The Group of Seven leaders closed their summit at Évian-les-Bains on Wednesday by agreeing to set up a critical minerals alliance and a shared platform, handing the International Energy Agency an expanded role in flagging supply shocks before they bite.

The headline pledge was a number rather than a project, with leaders committing to cut reliance on any single supplier outside the bloc to below 60% for rare earths and permanent magnets by 2030, and towards 50% as soon as conditions allow.

Nobody named China in the communiqué, though the target leaves little doubt about which supplier the leaders had in mind.

"We express our grave concerns regarding the use of non-market policies and practices and economic coercion, including arbitrary export restrictions and retaliatory measures on critical minerals and their related dual-use items, all of which undermine economic security and resilience," the G7 leaders said in their joint declaration.

What's changed

Last year's framework, launched at Kananaskis under Canada's presidency, dealt mostly in principles, traceability and a roadmap towards what officials labelled standards-based markets for critical minerals.

The Évian text goes considerably further, attaching a quantitative goal, harmonised stockpiling and a standing mechanism for sharing data and coordinating crisis response through the IEA.

A first round of pilots will cover lithium and nickel, before the arrangement expands to five additional minerals each year with rare earths treated as the clear priority.

"We agreed in various formats to work even more closely together on critical raw materials. We had very in-depth discussions with our guests about how we can diversify," German Chancellor Friedrich Merz told reporters in Évian.

The money behind the rhetoric sees member countries having announced 195 projects worth a combined US$74 billion since the start of 2026.

That builds on the production alliance unveiled last October, which mobilised $6.4 billion across 26 partnerships spanning graphite, rare earths and scandium.

On stockpiling the bloc is already moving, with the United States standing up a $12 billion reserve and the European Union assembling its first joint stockpile of tungsten, rare earths and gallium.

Interventionism and lofty targets

Leaders also cracked open the door to price-gap subsidies, joint procurement, quotas and price floors, the kind of interventionist instruments several members had previously treated with suspicion.

Tellingly, they stopped short of binding price-floor commitments, reflecting allied unease about Washington's enthusiasm for regulating mineral prices outright.

China still refines close to 90% of the world's rare earths and mines roughly 70% of the raw material, a chokehold assembled patiently over several decades.

Japan offers a sobering precedent, having spent 15 years diversifying since Beijing's 2010 export squeeze yet still drawing about three-quarters of its rare earths from its neighbour.

The gap between intent and delivery is where the analysts park their scepticism.

"The G7 statement is an important signal of intent, but the pace of diversification will ultimately depend on whether policy support translates into investment across the midstream and downstream parts of the value chain," Benchmark Mineral Intelligence research manager Neha Mukherjee told Reuters.

That midstream point is the whole game, because mining ore outside China is the easy bit while separating and refining it into usable oxides and magnets is where Beijing's lead is widest.

Where the pain lands

Mukherjee has put the dependency in starker terms before the summit ever convened.

"The problem is that the entire world is now structurally dependent on China," she warned in October, as Beijing's controls bit.

"If you want a secure supply chain, diversify your sources as much as possible."

She has also been blunt about which industries wear the consequences when shipments stall.

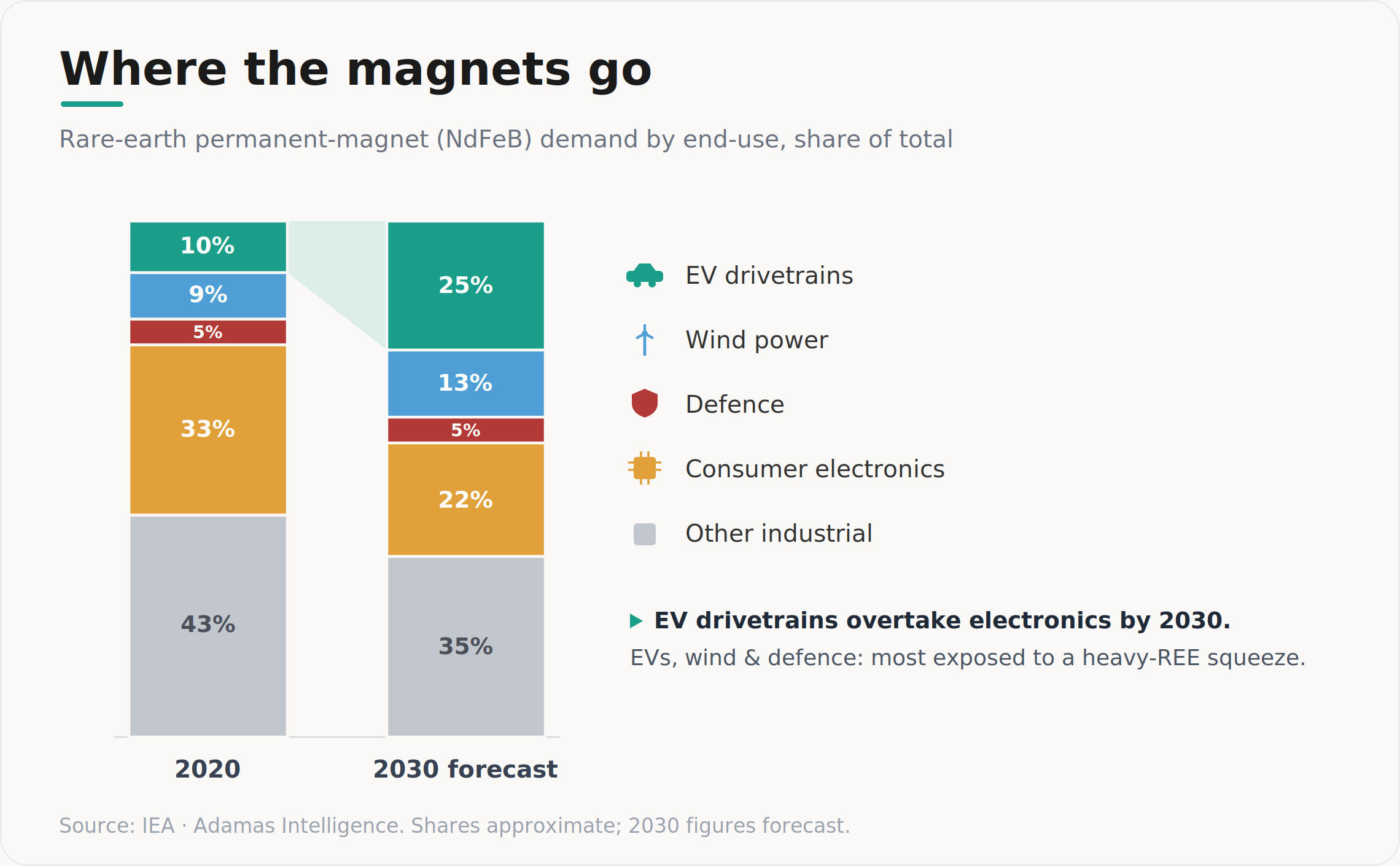

"Defence is going to be affected the most; e-mobility is also going to get hit. Consumer electronics and robotics, too, will be affected," Mukherjee said.

The cost of buying outside China is already visible in the price, with Benchmark's own data showing dysprosium oxide landed in North America at 4.4 times the Chinese domestic price during 2025, a gap the firm expects to widen to roughly 8.3 times by 2027.

That widening spread is precisely why price floors and subsidies keep resurfacing in G7 corridors, even as several members flinch at the cost.

An imminent test arrives in November, when China's one-year suspension of its toughest October 2025 export controls is scheduled to lapse.