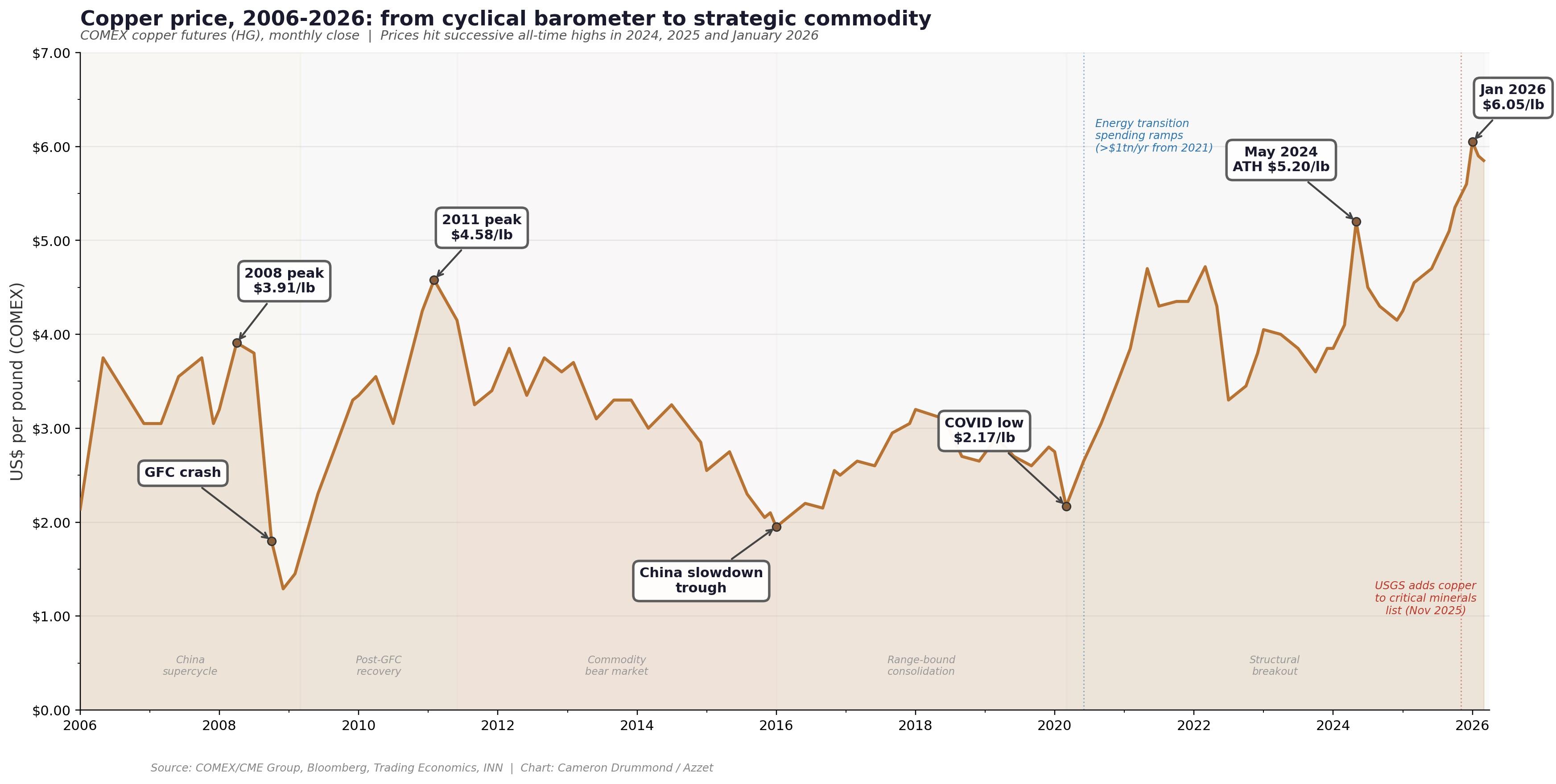

Copper's identity crisis is over - and the market is only just catching on. The red metal hit record highs above US$13,000 per tonne (t) in early January, capping a year in which it gained more than 35% - its best annual return since 2009.

According to Steve Schoffstall, Head of ETFs at Sprott Asset Management, the rally reflects a secular shift that has been building for half a decade - one that changes what copper is, who needs it, and how much there is to go around.

"An area where we've seen significant growth over the last two or three years that didn't exist before was AI and associated data centres," Schoffstall said.

"These associated data centres, along with hyperscalers building massive, power-hungry facilities, are expected to be a significant driver of electricity demand growth."

Speaking on a Sprott webcast, Schoffstall laid out a thesis that reframes copper from a cyclical construction barometer - the old "Dr. Copper" of business-cycle textbooks - into a strategic commodity, one that underpins electrification, artificial intelligence, defence modernisation and the energy transition at once.

A January study by S&P Global projects global copper demand will rise 50% from 28Mt today to 42Mt by 2040 - and that supply, absent major new investment, will fall roughly 10Mt short.

The International Energy Agency has flagged a similar tension, noting copper prices briefly exceeded $14,500/t intraday in January 2026, driven by mine outages, tariff-related stockpiling in the U.S. and a broadening consensus that demand is outpacing what the supply chain can deliver.

Not your grandfather's copper market

The core of Schoffstall's argument is that copper's demand profile has shifted in kind, not just degree.

Electrical infrastructure overtook construction as the largest source of copper consumption last year, now accounting for roughly 30% of the total.

S&P Global projects the share from traditional end uses - construction, appliances, conventional vehicles - will fall from 68% to about 55% by the end of the next decade, while newer vectors, including AI, defence and clean energy, fill the gap at a compound annual growth rate of approximately 2.9%.

"Copper prices are more directly tied to structural changes and demand than in the past, when demand was more cyclical and construction-driven," Schoffstall said.

That decoupling is already showing up in price data.

Since February 2021, physical copper has returned around 64%, while Chinese equities - the asset class copper was historically tethered to - have dropped roughly 28%.

A pronounced divergence for a metal whose price once moved in near-lockstep with China's property cycle.

Supply side worse than it looks

If the demand story is secular, the supply story is geological - and geology operates on its own schedule.

Schoffstall pointed to a cluster of setbacks that tipped the market into deficit late last year: a major mudslide at Indonesia's Grasberg mine (the world's second-largest), a 65% production drop at the Kamoa-Kakula operation in the Democratic Republic of Congo, and an ongoing shutdown at First Quantum's Cobre Panama mine, which had represented roughly 1.5% of global output before citizen opposition forced it closed.

Chile's state-owned Codelco, meanwhile, has flagged that production at its flagship El Teniente mine - curtailed 15-20% after seismic issues - won't recover for several years.

"Keeping these mines fully operational is challenging," Schoffstall said.

"We've mined it for so long, most of the easy copper ore we have to mine has already been mined out."

Declining ore grades mean miners must dig deeper and process more rock to extract the same volume of metal.

Only 14 of 239 new copper discoveries since 1990 qualify as "major," and the average timeline from discovery to production now sits at around 17 years.

In the spot market, the squeeze is visible in treatment charges - the fees smelters charge miners to process concentrate.

Those charges have turned negative since around 2024, meaning smelters are effectively paying miners for the right to process their material.

"These smelters are trying to keep their doors open," Schoffstall said.

"They're willing to pay about $40/t to the miners for the privilege of processing the material."

The IEA confirmed the 2026 annual benchmark treatment charge has settled at $0/t - effectively wiping out smelter processing income entirely.

Critical mineral status changes policy

In November 2025, the U.S. Geological Survey added copper to its critical minerals list for the first time, joining the EU, China and Canada in recognising the metal's strategic importance.

The designation is more than symbolic.

It opens the door to streamlined permitting, government procurement incentives and, potentially, the kind of strategic stockpiling already underway in rare earths.

"Once a mineral is identified and added to a government's critical materials list, it signifies how important that metal is to defence, aerospace, high-tech industries and other aspects of the economy," Schoffstall said.

He noted the U.S. government has already taken a stake in Trilogy Metals to support development of a copper deposit in Northern Alaska, and pointed to a $12 billion public-private initiative called Project Vault, designed to establish a critical materials stockpile accessible to American companies.

What miners are doing with the margin

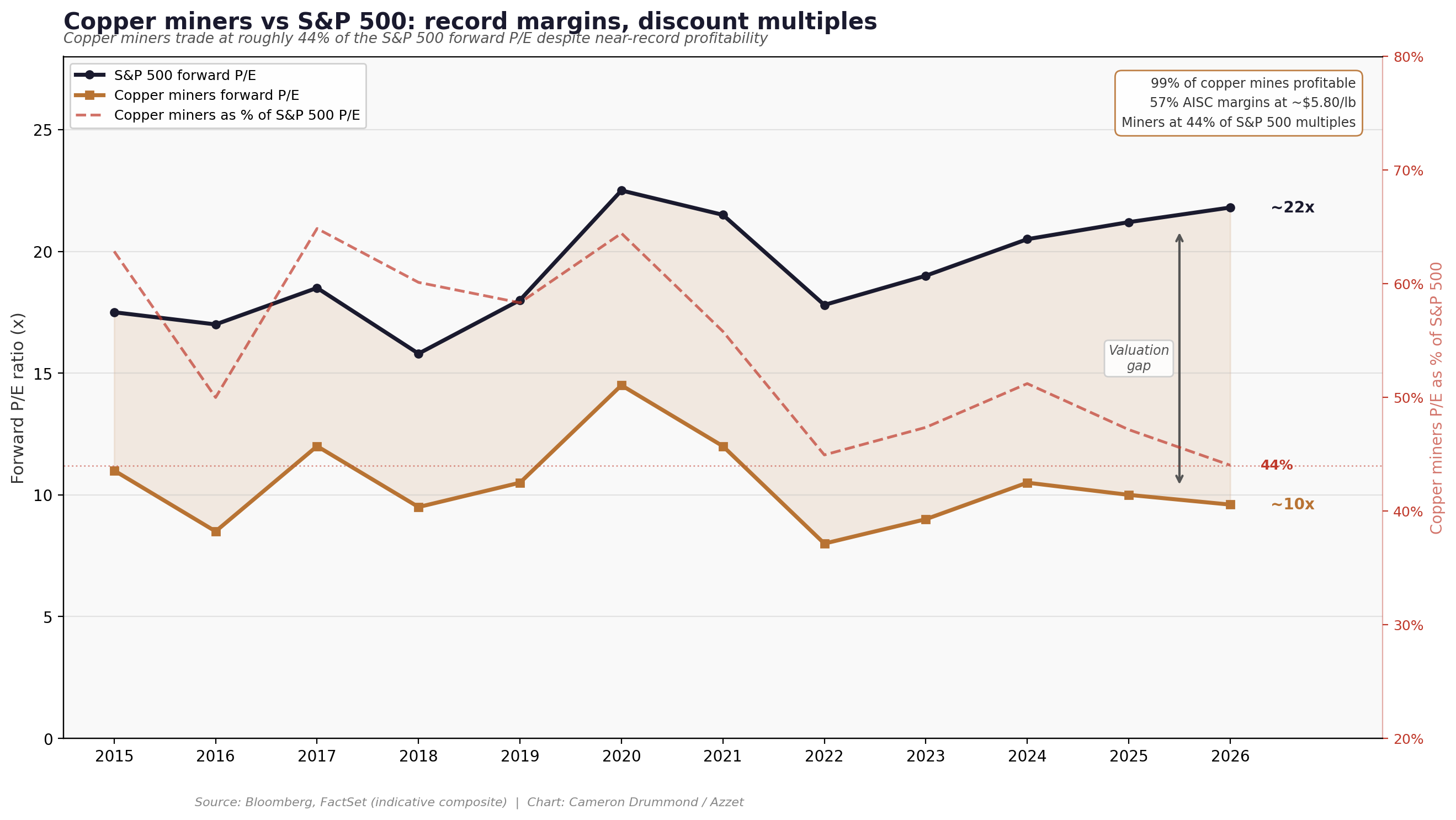

At current prices - around $5.80-5.90 per pound - Schoffstall said pure-play copper miners are operating at roughly 57% all-in sustaining cost margins, with about 99% of copper mines now in the black.

"Not only do we have the improving balance sheets, but we also have an asset class that, relative to other U.S. equities, is undervalued," he said, noting copper miners trade at approximately 44% the valuation multiple of the S&P 500.

Strong commodity prices, constrained supply, improving free cash flow and a valuation discount the broader market hasn't fully closed.

The open question is whether a cyclical downturn - a Chinese consumption wobble, a tariff resolution that releases hoarded inventories, or a global recession - resets the clock.

Goldman Sachs has cautioned that recent price strength has been driven more by speculative positioning and tariff-related stockpiling than by real-time consumption, forecasting a pullback to $11,000/t by year-end once tariff uncertainty clears.

But even the bears tend to concede the longer-term picture. As S&P Global vice chairman Daniel Yergin put it:

"Copper is the great enabler of electrification, but the accelerating pace of electrification is an increasing challenge for copper."