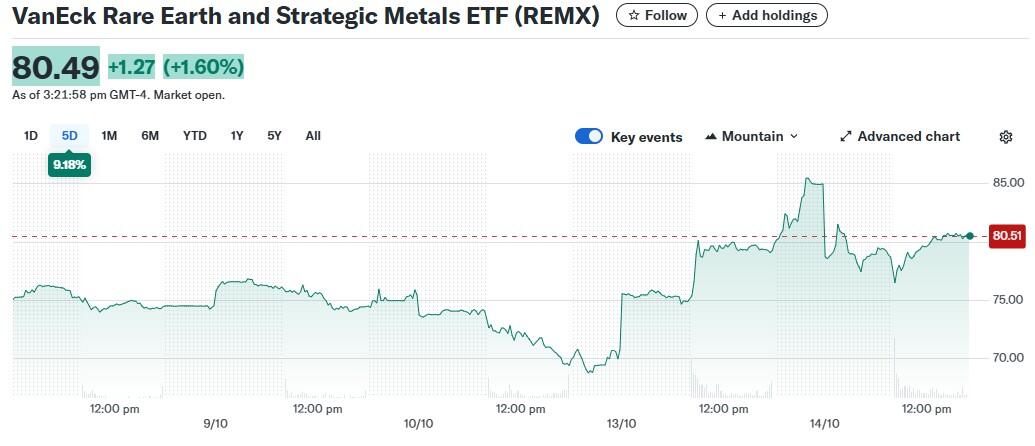

Wall Street has responded to China again tightening rare earths exports by launching every stock associated with that name into absolute orbit, leading to fears of an overbought sector. I thought I'd take a quick squizz at some notable rare earths stocks that have been posting huge price gains this past week or so and suss out their mettle.

Azzet’s Mission Critical is a weekly column that lays out the ebbs and flows around critical minerals supply chains - from pricing, production, refinement and mergers & acquisitions, to manufacturing and consumer products.

Backed by Aussie businessman Tony Sage, the +$2 billion Critical Metals Corp (NASDAQ : CRML) soared 55% in a single day, while USA Rare Earth - burning US$142 million a year with no sales revenue - rocketed 94% in just five weeks to all-time highs.

Then there's Verdis Minerals, which nobody had heard of six months ago, somehow managing to climb 401% this year without significant news apart from China headlines and general momentum.

“The rare earths market is notoriously opaque and volatile,” Bank of America Global Research said in a note.

"We often see stock prices for junior explorers move 20-30% on the back of drill results that are still years away from commercial reality.

"Investors need to distinguish between near-term producers with cash flow and the more speculative, high-risk exploration plays."

Building rare earths mines takes longer and costs more than anyone expects, especially the extraction and processing methods.

Exactly four Western companies are actually producing commercial-grade oxides right now, and two barely matter in the scheme of things.

The Producers

Lynas Rare Earths (ASX: LYC)

Lynas is up 203% since January, with a market cap now over $20 billion - triple where it started the year on basically the same business run rates.

They operate Mt Weld in Western Australia and a Malaysian processing facility, churning out 3,212t in Q4 FY25 as the only major non-Chinese producer.

Revenue hit A$556.5 million, but net profit was just A$8 million, which means they're trading at 37 times sales when fair value sits around 3.8 times.

If China floods the market or Malaysia gets difficult about environmental permits - both have happened before - the valuation gets rewritten fast.

MP Materials (NYSE: MP)

MP Materials jumped 24.1% to $93.50 after already quintupling for long-term holders.

They operate Mountain Pass in California, pumping out 40,000t of rare earth oxides annually, or ~11.5% of global supply, with unique Department of Defense backing.

The Department of Defence invested $400 million for a 15% stake and secured a 10-year price floor of $110/kg.

General Motors committed to buying 1,000t from the Texas magnet facility starting late 2025, and the 10X plant aims for 10,000tpa by 2028.

Every possible good news catalyst has already materialised and been priced into the stock immediately.

Energy Fuels (NYSE: UUUU)

Energy Fuels is up 16% on China news while actually delivering 850-1,000tpa of NdPr at White Mesa Mill in Utah right now.

They produced the first kilogram of 99.9% pure dysprosium oxide in August 2025, making them the first U.S. company with proven heavy rare earth capabilities.

They're a uranium company that figured out rare earths, giving them two critical mineral revenue streams when everyone else has one.

Commercial heavy rare earth operations hit Q4 2026, and if they greenlight their Australian Donald Project, that adds 129tpa samarium, 16tpa terbium, 92tpa dysprosium.

They lost $47.84 million on $78.11 million in revenue in 2024, so uranium exposure comes with the rare earth story, whether investors want it or not.

Australian Strategic Materials (ASX: ASM)

ASM jumped 67.65% in a single day with a 42% monthly surge despite being the only ASX company actually delivering rare earth alloys in Korea right now.

Their Korean Metals Plant delivers 1,300tpa of NdFeB alloy, which is real output while everyone else is still building PowerPoints.

They have conditional letters of interest for US$600 million from US EXIM, A$400 million from EDC, and A$200 million from Export Finance Australia for Dubbo.

None of that funding is binding, and auditors flagged "material uncertainty" over going concern in recent filings.

The Korean plant is real but small, and Dubbo has been shovel-ready for years without securing binding commitments from major lenders.

Billions in spending, output pending

Iluka Resources (ASX: ILU)

Iluka jumped 15.76% in October after more than doubling recently on a $1.7-1.8 billion refinery at Eneabba that's 30% complete and aiming for 2027 commissioning.

The Australian government backed them with $1.65 billion in non-recourse loans plus another $400 million, which is unprecedented support for strategic infrastructure.

The project was approved at $1.2 billion in 2022 and has already blown out 50% before they're even halfway done.

Projected NPV ranges from $869 million to $3.37 billion, depending on feedstock scenarios.

They're building Australia's first rare earth refinery after costs already exploded, while needing to secure third-party feedstock they don't currently have.

USA Rare Earth (NASDAQ: USAR)

USA Rare Earth climbed 94% in five weeks to hit $37.85 from a March low of $5.56, which is a seven-bagger for a company with zero revenue.

They built a 310,000 sqft magnet facility in Stillwater, aiming for 5,000tpa with first commercial shipments scheduled for Q1 2026.

The explorer posted a $142.7 million net loss in Q2 2025 versus $2.8 million a year earlier while sitting on just $128.1 million cash.

Their Round Top mine in Texas isn't delivering yet and needs $350 million to get operational, so they're currently buying feedstock from South Korea instead.

Cash burn is accelerating from $4 million per quarter last year to $7.9 million now, while the mine remains firmly in pre-development mode.

Arafura Rare Earths (ASX: ARU)

Arafura jumped 27% in October and is up 150% since January despite being "shovel-ready" for nearly two years without actually starting work.

They have almost $1 billion in debt financing secured, offtake agreements with Hyundai, Kia, and Siemens Gamesa, plus all permits for the Nolans Project.

They still need about $100 million more equity to close their funding gap, which remains the missing piece keeping shovels out of the ground.

Meteoric Resources (ASX: MEI)

Meteoric's Caldeira Project in Brazil contains 1.1 billion tonnes at 2,413 ppm TREO, making it the world's largest ionic clay rare earths deposit.

Ionic clay deposits are dramatically easier to process than hard rock, using simple ammonium washing with no tailings dams and lower capital costs.

They completed their Pre-Feasibility Study in 2025, are building a pilot plant now, and secured inclusion in Brazil's $1.4 billion strategic minerals program.

Meteoric received a cash injection of $42.5 million from U.S. funds in July. Caldeira's preliminary permits are expected soon, and installation licences are targeted for mid-2026.

Brazilian permitting, pilot plant success, and project economics all need to prove out two to three years before actual output starts.

Four companies are delivering rare earths right now - Lynas, MP Materials, Energy Fuels, and ASM at a small scale - and that's the entire Western supply base.

Iluka, USA Rare Earth, Arafura, and Meteoric will probably ship material between 2026-2028 if construction doesn't blow out and capital materialises when needed.

Everyone else - NioCorp, Critical Metals, and the rest - might eventually deliver something, but they're realistically five to ten years away if they ever survive that long.