Since December 2025, China has been running what amounts to a quiet rare earth blockade against Japan - not through formal diplomatic announcements, but through the systematic withdrawal of the materials that underpin everything from electric vehicle motors to missile guidance systems.

Exports of dysprosium, terbium, yttrium oxide and gallium to Japan have all but stopped, confirmed by Reuters this week - five months of near-zero shipments, with Chinese customs data recording only trace yttrium volumes crossing the border in that time.

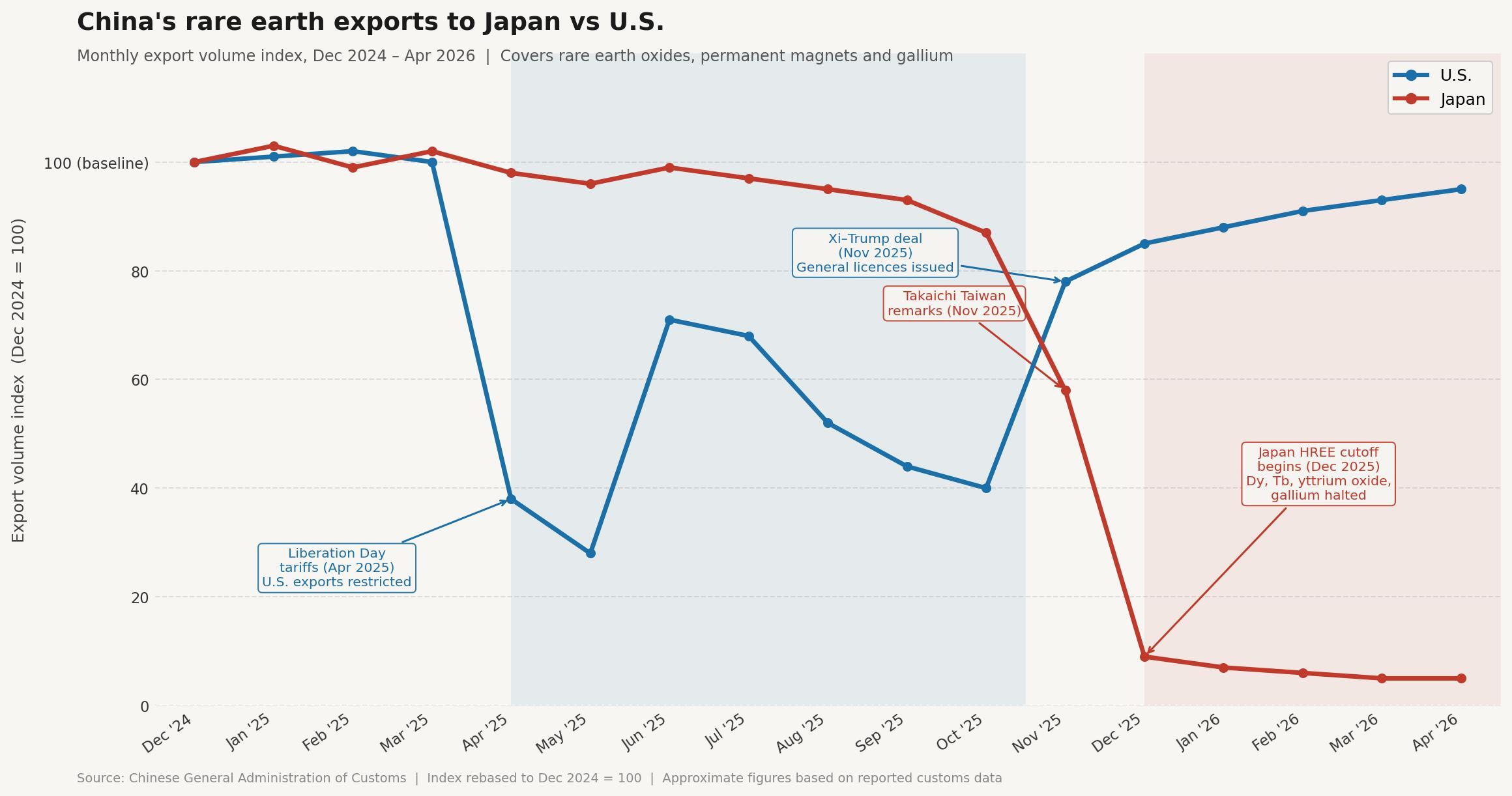

The trigger is well-documented: Prime Minister Sanae Takaichi publicly signalled that Tokyo could respond militarily if China moved on Taiwan, and Beijing activated the export controls it has spent years quietly building into enforceable law.

Japan imports roughly 70% of its rare earths from China according to the Yomiuri Shimbun - improved from near-total dependence in 2010 after years of costly diversification investment, though still far short of any position that can absorb a sustained cutoff of its highest-value inputs without industrial consequence.

Not 2010 - something more deliberate

So how does 2026 differ from the last time Beijing ran this play?

The short answer is that it is more deliberate, more precisely targeted, and built around a regulatory architecture that leaves little room to argue the disruption was anything other than intentional.

What separates this episode from the Senkaku spat is not scale but the surgical nature of its targeting, with Beijing formalising the restrictions within a codified regulatory framework in January before tightening controls twice more in February - specifically naming the shipbuilding and aero engine divisions of Mitsubishi Heavy Industries.

Those are not trade restrictions in any conventional sense; they are a supply chain scalpel drawn across the precise contours of Japan's defence-industrial base.

The 2010 episode, which permanently reset how governments thought about single-source mineral exposure, was arguably partly administrative in origin, with CEPR/VoxEU analysis later questioning whether a deliberate and sustained embargo ever fully materialised - a historical ambiguity the 2026 version plainly does not share.

Permanent magnet exports to Japan did nudge 2.5% higher in April month-on-month, according to Chinese customs data released in May, but that partial recovery followed a 17.3% collapse in March, leaving cumulative volumes well below anything Japanese manufacturers were running their forward order books against.

Major magnet producer Shin-Etsu Chemical has already halted new order acceptance for dysprosium-containing magnets, per a Reuters industry source - a move analysts at Project Blue flag as a leading indicator of upstream strain working its way through the production chain.

Arithmetic

Japan has been preparing for exactly this scenario since 2010, through strategic stockpiles, financial backing for alternative producers and engineering work to reduce HREE intensity in magnet designs - and yet when you look at the actual production numbers, the preparation still falls well short of what the current cutoff demands.

Australia's Lynas Rare Earths (ASX: LYC) - the world's only significant commercial producer of separated dysprosium and terbium outside China - produced ~8 tonnes of those two materials combined across the entire first quarter of 2026, against China's roughly 14 tonnes shipped to Japan alone every month throughout 2024.

The world's most strategically critical non-Chinese HREE producer cannot cover a single country's monthly import requirement across a full quarter of output, and Japan is only one of several allied nations currently drawing down stockpiles with no near-term path to meaningful replenishment.

Mitsubishi Motors disclosed in February that it had secured rare earth supply only through mid-year, a deadline now closing in without visible diplomatic progress.

Recently, Japan's Trade Minister Ryosei Akazawa managed a brief, unscheduled exchange with his Chinese counterpart at this week's APEC ministerial - notable mainly because it represents the most senior Japanese contact with Beijing since the restrictions took hold, rather than any indication of substantive movement.

Washington gets different terms

Now consider what has been happening on the other side of the Pacific during the same period.

While Japan has been cut off for five months, Washington has been operating under a partial reprieve courtesy of the Xi-Trump trade agreement finalised in late 2025, under which Beijing agreed to suspend its expanded rare earth export controls and issue general licences covering materials it had restricted earlier that year - a normalisation that holds until at least November 2026.

Beijing then introduced the Japan-specific restrictions within weeks of signing that agreement.

The sequencing tells you more about China's strategic thinking than any policy document could, with Washington receiving managed détente because extended mutual disruption carries real economic cost on both sides of the Pacific, while Japan is frozen out on explicitly geopolitical grounds - Beijing having decided the commercial cost of cutting a major HREE customer is worth the diplomatic leverage it generates over Taiwan.

Washington's own critical minerals effort is meanwhile generating its own internal friction, with an US$80 million conditional loan to rare earths refiner ReElement Technologies being reconsidered by the Pentagon - part of a broader $1.4 billion package alongside Vulcan Elements - after officials raised questions about the company's ability to scale its processing technology, setting off a public dispute with the White House over whether speed or scrutiny should take priority in a supply chain race the West is already running behind on.

Watchlist:

- Japan's stockpile runway remains opaque - government reserve volumes are classified - making Shin-Etsu's order freeze and Mitsubishi Motors' mid-year supply horizon the two clearest real-time indicators of how quickly the squeeze is feeding through to production.

- Lynas's Kalgoorlie processing ramp and heavy rare earth separation throughput at its Malaysia facility, which together determine how much volume the world's most strategically positioned alternative producer can actually deliver and when.

- Iluka Resources (ASX:ILU) Eneabba rare earths refinery, targeting commissioning in 2027 and designed specifically to produce separated dysprosium and terbium - a project sitting directly in the structural path of this demand shift.

- A Pentagon decision to scrap the ReElement loan would signal that U.S. institutional capacity to channel public capital into pre-commercial rare earth processing is less advanced than headline investment figures suggest.

- Whether diplomatic contact between Akazawa and Beijing produces any measurable easing before Mitsubishi Motors' mid-year supply window closes.