Global gold demand reached a record value in the first quarter of 2026, as surging prices and geopolitical uncertainty reshaped investor behaviour, with Asian buyers leading a decisive shift towards physical bullion.

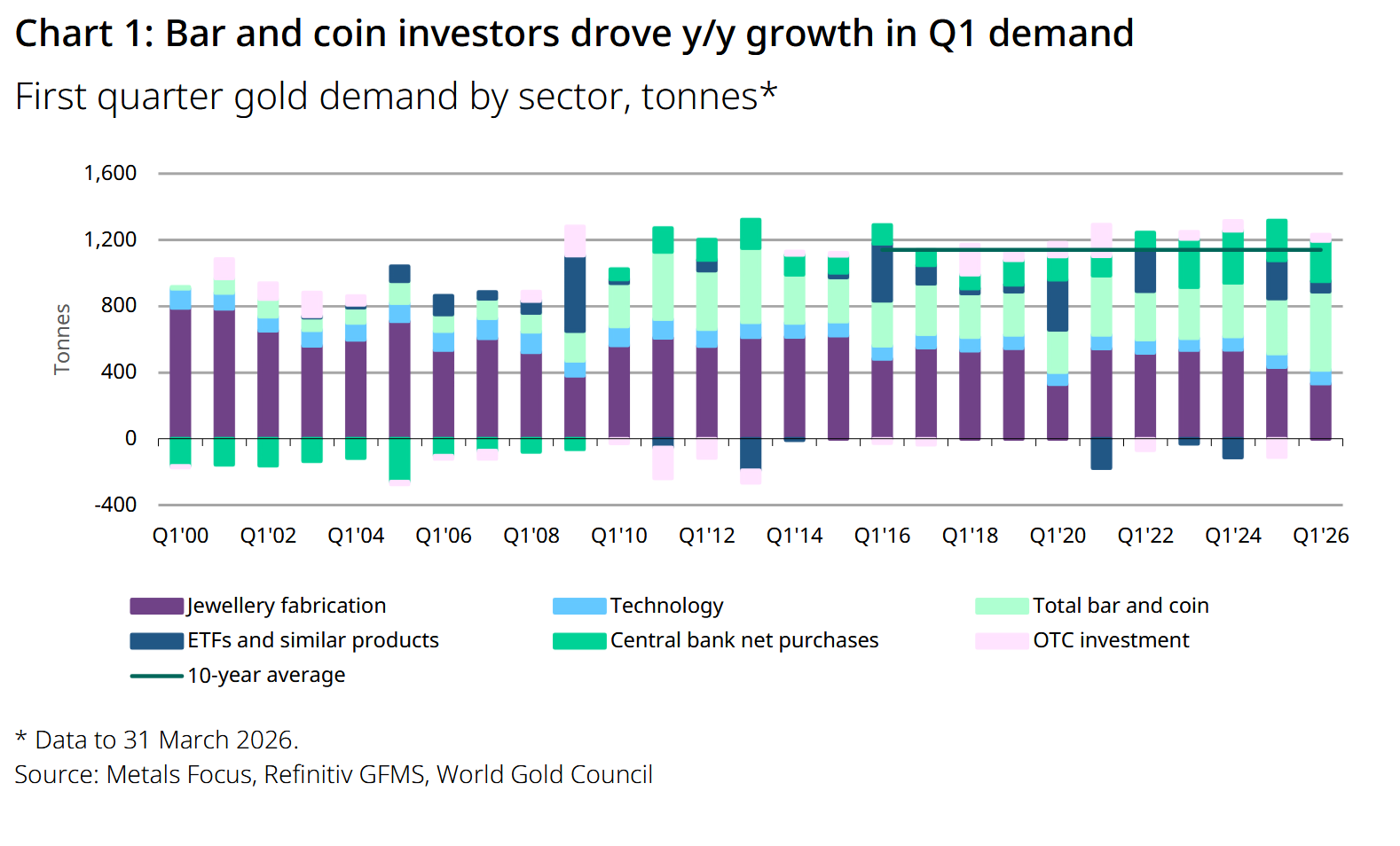

According to the World Gold Council’s Gold Demand Trends report, total demand, including over-the-counter trading, rose 2% year-on-year to 1,231 tonnes.

However, the modest increase in volume masked the impact of a sharp rally in prices, which drove the value of demand up 74% to an all-time high of US$193 billion (A$269.2 billion).

At the centre of this surge was a dramatic rise in bar and coin investment. Demand for physical gold products climbed 42% to 474 tonnes, marking the second-highest quarterly level on record.

The increase was overwhelmingly driven by Asian investors, who continued to accumulate bullion despite record-high prices.

Regional Divergence in Investor Behaviour

This divergence in behaviour between regions became one of the defining features of the quarter. While Asian retail investors aggressively bought physical gold, Western institutional investors showed more caution.

United States-listed gold exchange-traded funds recorded significant outflows in March, reversing earlier inflows and limiting total ETF demand growth to a net increase of 62 tonnes for the quarter.

The split reflects fundamentally different investment frameworks. Western investors, focused on real yields and opportunity costs, reduced exposure as bond returns remained elevated.

By contrast, Asian buyers appeared more concerned with preserving long-term purchasing power amid persistent inflation and geopolitical instability.

This dynamic has historical significance. Periods in which physical demand strengthens while paper gold flows weaken have often marked structural turning points in the gold market, suggesting that current trends may have longer-term implications.

Central Banks Maintain Strong Buying

Central banks remained another key pillar of demand. Net purchases totalled 244 tonnes in the quarter, up 3% year-on-year, extending a sustained period of official sector buying.

Despite some increase in selling activity, the broader trend reflects continued efforts by central banks to diversify reserves and hedge against macroeconomic and geopolitical risks.

The World Gold Council expects full-year purchases to remain robust, in the range of 700 to 900 tonnes.

Jewellery Demand Weakens on High Prices

In contrast, jewellery demand continued to struggle under the weight of high prices. Global consumption fell 23% year-on-year to around 300 tonnes, the lowest level since the pandemic-era downturn.

Yet, in a pattern seen across multiple markets, the value of jewellery demand rose 31% to a record US$47 billion for a first quarter, as consumers paid more for lighter or lower-carat items.

China and India illustrated this trend clearly. In China, jewellery demand dropped 32% year-on-year to 85 tonnes, pressured by high prices, weaker consumer confidence and tax changes.

However, spending still rose 16% to US$13 billion, highlighting the resilience of underlying demand. Consumers increasingly shifted towards smaller pieces or investment-style products to manage costs.

In India, demand also softened in volume terms but remained resilient in value, reaching a record US$10 billion for the quarter. Buyers continued to favour lighter-weight and lower-carat jewellery, while some shifted towards bars and coins due to their lower premiums.

Across the Middle East and Turkey, jewellery demand volumes declined sharply amid record prices and regional conflict, although total spending rose significantly.

In Western markets, including the United States and Europe, high prices and tariffs weighed on affordability, leading to reduced purchase frequency and a shift towards lighter items.

Australia Sees Shift to Physical Bullion

Australia followed the global pattern but showed a notable tilt towards physical investment. Bar and coin demand rose 23% year-on-year to 3.9 tonnes, outpacing inflows into gold-backed ETFs, which totalled 1.9 tonnes.

This marked a reversal from previous trends and pointed to growing preference among Australian investors for direct ownership of bullion.

“Australian investors continued to allocate to gold during the March quarter, adding 3.9t in bar & coins, a 23 per cent year-on-year increase. Notably, this was twice the 1.9t added to gold-backed ETFs, a divergence from Q1 2025 when bar and coin demand rose 3.1t compared to 2.8t for ETFs,” Shaokai Fan of the World Gold Council was quoted as saying in an Investor Daily article.

“While this suggests that more investors have opted to own and store physical gold year-to-date, a traditional response to intensifying geopolitical risks, the broader trend is that Australian investors continue to defy historically high prices and elevated volatility by adding more gold to their portfolios, affirming its role as a long-term safe haven, diversifier and hedge against inflation and slower economic growth.”

On the supply side, mine production rose modestly and is expected to increase further in 2026 as high prices improve margins. However, structural challenges, including permitting, financing and energy constraints, are likely to limit the pace of expansion.

Recycling activity has also begun to pick up, but remains constrained by expectations of further price gains and limited near-market supply.

Demand for gold in technology applications edged 1% higher to 82 tonnes, supported by ongoing growth in artificial intelligence infrastructure.

Looking ahead, the World Gold Council expects geopolitical tensions, inflationary pressures and elevated interest rates to remain central drivers of the gold market.

While ETF demand may moderate compared with 2025, strong bar and coin investment, particularly in Asia, is expected to continue underpinning overall demand.

Central bank buying is also forecast to remain solid, reinforcing gold’s role as a strategic reserve asset. At the same time, high prices are likely to keep jewellery volumes under pressure, even as spending remains resilient.