The Hormuz blockade has removed a fifth of global LNG from the market at the worst possible moment, and every week of delay makes the refill maths harder to solve.

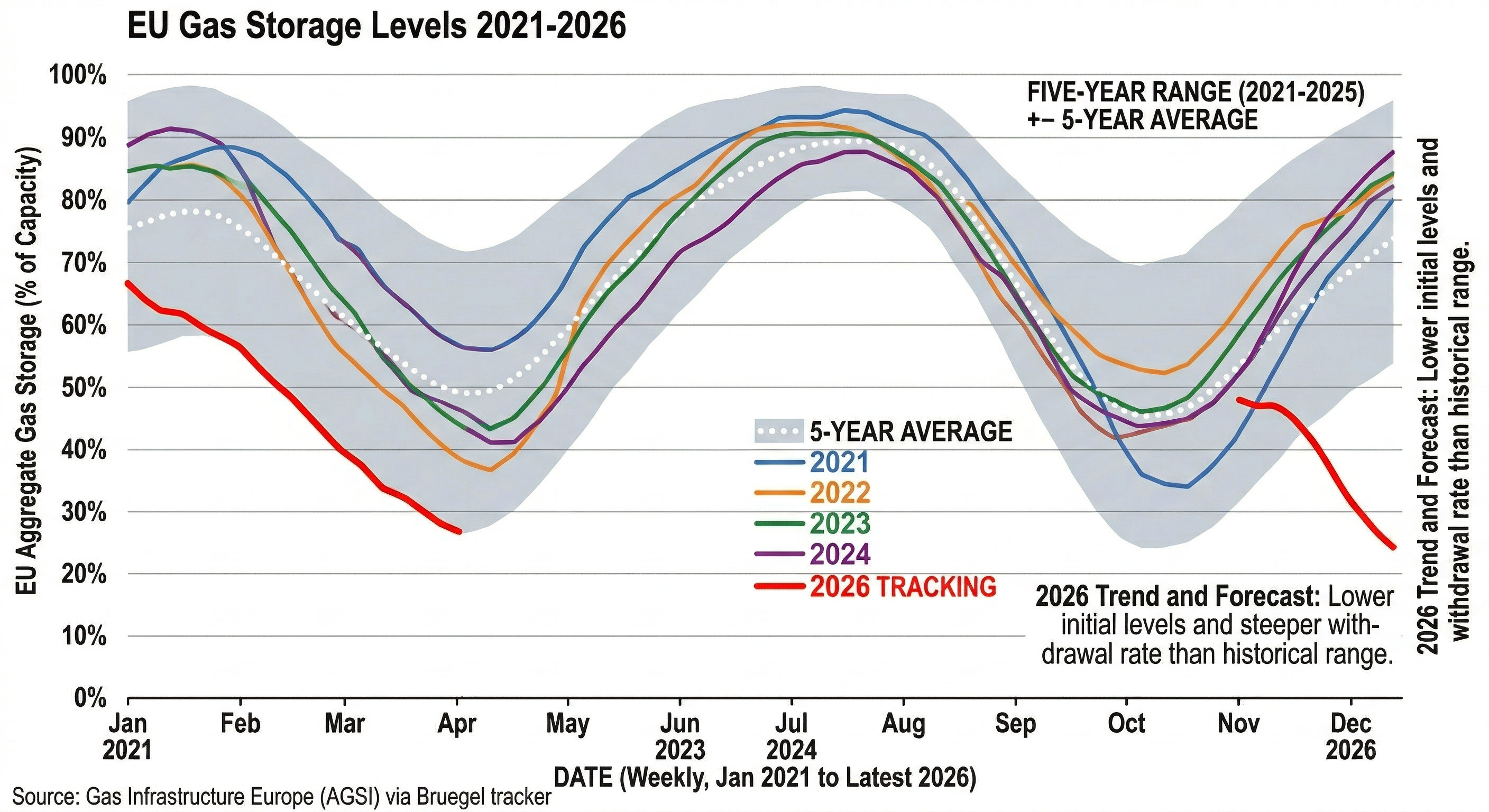

EU gas storage stood at around 28% capacity in early April, its lowest seasonal level since the 2022 supply crunch, with Germany roughly a fifth full and France in a similar position.

These numbers would ordinarily prompt mild concern and a busy injection season through spring and summer, but three compounding disruptions have turned a routine refill task into something far more precarious.

The Strait of Hormuz remains closed to Western commercial shipping, though Iran has granted selective passage to Chinese, Russian, Indian, Pakistani, and Philippine-flagged vessels, creating a two-tier transit system.

Qatar's Ras Laffan complex is physically damaged, Asian buyers are scrambling for every available cargo, and European utilities are stuck on the wrong side of the access list.

That matters because EU regulation mandates gas storage to reach at least 90% capacity before winter, though the European Commission has told member states to consider targeting 80%.

Some countries have been allowed to drop as low as 70-75%, a measure of how far the goalposts have shifted since the Strait closed.

Even hitting the relaxed 80% target from a 28% starting point requires a refill rate roughly double what Europe managed during the relatively comfortable restocking period of 2025.

The early numbers confirm the shortfall: daily injection forecasts for April sit at roughly 34 million cubic metres per day, a 77% decline compared with the same period last year.

Worse still, LNG from the spot market - Europe's primary marginal source - is now the subject of a bidding war with importers across Asia who have lost their Qatari contract volumes.

"Reserves have never been this low at this time of year," Bruegel senior fellow Simone Tagliapietra told the Financial Times.

"Filling gas storage facilities for the next winter starts now. If this has to be done at such prices, the burden on Europe will be enormous."

Why Qatar punches above its weight

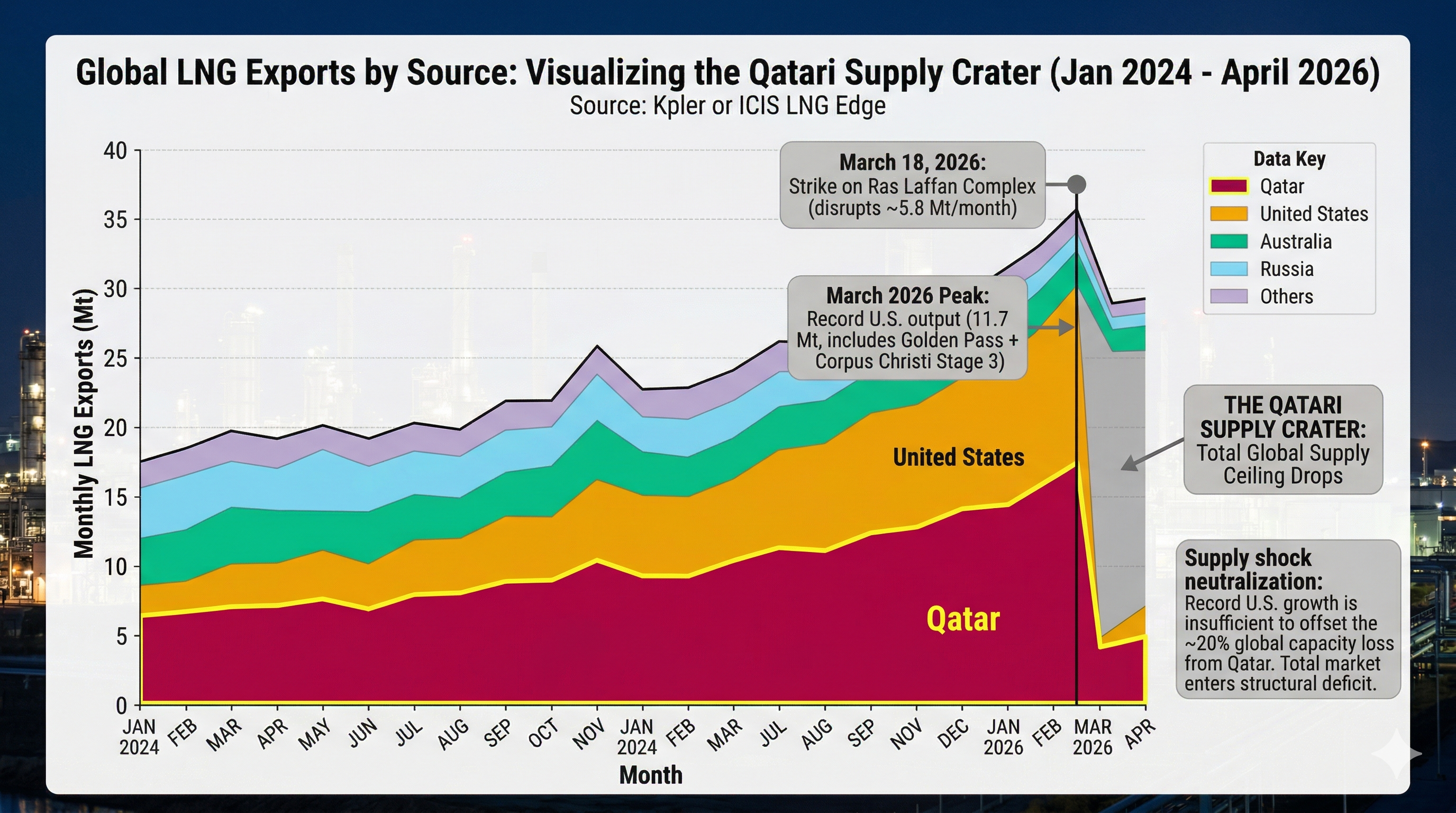

Qatar accounts for roughly 20% of global LNG trade, and the Ras Laffan complex in the country's northeast handles about a fifth of all seaborne gas as the world's largest export facility.

Iranian missile strikes in March knocked ~17% of the facility's liquefaction capacity offline for what QatarEnergy's own estimates suggest will be years rather than months.

Fitch responded by placing Qatar's AA sovereign rating on watch negative, with the annual revenue loss running to an estimated US$20 billion.

Europe imported just 9.2 million tonnes (Mt) of LNG from Qatar last year, roughly 8% of total imports, which might suggest the direct exposure is manageable.

What that figure misses is how LNG markets clear when a supplier of this scale goes offline: importers who lose Qatari volumes redirect purchasing power into the same open market European utilities rely on.

Since LNG replaced Russian pipeline flows as the swing molecule in Europe's gas mix, the continent must outbid China, India, Japan, and South Korea - or go without.

That competition showed up immediately in the price data, with Dutch TTF gas futures surging roughly 85% over March and briefly punching above €60/MWh for the first time since February 2025.

Goldman Sachs hiked its April forecast to €55/MWh from €36/MWh within days, while the Asian JKM benchmark moved in lockstep and U.S. Henry Hub barely shifted.

A refill season with no spare supply

The damage extends beyond operating capacity, because construction on Qatar's North Field East expansion has also been halted.

The project was intended to add 33Mt per annum of LNG, equivalent to roughly half of Germany's annual gas consumption.

If the shutdown persists through the Gulf's summer heat, commissioning may slip into late 2026 or early 2027, removing volumes the market had already pencilled into its forward balance.

That leaves European storage operators caught between weak incentives and shrinking options, because the inverted summer-winter spread has eliminated any commercial reason to buy and inject.

Governments stepped in directly to fill that gap in 2022 and the same playbook is being dusted off, but the supply side is tighter and the fiscal headroom thinner than four years ago.

"This is a double blow," Eurasia Group expert Henning Gloystein told the Financial Times.

"Europe has just started to recover from the industrial energy crisis, and now we have the next one."

Who gains and who absorbs the pain

While Europe scrambles, Russia is collecting the windfall - a difficult reality for a continent that spent three years weaning itself off Moscow's hydrocarbons.

Western sanctions had compressed Russian fossil fuel revenues to roughly $501 million per day by January 2026, but within two weeks of the Hormuz closure, daily revenues rebounded to approximately $554 million.

The Urals crude discount to Brent narrowed from $25 per barrel to $15, and by mid-March, Urals had doubled to $90 from its February lows, with Brent itself now trading above $110.

Russian gas exports to Europe via TurkStream rose 10% in the first quarter, leading the EU to debate whether to delay its timeline for phasing out Russian imports.

The benefits extend beyond hydrocarbons: Moscow's fertiliser exports are picking up new customers in Nigeria and Ghana, pre-purchasing for the third quarter, commercial relationships that tend to outlast the conditions that created them.

China occupies a more layered position, holding roughly six months of strategic oil reserves and displacing more than a million barrels per day of implied domestic oil demand through its electric vehicle fleet.

That cushion provides short-term breathing room, and Chinese-flagged vessels appear to retain some preferential passage through the strait, but 30% of China's LNG imports still route through Hormuz via Qatar and the UAE.

The longer the disruption persists, the stronger the case for overland alternatives, which is why discussions around Russia's Power of Siberia 2 pipeline are accelerating after Beijing resisted the project for years.

A fresh draft of China's five-year plan mentioned new Russian pipeline infrastructure for the first time in March, a shift that would have drawn far more attention in quieter times.

India faces a severe dual shock, with more than 60% of its oil imports originating from the Middle East and Qatar and the UAE accounting for over half its LNG supplies.

The downstream effects are already visible: three Indian urea plants have cut production due to reduced Qatari deliveries, squeezing fertiliser supply ahead of the kharif planting season.

Indian refiners are meanwhile ramping purchases of Russian crude at a pace that puts March shipments on track to nearly double February volumes.

Those Russian cargoes are arriving at prices exceeding the Brent benchmark, an inversion few traders would have entertained six months ago.

Further down the income ladder, Pakistan and Bangladesh sit at the receiving end of this adjustment, with Islamabad having sourced 99% of its LNG from Qatar and both terminals facing shutdown by month's end.

Power sector load shedding across the country and industrial gas supply cuts in Bangladesh are already underway - a reminder that the global gas market's default adjustment mechanism is enforced rationing of its poorest participants.

What comes next

The most immediate catalyst is diplomatic: Egyptian, Pakistani, and Turkish mediators submitted a 45-day ceasefire proposal over the weekend, calling for a halt in hostilities and the reopening of the strait.

Iran rejected it, demanding a permanent settlement rather than a temporary pause, while President Trump called the proposal "not good enough."

Trump has set a Tuesday 8pm ET deadline for Tehran to reopen Hormuz or face strikes on its power plants and bridges, an ultimatum Iran has so far dismissed.

Whether that deadline produces a breakthrough or further escalation will shape the trajectory of gas and oil markets for the rest of the quarter, and neither outcome looks priced with any confidence.

The policy response is catching up to the price action, but slowly: the ECB postponed its planned March interest rate cut, raised its 2026 inflation forecast, and trimmed GDP growth projections.

The OECD followed with a warning that global growth could ease to 2.9% in 2026 as energy price pressures and geopolitical uncertainty weigh on developed and emerging markets alike.

A fuller picture will arrive on 14 April when the IMF publishes its World Economic Outlook, the first official damage assessment to capture the conflict and the Hormuz disruption in a single report.

Gas is a storable commodity, but storage requires injection, and injection requires available supply at commercially viable prices - neither of which is being met while the strait remains closed.

The U.S. is insulated by its own production base, Russia is enriched by the price spike and the collapse of its competitors' export routes, and Asia is scrambling for replacement cargoes.

Europe is discovering that swapping one energy dependency for another has not made it safer, just differently exposed.