The intensifying war between the United States-Israel and Iran appears to put a halt to the strong momentum experienced in the A$ credit market issuance, which has been experiencing record-breaking activity into early 2026.

The notable hull in Australian credit markets follows record issuance and strong performance in 2025, when the A$ bond market saw total issuance of around A$320 billion, nearly reaching the all-time high of A$324.66 billion set in 2024.

The notable downturn since the Iran war began marks a severe "flight to safety", with investors favouring cash over riskier corporate debt amidst soaring oil prices and intense uncertainty.

However, the one issuance that did get away amid the chaos was the recent pricing of a small $40 million increase from MAFG Finance, the finco arm of MA Financial (ASX: MAF), to its existing 8% senior unsecured notes maturing 30 March 2029.

The notes are unrated, carry an 8% coupon, and are non-callable until 30 September 2026.

Pipeline of deals

Subject to market conditions, NEXTDC (ASX: NXT) - which has flagged plans for a subordinated notes offering (NextDC Notes IV) to fund its data centre capacity pipeline - will be joining a long queue of issuers ready to tap the A$ market with a string of mandates announced in recent days.

In other words, there is a pipeline of upcoming corporate or government debt issuance deals that have been officially assigned to investment banks but have not yet been launched to investors.

However, in contrast to the strength witnessed over the past few years, BondAdviser suspects any transaction is likely to include a concession to buffer to entice investor appetite amidst current market gyrations - especially given the queue is dominated by corporate issuers.

“While a reopening of the primary market is typically led by high-grade issuers before moving down the rating spectrum, offshore issuance last week demonstrated even high-quality transactions required a >20bps premium to secondary curves,” the bonds and fixed income specialist noted.

Higher rates

In layman's terms, this means that even the most "reliable" borrowers - like stable, big-name companies - are having to pay much higher interest rates than usual to convince people to lend them money right now.

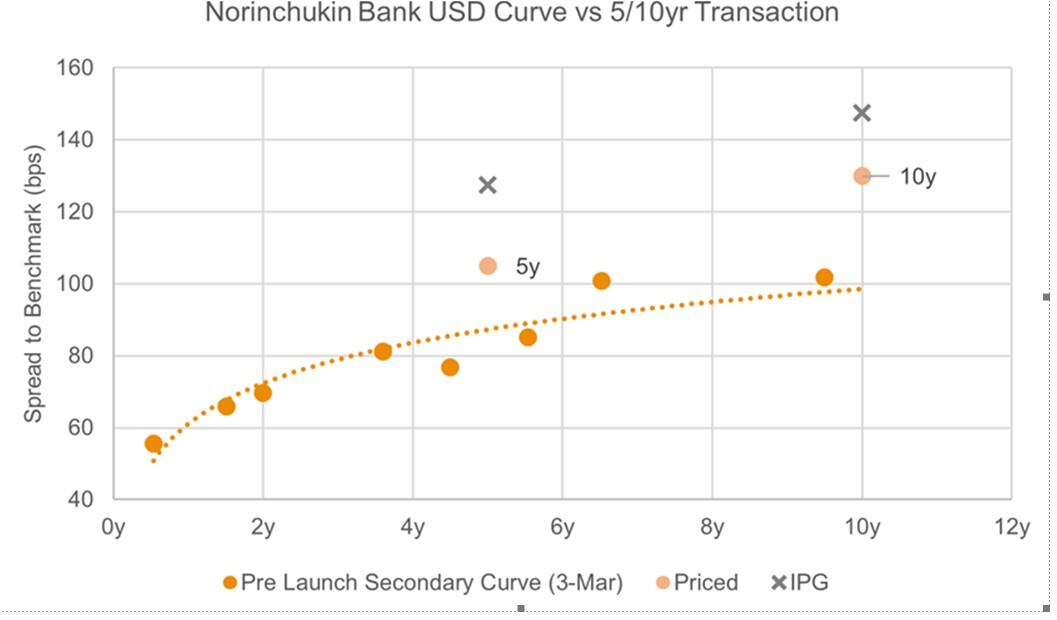

This became evident within Norinchukin Bank’s - a Japanese cooperative bank - 5/10-year US$ transaction last Tuesday, as the first major US$ print following the Iran war that came 20-30bps to the pre-launch secondary curve despite being rated A/A1.

In other words, Norinchukin Bank had to pay a much higher "interest premium" than expected to borrow money in the U.S. bond market due to increased global tension.

Norinchukin was the first big company to issue new bonds (a "print") in the U.S. market immediately after the start of a conflict with Iran, and with investors feeling yippy, they demanded a higher return for their risk.

In this context, BondAdviser notes that NBN Co’s 10-year sustainability transaction has launched IOIs (Indication of Interest) at a 20bp premium to the A$ NBN curve.

Last Thursday, Commbank (ASX: CBA) had its Issuer Default Rating (IDR) upgraded to AA (Stable) from AA- by Fitch, reflecting an increase in the bank’s Viability Rating (VR) – that measures intrinsic creditworthiness - to AA- from A+.

After revising its outlook on the bank to Positive in March last year, Fitch cited the bank’s peer-leading earnings profile, strong franchise strength and robust capital and asset quality metrics as drivers of the result.

The upgrade leaves Commbank rated one notch above its major bank peers at Fitch, both at the senior unsecured (AA vs AA- for peers) and Tier 2 levels (A vs A- for peers).

Nevertheless, secondary markets continue to price CBA broadly in line with the other majors, with Tier 2 spread differentials remaining unchanged since the update.

“In our view, this reflects investors’ tendency to treat the Australian majors as a largely homogenous cohort, given their similar regulatory settings, systemic importance and capital profiles,” BondAdviser.

Pacific National Outlook Revised to Stable by S&P

A week ago, S&P released a note revising Pacific National’s outlook to Stable/BBB- from Negative/BBB-, expecting improvements in earnings and cash-flow metrics over the next one to two years.

The revision reflects operational gains, cost savings, and asset sales, all expected to reduce leverage and strengthen the company’s balance sheet.

S&P also highlighted disciplined shareholder distributions and ongoing management initiatives as supporting factors for the stable outlook.

Since making the announcement, pricing has drifted tighter on Pacific National’s existing subordinated notes PNHAU +3.85% Dec-29/54 by around 17bps despite ongoing market turmoil globally, while equivalently rated LLC 7.429% Oct-28/Perp has tightened around 14bps over the same period.

Issuance Update

- Charter Hall (Baa1) has mandated banks for a potential 7-yr senior unsecured FXD transaction.

- Dalrymple Bay Infrastructure (BBB/BBB-) has mandated banks for a potential 5-yr senior secured FXD transaction.

- ICPF Finance (BBB+) has mandated banks for a potential 10-yr senior unsecured FXD green transaction.

- NextDC (unrated) has mandated banks for a potential 4-yr and/or 7-yr FXD and/or FRN subordinated notes transaction.

- MAFG Finance (unrated) priced a $40mn tap to its existing 4.5NC2 senior unsecured notes at SQ ASW +367bps (8.00% coupon). This brings the amount outstanding to $80mn.

- Meridian Energy (BBB+) has mandated banks for a potential 7-yr senior unsecured FXD green transaction.

- NBN Co (AA+/Aa3) is taking IOIs for a 10-yr senior unsecured FXD sustainability transaction. IPG has been set at SQ ASW +110bps area (5.9% indicative coupon).

- Qantas Airways (Baa2) has mandated banks for a potential 7-yr and/or 10-yr senior unsecured FXD transaction.

- Verizon Communications (BBB+/Baa1/A-) is taking IOIs for a 30.5NC5.5 and 30.5NC10.5 A$ junior subordinated notes transaction. IPG has been set at SQ ASW +210bps for the 30.5NC5.5 and SQ ASW +230bps for the 30NC10.5.