Asia keeps reaching for more gas. Someone should probably tell them how that's been going.

Here's a fun game…

Take the world's biggest energy-importing region, subject it to repeated geopolitical supply shocks, watch prices detonate, and wait for policymakers to respond by locking in more of the same fuel that caused the problem in the first place.

Rinse and repeat.

That, in broad strokes, is the story the Institute for Energy Economics and Financial Analysis (IEEFA) has just documented across Japan, South Korea and Thailand in its March 2026 Asia energy research roundup.

The IEEFA's core argument is simple and genuinely hard to argue with: Building more gas infrastructure doesn't fix exposure to global gas price shocks, it deepens it.

It makes for pretty uncomfortable bedtime reading if you're an energy security hawk, or, you know, a taxpayer in any of those countries footing the bill for imported fuel at crisis prices.

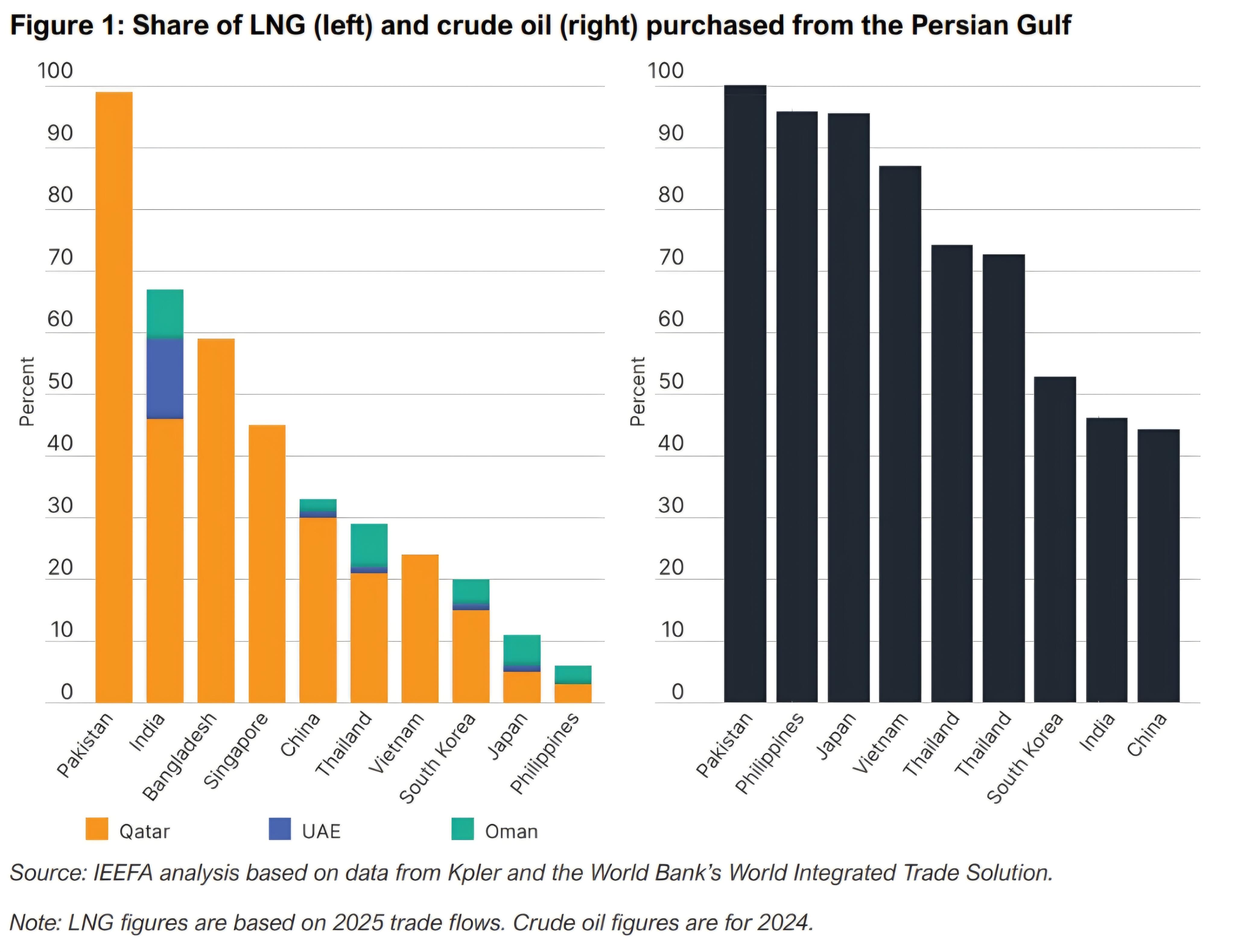

Iran lights the match, Asia buys more petrol

The Iran conflict has been doing what Middle East supply disruptions always do: sending energy markets into a spin and making the renewables argument look increasingly obvious.

IEEFA analysts put it plainly - fiscal backstops and monetary buffers can absorb a price shock temporarily, but the only thing that actually resolves the problem is structurally reducing exposure to imported fuel in the first place.

Straightforward enough thesis, and what's less straightforward is why three of Asia's biggest economies have spent the past 18 months doing the exact opposite.

Japan: An arbitrage strategy

Let's start with Japan, which has quietly pulled off one of the more impressive pivot moves in global energy markets - just not in the direction you'd hope.

Domestic LNG consumption has fallen nearly 20% since FY2018, thanks to nuclear restarts and growing renewables penetration.

Rather than wind back procurement commitments to match that declining demand, Japanese utilities and trading houses simply redirected surplus cargoes to overseas buyers instead.

In FY2024, 40% of all LNG volumes handled by Japanese companies were flicked to foreign markets - up from just 16% in FY2018, per the Japan Organisation for Metals and Energy Security (JOGMEC).

To put that in perspective, Japan resold more LNG in FY2024 than Russia - the world's fourth-largest LNG exporter - produced across the same period.

That's a bold arbitrage position, and one that depends entirely on global prices staying elevated enough to maintain margins, which gets trickier by the quarter as record export capacity floods the market through 2026 and beyond.

In February, power utility JERA doubled down by locking in 3 million tonnes per annum of LNG from QatarEnergy through 2054 - the largest Japanese offtake deal in a decade and one that expires well past Japan's own net-zero target date of 2050.

Make of that what you will.

And Japan's clean energy credibility takes a further knock when you pull up the battery storage numbers.

BESS project applications have surged from 70 gigawatts (GW) to 170.8GW since mid-2024, reflecting genuine investor appetite for grid-scale storage.

The amount of that capacity actually connected to the grid, however, sits at a rather underwhelming 0.62GW.

That's a chasm of roughly 275X between what's queued and what's plugged in, driven by grid interconnection bottlenecks, policy flip-flopping mid-procurement cycle, and battery system costs running 2.5-3X above global benchmarks.

South Korea's balloon problem

South Korea pledged at COP30 to retire 40 of its 61 coal-fired power plants by 2040, which sounds like a serious climate commitment until you look at what's filling the capacity gap left behind.

IEEFA calls it the balloon effect: squeeze coal output and gas-fired generation swells to compensate, which is exactly what unfolded between 2017 and 2023 when coal generation fell 23% while gas-fired output rose 25%.

Total power-sector CO2 emissions over that same stretch still climbed 6%, reaching 256 million tonnes in 2023 - suggesting the coal phaseout, as currently constructed, is less a decarbonisation strategy and more emissions relabelling with extra steps.

There's also a new commercial sting in the tail, with the EU's Carbon Border Adjustment Mechanism having started levying tariffs on embedded-carbon imports from 1 January 2026.

South Korea's LNG-heavy semiconductor and AI data centre supply chains are now accruing a real, measurable cross-border trade cost every time they sell into Europe.

Thailand: Overbuilt, still building

Thailand's situation is, frankly, the easiest to explain.

The country's gas-fired power fleet is already running well below capacity, the Electricity Generating Authority of Thailand cancelled three separate project tenders in 2025, and nearly every other proposed scheme is running behind schedule - yet the government still plans to commission 6.3GW of new gas capacity by 2037.

Rising LNG import costs and escalating capital expenditure are eroding project economics before a single turbine fires up, which raises the fair question of whether Thailand's power planning assumptions have caught up with the energy market that actually exists in 2026.

Apparently not yet.