Canberra and Washington have pledged more than US$5 billion to critical minerals projects in Australia this week, ahead of the 20 April six-month milestone under their October framework.

Named priority recipients include Tronox, Ardea Resources, Arafura and Alcoa-Sojitz, backed by Export Finance Australia and the U.S. Export-Import Bank.

Catch is, the framework's forward economics depend on two geopolitical deadlines, and neither is locked in.

Beijing has to keep its rare earth export controls suspended past November, while Trump needs a price floor deal signed before the 13 July cutoff.

Where the capital is heading

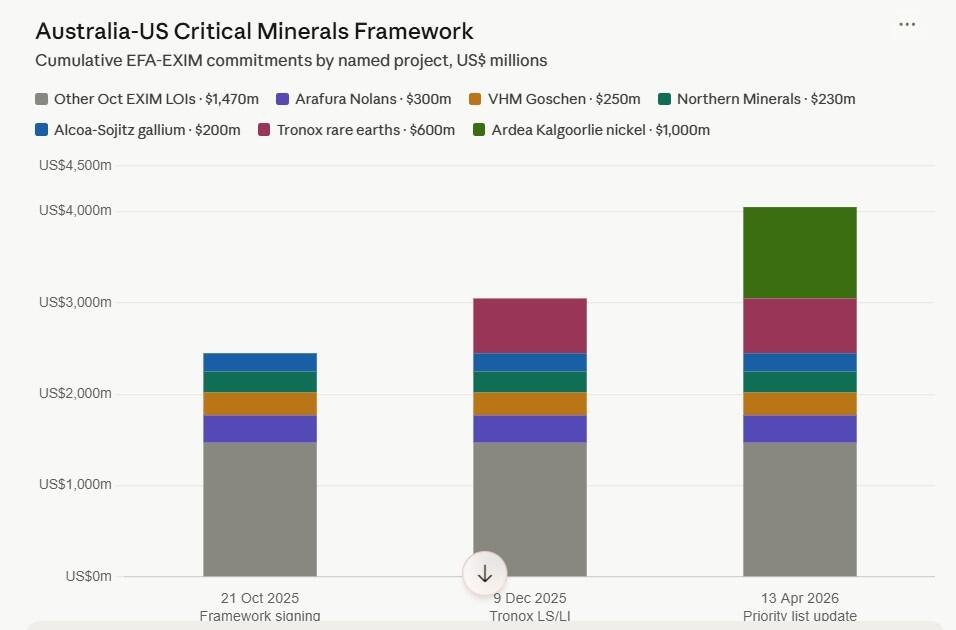

Minister for Resources Madeleine King and US Secretary of the Interior Doug Burgum confirmed priority projects under the bilateral framework on 13 April.

The biggest single cheque landed with Tronox (NYSE: TROX), which picked up coordinated letters of support worth around US$849 million for a new Western Australian rare earths refinery.

Close behind, Ardea Resources (ASX: ARL) drew roughly A$1 billion of combined backing for its Kalgoorlie nickel-cobalt project - the largest nickel-cobalt resource in Australia.

Arafura Rare Earths (ASX: ARU) held onto its marquee position, with the Nolans project remaining one of only two priority assets from the October 2025 framework signing.

Rounding out the headline allocations, the Alcoa-Sojitz Wagerup gallium recovery venture received up to US$200 million in Australian concessional equity, alongside US and Japanese government contributions.

Away from the funding announcements, Lynas Rare Earths (ASX: LYC) posted its highest quarterly revenue since mid-2022 on 21 April, delivering A$265 million in March-quarter gross sales.

Behind that number, total rare earth oxide production reached 3,233 tonnes (t) and the average neodymium-praseodymium (NdPr) selling price rose 25% quarter on quarter.

On the legislative side, the A$1.2 billion Critical Minerals Strategic Reserve's enabling amendment bill passed Parliament on 31 March, coming into effect the following day.

That gives Export Finance Australia fresh statutory powers to secure, stockpile and on-sell critical minerals on Canberra's behalf.

Beijing's pause

China announced a suspension on 7 November 2025 of its 9 October 2025 rare earth export control package, extending the pause until 10 November 2026.

None of the underlying mechanisms have been struck off.

The 50% Rule, trace-content thresholds on overseas-manufactured magnets and the extraterritorial licensing regime all remain on the books, just unenforced through to that expiry date.

Buyers have not been taking chances either, and Lynas CEO Amanda Lacaze flagged a renewed customer focus on securing outside-China supply chains amid ongoing disruptions.

The April 2025 episode informs that caution - Chinese controls on seven heavy rare earths forced some US and European carmakers to cut utilisation rates or shut factories, per IEA analysis.

The current Trump-Xi détente is holding the suspension in place for now, though Chinese officials have stopped short of any commitment on whether the pause becomes permanent.

Trump's deadline

The other clock is ticking in Washington.

Trump's 14 January 2026 Section 232 proclamation directed Commerce and the U.S. Trade Representative to negotiate price floor agreements covering 60 critical minerals plus uranium.

The 180-day reporting deadline lands on 13 July 2026.

Against that window, U.S. Trade Representative Jamieson Greer was slated to begin formal negotiations with the European Union and Japan in April.

Vice President JD Vance laid the groundwork at the 4 February Critical Minerals Ministerial, floating "Pax Silica" - a preferential trade zone underwritten by adjustable tariffs above a cost-of-production floor.

Should agreements fail to materialise, Trump has reserved the right to impose minimum import prices or Section 232 tariffs directly on processed critical minerals and derivative products.

Both scenarios would reshape the economics for Australian developers - hard tariffs reroute supply chains overnight, while a softer agreement erodes the price-floor premium underpinning Arafura, Northern Minerals (ASX: NTU) and Ardea.

If the deadlines slip

There is also the quieter scenario, where a broader U.S.-China trade rapprochement lifts Washington's urgency just as Beijing tightens licensing again, compressing producer margins.

The signals are already mixed, with Chinese rare earth magnet exports rising 8.2% year on year in the first two months of 2026, yet shipments to the U.S. falling 22.5%.

Beijing is applying selective access, holding exports up globally while diverting volume away from U.S. buyers.

On pricing, China's rare earth price index reached 283.2 on 21 April, nearly 2.8 times the 2010 baseline.

Within that, magnet materials continued tightening while commodity light rare earths stayed flat, pointing to concentrated demand in high-performance applications.

A policy reversal in Washington or a quiet licensing reinstatement in Beijing would shift the sector's forward curve across a matter of weeks.

Project timelines compound the pressure, with Arafura's funding package carrying a sunset clause expiring 1 December 2026 that limits how far FID can slip without a restructure.

Iluka Resources (ASX: ILU) faces similar drag, after Eneabba capex drifted from A$1.2 billion to between A$1.7-$1.8 billion, with 2027 commissioning.

Northern Minerals sits further back again, unable to produce from its Browns Range heavy rare earth project until 2028 at the earliest.

That is the gap between committed capital and operational output.