The Federal Reserve's preferred inflation measure accelerated to its highest annual rate since 2023 in May, while the United States economy expanded much faster than previously estimated during the first quarter, reinforcing expectations that interest rates will remain elevated for an extended period.

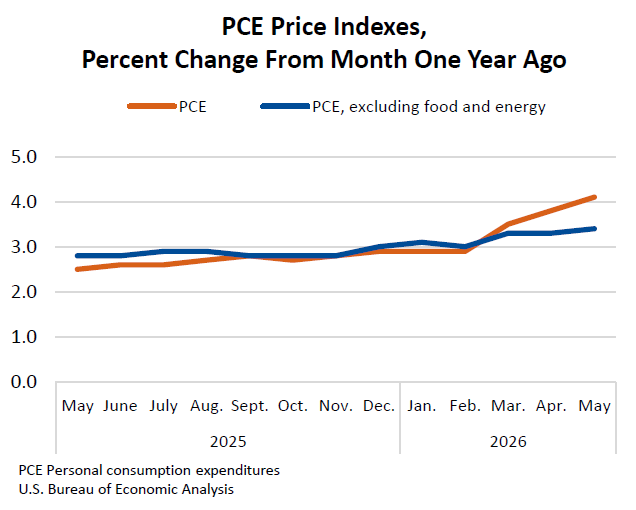

Data released by the Commerce Department's Bureau of Economic Analysis on Thursday showed the core personal consumption expenditures (PCE) price index, which excludes food and energy, increased 0.3% in May, lifting the annual inflation rate to 3.4%.

The annual reading marked the highest level since October 2023.

The headline PCE index rose 0.4% during the month, taking annual inflation to 4.1%, the strongest reading since April 2023.

The annual figure was in line with market expectations, while the monthly increase was 0.1 percentage point below forecasts.

Although Federal Reserve policymakers monitor both headline and core inflation, they place greater emphasis on the core measure as an indicator of underlying price pressures. This year's inflation acceleration has been driven largely by higher energy prices linked to the Iran conflict, with those cost increases increasingly filtering through to other parts of the economy.

ANZ analysts said the data continued to support expectations that the Federal Reserve would maintain restrictive monetary policy.

"Both the PCE deflator and the core inflation measure are too high relative to target and underpins our expectation that the Fed will hold rates steady into mid-2027 to exert downward pressure on inflation.

"The breakdown of the data, however, was more encouraging. Service prices rose 0.5% m/m, but the gain was concentrated in finance and insurance (+1.2% m/m) and transportation (+0.8% m/m).

"In May, portfolio fees rose strongly. Portfolio fees are imputed. Market-based PCE, which is around 85% of the index, excludes imputed prices. It rose 0.24% m/m, down from 0.28% m/m in April and 0.42% m/m in February.

"That easing does not suggest a broadening in inflation pressures outside of the energy sector."

Despite the stronger inflation readings, household demand remained resilient. Personal consumption expenditures, a key measure of consumer spending, increased 0.7% during May, exceeding expectations of a 0.6% gain and comfortably outpacing inflation.

Personal income also rose 0.7%, well above forecasts for a 0.4% increase, while the personal saving rate edged up to 3%.

The latest figures follow last week's Federal Reserve meeting, where policymakers adopted a more hawkish tone on inflation and interest rates. Fed Governor Kevin Warsh also stressed the importance of restoring price stability, with the Federal Open Market Committee stating it would "deliver price stability" after missing its 2% inflation target for five consecutive years.

In addition, policymakers removed a previously anticipated interest rate cut this year from their projections and indicated that a rate increase remained a possibility.

Additionally, the Commerce Department's Bureau of Economic Analysis revised first-quarter gross domestic product (GDP) growth sharply higher, reporting the U.S. economy expanded at an annualised rate of 2.1%, compared with the previous estimate of 1.6%.

Markets had expected the figure to remain unrevised.

The 0.5 percentage point upward revision largely reflected lower imports, particularly consumer and capital goods, which boosted overall growth. However, this was partially offset by a substantial downgrade to consumer spending, which accounts for more than two-thirds of U.S. economic activity.

Consumer spending growth was revised down to an annualised 0.5% from the previously reported 1.4%, reflecting weaker expenditure on services, including financial services, insurance and international travel.

Part of the downgrade to financial services spending was linked to the sharemarket sell-off during the quarter.

Consumer spending appears to have strengthened early in the second quarter, supported by sizeable tax refunds that have partly offset higher petrol prices resulting from the U.S.-led conflict with Iran.

Business investment remained a key driver of economic activity, fuelled by continued spending on artificial intelligence infrastructure. Investment in equipment increased at a 15.8% annualised pace, revised down from 17.2%, while spending on intellectual property products was revised higher to 13.8% from 11.6%.

Final sales to private domestic purchasers, which exclude government spending, trade and inventories and are regarded as a key measure of underlying demand, increased at a 1.7% annualised rate. That was revised down from the previously estimated 2.4%.

Corporate profitability also strengthened. Profits from current production rose at an annualised rate of $74.4 billion during the first quarter, significantly above the previous estimate of $40.4 billion, though below the $246.9 billion increase recorded in the fourth quarter.

Measured from the income side, gross domestic income expanded at an annualised rate of 1.2% during the January to March quarter, up from the previous estimate of 0.9%. Gross domestic income increased 1.6% in the fourth quarter.