China has blacklisted the two American rare earth firms Washington funded to reduce its reliance on Beijing, in a move analysts have described as largely symbolic.

Azzet’s Mission Critical is a weekly column that lays out the ebbs and flows around critical minerals supply chains - from pricing, production, refinement and mergers & acquisitions, to energy, manufacturing and consumer products.

China's Ministry of Commerce added mining companies' MP Materials and USA Rare Earth to its export control list on 22 June, naming both alongside eight other American companies drawn from aerospace, drones, radar and shipbuilding.

The order bars Chinese suppliers from shipping dual-use goods to the listed firms, and extends further still by prohibiting any party, in any country, from passing Chinese-origin dual-use items to them.

Both producers anchor Washington's drive to build a rare earth value chain that routes around China, which is the detail that makes the designation worth parsing rather than waving through.

The two front-runners of American mineral independence have, in effect, been formally listed by the very country their public funding was meant to help them sidestep.

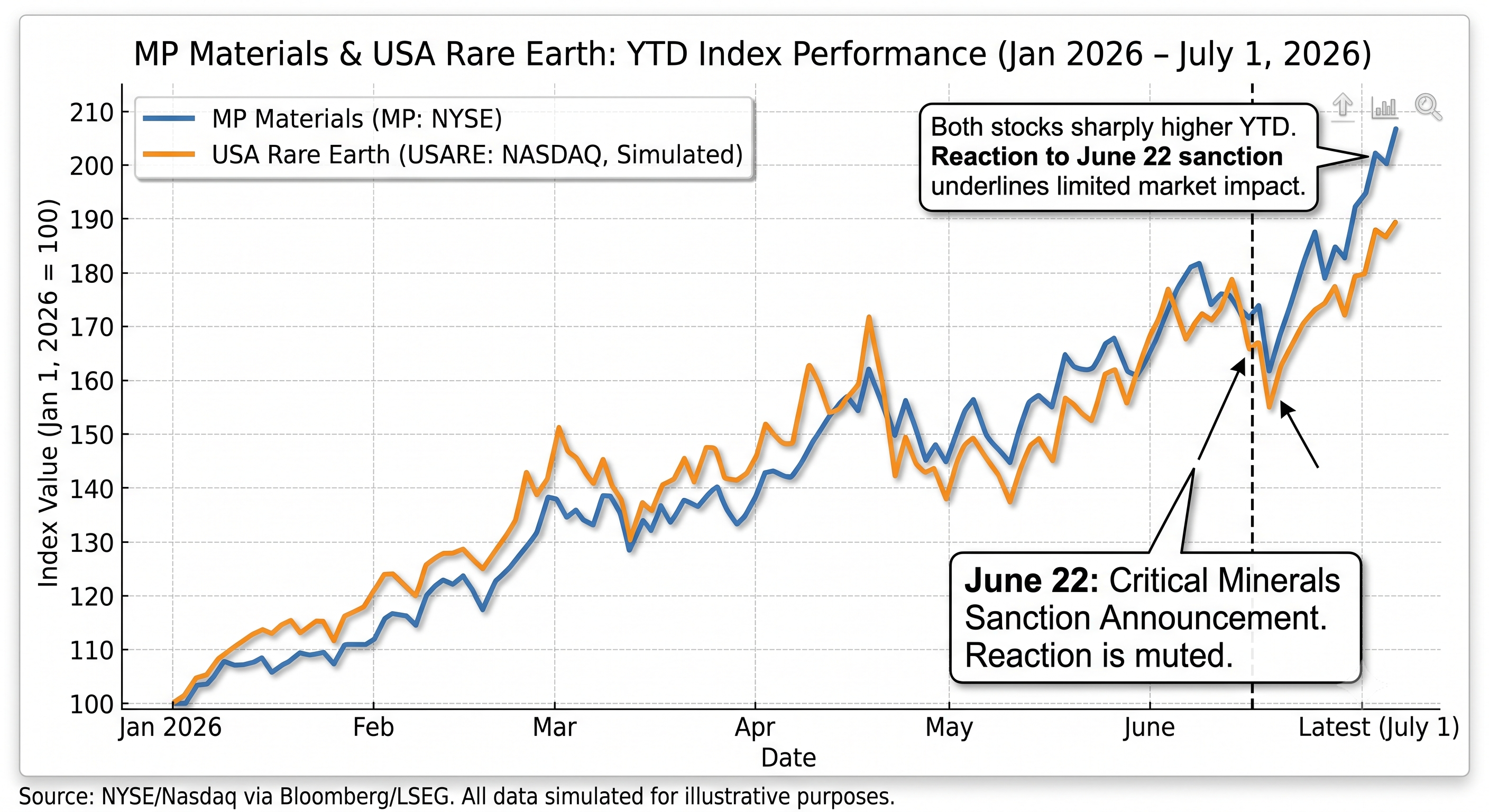

Trading reaction stayed contained, and several analysts read the curbs as a token response rather than a binding constraint, since both companies say they cut their reliance on Chinese equipment and feedstock some time ago.

A ban on receiving Chinese goods, on that reading, settles on firms that had already stopped placing the orders.

What the listing signals about Beijing's posture toward each new node of the parallel chain therefore matters more than the day's quotes, and the clearest pointer is the November expiry of China's suspended extraterritorial controls.

Token on the numbers

The consensus read is that the curbs carry more message than mechanism, and the figures behind them support the view.

George Chen of The Asia Group noted that the named entities are mostly U.S. defence players or government-linked outfits with no plans to trade in China, leaving the operational drag close to negligible.

Share prices tracked that logic, with MP roughly flat on the session and USA Rare Earth drifting modestly higher.

The measure is also entity-specific rather than a fresh blanket restriction on rare earth shipments, a distinction that shapes how it should be read.

Rather than tighten the broad controls, Beijing named individual firms in the manner of Washington's own entity-list method, and aimed the order at companies already shut off from Chinese trade.

A token measure need not be an empty one, and by listing the very enterprises designed to compete with it, China signalled that it will act promptly whenever Washington moves against Chinese firms.

The order followed by two weeks a Pentagon expansion of its roster of Chinese military-linked companies, a list that swept in names such as Alibaba, Baidu and BYD.

For a sector where confidence and capital carry much of the load, the reminder that Beijing is tracking each new entrant registers well beyond a single session's pricing.

Rivalry at home

The timing folded in a second storyline, because on the same day Beijing listed the pair, USA Rare Earth was in a Texas court filing its formal denial against MP Materials.

MP had sued its rival in May over the alleged theft of proprietary magnet technology by a former engineer, in a case still at an early stage.

The complaint centres on grain boundary diffusion, the process that lets manufacturers draw high performance from neodymium magnets while using less of the scarce heavy rare earths China controls.

According to the miner, a former employee carried its formulations across to USA Rare Earth, which calls the suit meritless and reads it as a deliberate attempt to slow its progress.

The quarrel marks where value concentrates in the business, since the prize lies in the processing knowledge that converts ore into a finished magnet rather than in the deposit itself.

Washington, meanwhile, has committed public money to both sides, putting US$400 million in equity into MP and signing a $1.6 billion funding agreement with USA Rare Earth.

China runs its own rare earth sector along opposite lines, coordinating output, pricing and export timing through the state as a single instrument.

Where exposure sits

Set the optics aside, and the genuine exposure rests on timing rather than on the contents of this week's order.

The strict extraterritorial controls China introduced in 2025 sit under a partial suspension that runs until 10 November, after which Beijing can reinstate a wider suite of measures through legal machinery it has already assembled.

Heavy rare earths are where any squeeze would register, because grain boundary diffusion leans on terbium and dysprosium, and China has recorded no shipments to Japan of either oxide since November 2025.

A step that reads as token against MP and USA Rare Earth today would change character entirely were Beijing to widen it to the heavy elements Western magnet-makers still cannot source at scale.

The leverage runs deep, since China accounts for roughly 60% of mined magnet rare earth output and above 90% of refining, with permanent magnet production near 95% on IEA figures.

Should the suspension lapse in November without a durable trade framework, the question shifts from whether named firms can buy Chinese equipment to whether anyone outside China can secure the heavy rare earths the strategy depends on.

Outlook

For now, Beijing has paired a pointed signal with deliberately light practical content, which leaves three paths open as the November deadline approaches.

- Base case: the June listing stays token and the named firms keep operating, with attention turning to whether the 10 November deadline brings escalation or extension while the parallel chain builds slowly and at high cost.

- Bull case for the West: the sanction and the lawsuit together sharpen focus, Washington deepens price floors and offtake guarantees, and the pressure nudges the two firms toward coordination rather than litigation.

- Bear case: the suspension lapses, China extends entity-style controls to heavy rare earth feedstock and equipment, and Western producers find that owning the mine and the magnet plant counts for little without terbium and dysprosium to run them.

What to watch:

- 10 November 2026, when China's suspended extraterritorial controls are set to expire and any trade flare-up could pull escalation forward.

- Heavy rare earth flows, terbium and dysprosium in particular, where the freeze on shipments to Japan stands as the template for wider enforcement.

- The litigation between MP and USA Rare Earth, and whether any court grants injunctive relief that disrupts USA Rare Earth's magnet ramp at Stillwater.

- Washington's next funding move, since the cadence of fresh equity stakes and price floors shows how hard the state intends to subsidise the parallel chain.

- ASX-listed exposure, with Lynas (ASX:LYC) the obvious non-China heavy rare earth bellwether and any separation-capable developer liable to rerate if November bites.