Analysts have been left scratching their heads trying to pick the market lately, with Brent crude rising more than 55% in March - the steepest monthly gain on record - and the three temporary measures propping up global supply are set to lapse within days of each other in mid-April.

Brent was trading above US$115/bbl on Monday morning, up ~2% from Friday's settle of US$112.57 and on track for the largest single-month surge in the benchmark's history, according to CNBC.

That surpasses the 46% spike recorded during the Gulf War in September 1990, while WTI briefly crossed US$103 intraday for the first time above the US$100 mark.

The futures price is one thing, though - what matters now is the clock.

The IEA's 400-million-barrel strategic reserve release, the U.S. Treasury's sanctions reprieve on Russian oil and temporary exemptions for Iranian barrels are the three stopgaps keeping this disruption manageable.

BCA Research's Marko Papic estimates they all run dry at roughly the same time in mid-April, a convergence he's calling an "oil cliff".

Once those lapse, there's no substitute for crude flowing through the Strait of Hormuz - the 21-mile-wide chokepoint between Iran and Oman that carries roughly 20% of the world's seaborne oil and has been effectively shut to commercial traffic since early March.

Nobody with the authority to reopen the waterway is showing any sign of doing so.

How the Strait shut without a blockade

RBC Capital Markets' Helima Croft, head of global commodity strategy and a former CIA senior economic analyst, has tracked the fallout through her "Iran Flashpoints" series since the joint U.S.-Israeli strikes began on 28 February.

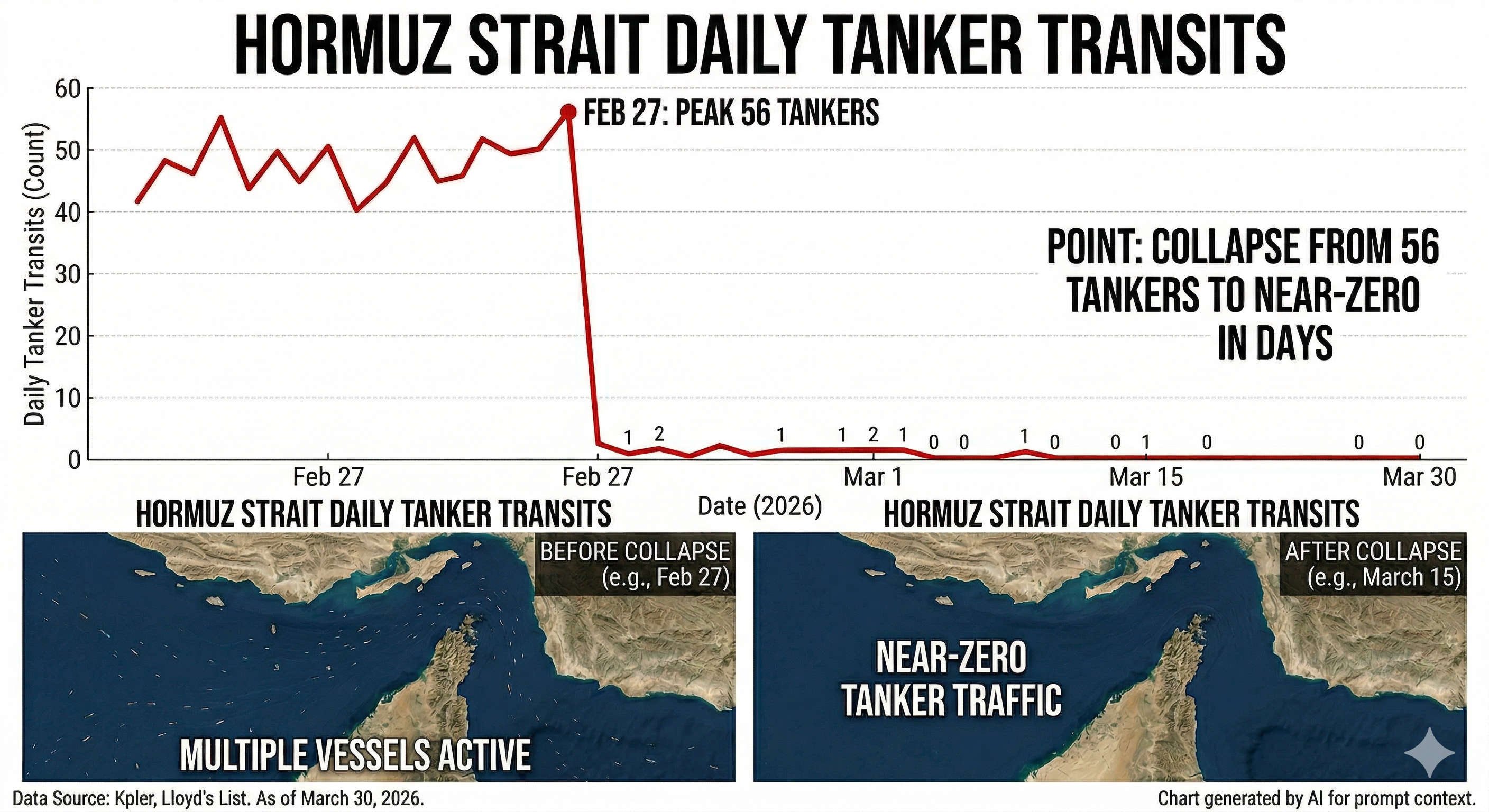

The speed of the shutdown caught most analysts off guard - tanker traffic through the passage collapsed from 56 vessels on 27 February to near-zero within days.

"It's really an insurance-driven shutdown," Croft said on NPR.

"All [Iran] had to do was several drone strikes in the vicinity of the Strait of Hormuz, and all of a sudden, insurers and shipping companies decided that it was unsafe to traverse that very narrow S-curve of that waterway."

Iran's Islamic Revolutionary Guard Corps didn't need a full naval blockade - small boats, mines and drones proved sufficient to keep underwriters and carriers out of the corridor, vessel tracking firm Kpler confirmed.

Washington's proposed $20 billion maritime reinsurance facility through the Development Finance Corporation hasn't shifted that calculus.

Croft noted in a separate Flashpoints report that the potential insurance exposure of vessels currently in the Gulf likely exceeds the DFC's entire $205 billion statutory risk limit.

The bypass routes aren't faring any better.

Saudi Arabia's East-West pipeline to the Red Sea port of Yanbu can move up to 5 million bpd, but tanker rates from Yanbu have more than doubled to $28 million per vessel.

Fujairah port in the UAE, marketed for years as a safe corridor outside the chokepoint, has come under drone attack from Iranian forces.

Iran announced on 26 March that it would permit vessels from China, Russia, India, Iraq and Pakistan to transit the waterway, but two Chinese container ships were subsequently turned back.

The result, per the International Energy Agency's March Oil Market Report: global oil supply fell by an estimated 8 million bpd in March, the largest supply disruption in the history of the global oil market.

IEA executive director Fatih Birol described the effect as worse than the two 1970s oil shocks and the Russia-Ukraine gas shock combined.

Physical crude is telling a different story

That 8 million bpd loss is hitting physical markets far harder than futures.

Cash Dubai premiums - what buyers pay for actual delivery - reached US$62.68/bbl in mid-March per Croft's 19 March report, and the Dubai physical benchmark was at $126/bbl as of Friday, roughly $13 above the Brent settle.

"There really is a difference in terms of physical supply this time versus prior incidents," Chevron CEO Mike Wirth said at S&P Global's CERAWeek conference in Houston.

"The markets are trading on scant information."

Rystad Energy's chief oil analyst Paola Rodriguez-Masiu noted on CNBC that the temporary cushion provided by pre-war surplus, crude-on-water and strategic reserve drawdowns is now ending.

Dan Pickering, CIO of Pickering Energy Partners, put it to NPR this way: you can wear two hats on crude right now - "Why is it so high?" if this war ends soon, or "Why is it so low?" when a fifth of global supply is bottlenecked behind the strait.

How far it goes depends on who you ask

Goldman Sachs lifted its full-year 2026 Brent forecast to $85/bbl from US$77, assuming Hormuz flows stay at 5% of normal for six weeks followed by a one-month recovery.

An adverse scenario where the disruption runs for 10 weeks takes Brent to a peak of $140, with a severely adverse case involving infrastructure damage pushing it to $160.

The bank pegs the 12-month U.S. recession probability at 30%, up from prior estimates, with unemployment expected to climb to 4.6% by year-end.

Not everyone is that bearish.

Chatham House reached a different conclusion in early March: if the conflict proves short-lived and production facilities avoid lasting damage, the spike above $100 would likely be temporary, with inflation in Europe and Asia running only ~0.5 percentage points above pre-conflict forecasts.

Croft's own firm, RBC Economics, argued that a U.S. downturn remains unlikely, pointing to the fiscal deficit running at 6-7% of GDP, inflation-indexed social security transfers near historic highs, unemployment near record lows and continued AI-related capex as structural buffers.

BlackRock CEO Larry Fink framed the spread as binary: either global powers accept Iran and its oil reaches the market at $40/bbl, or the regime remains adversarial and crude stays above $100 - closer to $150 - for years.

Every one of those scenarios turns on whether the waterway reopens before the backstops lapse.

Three parties, three timelines, no deal

Iran's new supreme leader, Mojtaba Khamenei - who succeeded his father after the 28 February strikes - publicly vowed to keep the chokepoint sealed.

Tehran's five-point counteroffer to Trump's 15-point plan demands war reparations, sovereignty over the Strait of Hormuz and a comprehensive end to hostilities across all fronts including Lebanon.

Iran's foreign minister Abbas Araghchi said on state media that Tehran doesn't want a ceasefire - it wants the war to end on its own terms.

Washington's position requires full dismantlement of Iran's nuclear programme, sharp limits on its missile arsenal and reopening of the passage.

Trump extended his deadline to 6 April for Iran to reopen the waterway or face strikes on its power plants, but escalated over the weekend by telling the Financial Times his preferred option would be to "take the oil" and threatening to destroy Iran's wells, power plants and the Kharg Island export hub.

Israel appears to be moving in the opposite direction - reports indicate Israeli leadership was caught off guard by the ceasefire proposal, with the IDF reportedly accelerating strikes on Iranian arms factories in case a deal materialises.

The conflict widened further over the weekend when Yemen's Houthi rebels - an Iranian proxy that had largely stayed on the sidelines - fired missiles at Israel.

RAND's Raphael Cohen characterised the U.S. troop buildup - including the 82nd Airborne and two Marine Expeditionary Units totalling ~4,700 troops - as coercive diplomacy rather than preparation for a ground war.

Iranian-American historian Arash Azizi said on CNBC that some sort of pause in the next couple of weeks is likely, but the question is what follows - either a lasting agreement or a war of attrition.

Russia picks up the tab

With Gulf barrels stranded, Moscow is selling oil at elevated prices to a buyer Washington itself approved.

The U.S. Treasury issued a 30-day sanctions carve-out allowing Indian refiners to purchase stranded Russian crude, with Kpler analysts projecting India's Russian intake could return to 40-45% of imports.

Washington spent the past year pressuring New Delhi to cut Russian purchases - including slapping 50% tariffs on Indian exports and sanctioning Rosneft and Lukoil - before granting a reprieve that effectively reverses that effort.

Congressional Democrats demanded the carve-out be reversed, noting reports that Russia is assisting Iran in targeting U.S. assets in the region.

The exemption doesn't lapse until early April, at which point it becomes another backstop that vanishes.

Croft noted the Russian release valve has structural limits, given that EU and Congressional restrictions remain intact.

The next two weeks

The industry executives who actually move barrels for a living were blunt at CERAWeek in Houston last week.

"You just can't take 8 to 10 million barrels a day of oil and 20 or so % of the LNG market off the world stage without having some significant repercussions," ConocoPhillips CEO Ryan Lance said at the conference.

Kuwait Petroleum CEO Sheikh Nawaf al-Sabah described the Hormuz closure as an economic blockade against Middle Eastern producers, saying the costs of this war "don't stay within geographical lines in this region - they extend all the way through supply chain."

Refined fuel prices for diesel and jet fuel have at times exceeded $200/bbl, Pakistan has asked cricket fans to watch matches from home to conserve fuel, hundreds of Australian service stations have reported shortfalls, and South Korea has imposed a five-month restriction on naphtha exports.

The OECD expects U.S. inflation to average 4.2% in 2026, up from 2.6% in 2025.

The 10-year Treasury yield closed Friday at 4.46% - its highest since July 2025 - and the S&P 500 settled at 6,368.85, a seven-month low, with the Dow entering correction territory after shedding 793 points on the session.

Croft's base case: if the conflict drags on for several months with little improvement in maritime transit, oil prices could exceed the 2008 record of US$146/bbl.

Energy analyst Rory Johnston described the market to NPR as simultaneously pricing the largest supply shock in history and the possibility it could end at any moment.

Trump's 6 April deadline is one week away, and the mid-April buffer expiry is two weeks after that - if the strait hasn't reopened by then, the supply arithmetic changes.