.

Stateside, operations at U.S. airports returned to normal after the staffing upheaval of the prior week.

Wednesday

Washington warned the Iran war was nearing a decisive phase - a framing that carries the weight of either imminent de-escalation or sharp escalation, depending on which reading of the White House's signals you prefer.

Over in Martin Place, the RBA flagged a material economic effect from a longer war, joining the growing queue of central banks treating the Hormuz upheaval as a baseline planning assumption rather than a tail risk.

OpenAI closed a $122 billion funding round - Silicon Valley's largest ever - valuing Sam Altman's outfit at $852 billion ahead of a potential late-2026 IPO, with SoftBank co-leading the raise alongside Amazon, Nvidia and Microsoft.

Altman's company is assembling what it calls a "superapp" merging ChatGPT, coding tools, web browsing and agentic features, though it has yet to turn a profit and recently axed its Sora video app and Instant Checkout feature to pare costs - raising $122 billion while culling products is a uniquely Silicon Valley trick.

Fresh polling showed 55% of Americans expect AI to do more harm than good in their daily lives - up 11 percentage points from a year earlier - at the same time Amazon, Meta, Google and Microsoft are collectively expected to pour around $650 billion into AI infrastructure in 2026.

70% of respondents said AI would shrink job opportunities, 65% oppose data centre construction in their communities, and corporate America is spending as though the future is settled, while Main Street is not remotely convinced.

Oracle announced mass layoffs while redirecting capital toward AI - one more entrant in the growing club of firms shedding headcount to fund compute.

A deep analysis showed how tariffs quietly intensified China's trade grip rather than loosening it, with McKinsey Global Institute data revealing Chinese exports of intermediate goods - the components other countries need to build things - expanded 9% in 2025 despite U.S.-China bilateral trade falling ~30%, because firms are relocating the assembly, not the production network, and Beijing is increasingly the factory to the factories.

McCormick investors choked on news of a potential Unilever foods buyout, with the spice company's stock sliding on concerns about dilution and integration risk.

Nike (NYSE: NKE) beat earnings estimates but watched its China revenue continue to decline - a now-familiar pattern for Western consumer brands losing ground to domestic competitors.

U.S. consumer confidence ticked up modestly despite the war, providing a small counterweight to the broader deterioration in sentiment data.

American house prices grew slightly in January, while Australian dwelling approvals surged in February on the back of an apartment rebound.

NASA unveiled plans to send its first crew to the moon in over 50 years, chasing China's advancing 2030 lunar programme.

Superannuation peak bodies continued squabbling over switching data, and Trump signed an executive order to limit mail-in voting.

Thursday

Iran denied Trump's claims that it had asked for a ceasefire, keeping to the now-familiar pattern in which Washington and Tehran offer incompatible accounts of the same diplomatic exchange.

Tehran then warned U.S. tech giants of imminent cyber attacks, opening yet another front in a war that has already spread across sea lanes, commodity markets and - now - corporate networks.

SpaceX reportedly filed for an IPO ahead of an analyst day, which would rank among the most anticipated listings in a generation, given the company's estimated valuation north of $350 billion - and, coupled with OpenAI's $122 billion round landing in the same week, confirmation that the private-to-public capital pipeline is running at full bore.

Intel (NASDAQ: INTC) shares rallied 9% after the chipmaker re-bought its stake in an Ireland plant, a renewed commitment to European fabrication capacity at a time when semiconductor sovereignty sits near the top of every policymaker's agenda across the Atlantic.

On the ASX, Australia's first humanoid robotics ETF debuted, giving local investors their inaugural listed vehicle for a sector where AI, manufacturing and science fiction are converging faster than most analysts expected.

Tesla guided for slight delivery growth in Q1 - a modest target reflecting the EV market's shift from hypergrowth to something closer to normal automotive cadence.

U.S. manufacturing PMI rose in March, but the details told a different story - supplier delivery times lengthened, signalling the Hormuz shock is now choking industrial supply chains the same way it has already squeezed energy markets, and when factory data starts confirming what crude is screaming, the stagflation argument gets harder to dismiss.