The IEA has hung a multi-trillion-dollar figure on China's rare earth export controls and the expiry date buried underneath is the part that should worry anyone building a Western supply chain in the near future.

The International Energy Agency published its Global Critical Minerals Outlook late last week, and the headline number travelled a good deal faster than the analysis that produced it.

Full implementation of China's rare earth export restrictions would place about US$6.5 trillion of downstream production outside the country at risk, spread across automotive, high-tech, defence and energy manufacturing, with the U.S. and Europe absorbing close to half of that exposure between them.

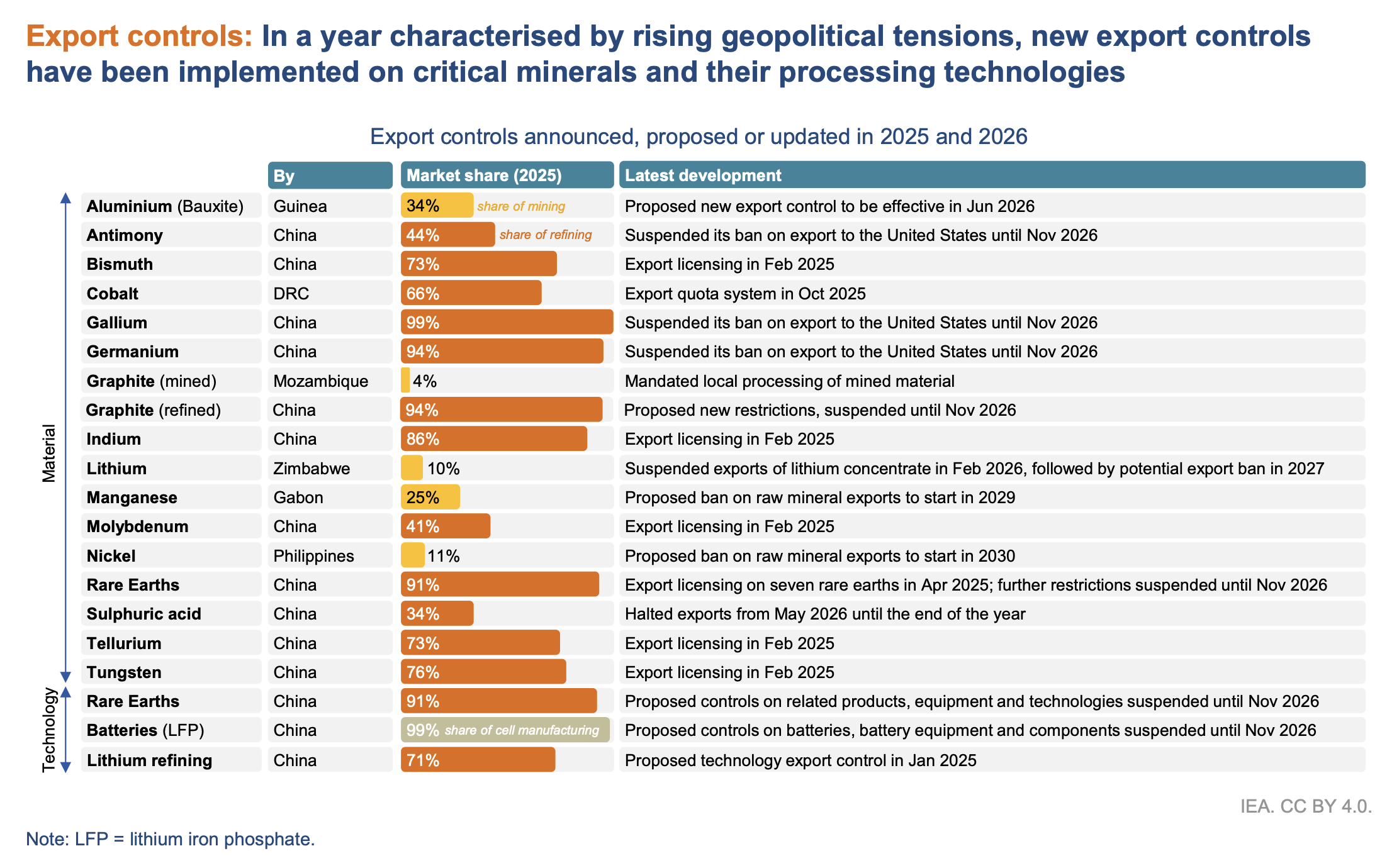

The date buried beneath that figure matters more, because Beijing widened its export controls in October last year, adding materials to the control list and layering on fresh licensing requirements, before agreeing to delay implementation for a full 12 months.

That suspension runs to 10 November this year, which leaves barely four months on the clock.

Nothing was repealed along the way, and the licensing architecture, the entity listings and the extraterritorial reach all stayed precisely where they were, with only the commencement date moving.

Markets have spent the intervening months treating the pause as a resolution, which is a defensible way to trade a quarter and a poor way to build an industrial base.

Rare earths are a group of 17 metals used in tiny quantities and effectively impossible to engineer around at short notice, embedded in cars, aircraft, electronics and weapons systems in amounts usually measured in grams rather than tonnes (t).

That asymmetry drives the entire exercise, and it explains why the value at stake runs so far ahead of the volumes involved.

The West received a year of grace, spent a considerable amount of public money, and shifted China's refining share by just 5%.

The agency's framing rests on the gap between physical volume and economic consequence.

"Vast amounts of economic value depend on relatively small volumes of critical minerals," IEA exec director Fatih Birol said.

The $6.5 trillion is an exposure estimate rather than a modelled loss, and the distinction is worth holding before anyone builds a forecast around it.

Graphite comes with a caveat of its own, as the agency warned that full implementation of separately announced and subsequently postponed controls could expose about $300 billion of downstream production beyond China's borders.

The country accounts for more than 90% of processed graphite output, which attaches a smaller number to an equally awkward chokepoint.

A pause, not a retreat

The October 2025 measures were modelled openly on Washington's foreign direct product rule, demanding a licence for foreign-made goods containing 0.1% or more of Chinese-origin rare earths, or manufactured using Chinese processing technology.

Both capitals stood down at much the same moment, with Beijing suspending its October package while the Bureau of Industry and Security parked its Affiliates Rule for a matching period.

The April 2025 restrictions on heavy rare earths were never touched, and the wider licensing regime has continued to bite through every stretch of nominal détente.

Enforcement has been sharpening rather than softening, with China adding 10 U.S. entities to its export control list in June, among them rare earths producers MP Materials (NYSE:MP) and USA Rare Earth (NASDAQ:USAR).

A separate MOFCOM announcement took effect on 1 July, formalising a mechanism that encourages organisations and individuals to report suspected breaches involving strategic minerals.

A country dismantling its leverage does not usually bother building a tip line for it.

Five points in three years

Public financing commitments for new critical minerals projects more than quadrupled between 2023 and 2025 to reach $65 billion, which sounds decisive until it meets a commissioning schedule.

Fresh refining capacity in the U.S. and Malaysia trimmed China's slice of the global rare earth refining market to 85% last year, down from 90% in 2023.

The agency reckons that figure could fall to 70% by 2035, provided planned projects proceed on time, and the conditional is carrying more weight than most of the sentences around it.

Its wider work cuts the other way, with the average market share of the top three refining nations across copper, lithium, nickel, cobalt, graphite and rare earths climbing to 86% in 2024 from around 82% in 2020.

Money to land down under?

Australia remains the most credible non-Chinese node in the chain, largely because Lynas Rare Earths (ASX:LYC) became the first producer outside China to turn out commercial quantities of dysprosium oxide at its Malaysian plant in May 2025, using feedstock from Mount Weld in Western Australia.

Iluka Resources (ASX:ILU) is building its Eneabba refinery on the back of an A$1.25 billion government-backed loan tied to allied offtake, and in June confirmed a binding four-year supply deal with an unnamed global automaker covering roughly 10% of the plant's planned output, worth a minimum A$155 million.

The remaining 90% of Eneabba's capacity still needs a buyer, which is the real test of whether a November restart tightens the non-Chinese order book or simply raises the price of finding one.

Lynas, for its part, has locked in 5,000t a year of NdPr with Japan's JOGMEC and Sojitz at the same $110/kg floor Washington uses for MP Materials, with up to 75% of its heavy rare earth output also committed to the Japanese market.

Washington's own answer has been a decade-long price floor of $110 per kilogram for MP Materials' NdPr output, alongside a $400 million equity injection that made the government the company's largest shareholder.

The free market's response to Chinese industrial policy turned out to be industrial policy, only with worse economies of scale and a slower permitting regime.

What to watch:

- 10 November 2026 - expiry of China's suspension of the October 2025 controls, and the single most important date in the sector.

- Licensing throughput - approval rates and volumes by destination are the real-time signal, not the rhetoric around them.

- Eneabba construction through H2 2026, where execution risk is concentrated.

- NdPr pricing against the $110/kg floor, which separates the policy-supported portion of the rally from the demand-driven one.