The Bank for International Settlements has used its 2026 Annual Economic Report to warn that AI-related borrowing, leveraged non-bank lenders and shrinking fiscal space are now reinforcing each other's risks.

The Basel-based institution's annual economic report, published on 28 June, delivered its bluntest financial-stability warning in years, flagging a system reliant on borrowing, leverage and lenders that sit outside the banking net.

Four pressure points anchored the analysis: persistent inflation risk after the Strait of Hormuz oil shock, the sustainability of AI investment, growing financial risk beyond the banks, and fiscal positions with less room to move than at any point since the Second World War.

"Success depends on sound fiscal and financial foundations," BIS general manager Pablo Hernandez de Cos said.

The central bank umbrella group framed the warning as urgent, since most of that funding now runs through lenders outside the banking system.

Borrowing funds the buildout

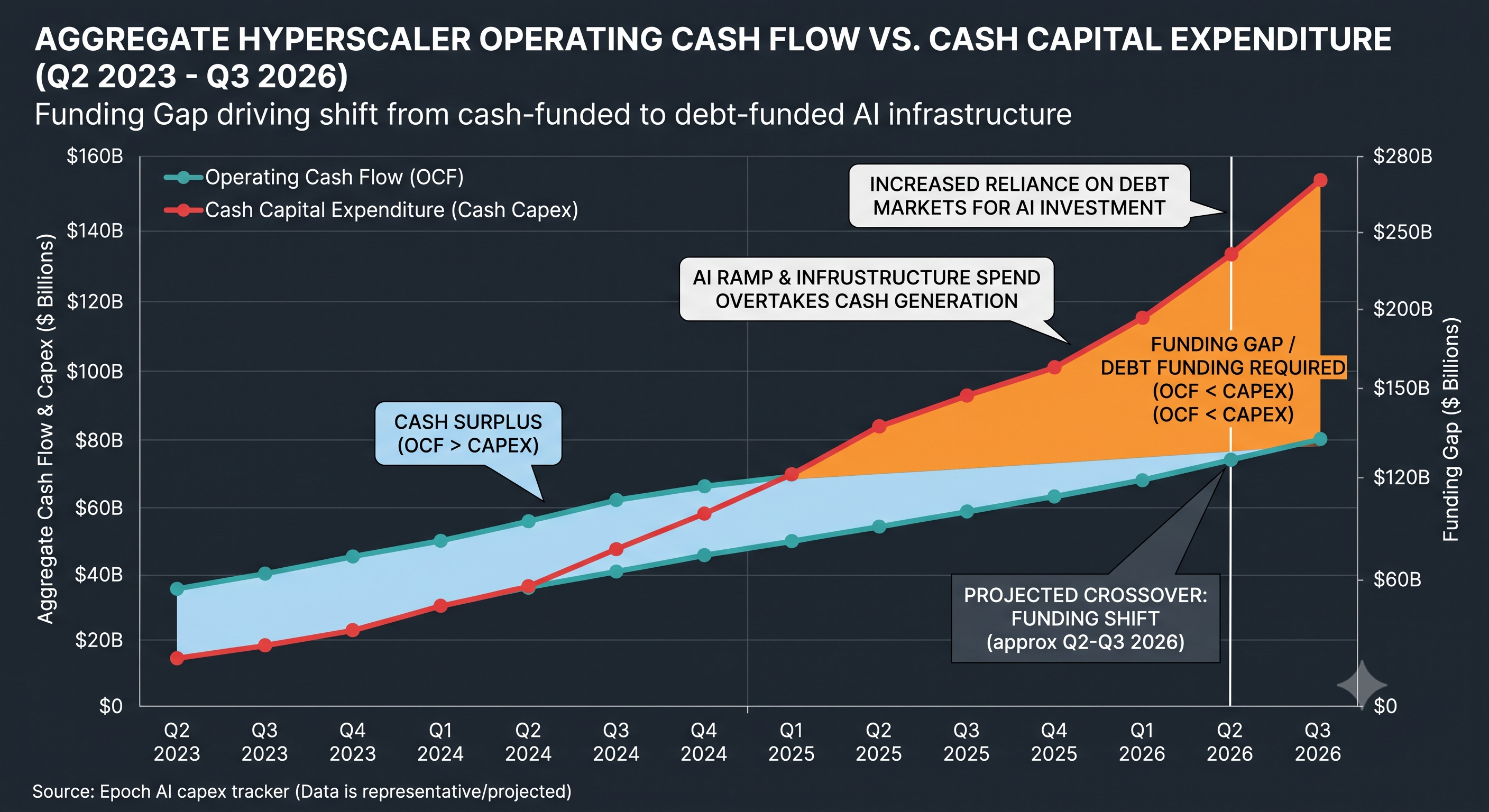

The five largest U.S. hyperscalers, Alphabet, Amazon, Meta, Microsoft and Oracle, are set to spend more than US$1 trillion combined on AI capex across 2025 and 2026, the report found.

That spending is outpacing free cash flow, which is why the same five firms issued $121 billion in U.S. corporate bonds in 2025 alone, 4x their average annual issuance between 2020 and 2024.

Oracle shows the mechanics most clearly, with fiscal 2026 capex reaching around $55.7 billion, above its prior target, and fiscal 2027 capex flagged at up to $95 billion.

What concerns the BIS most is not the size of the exposure but its opacity, in particular what it calls circular financing.

Under that structure, chip makers and hyperscalers take equity stakes in AI labs and neocloud providers in exchange for multi-year purchase deals, while data centres are often leased back on long-dated contracts.

Not every analyst agrees, with CreditSights data putting hyperscalers' aggregate ratio of liabilities to assets at 48% in the third quarter of 2025, down from a 59% peak in late 2022.

Bonds change hands

Who actually owns government borrowing is the second pressure point, and the picture has changed markedly since the pandemic.

Non-bank financial institutions, or NBFIs, now hold 53% of advanced-economy sovereign debt, up from 44% in 2021, as central banks wound down quantitative easing and deficits pushed bond issuance ahead of private credit growth.

Leveraged hedge funds have become the marginal buyer within that shift, with their exposure to U.S. Treasuries, measured against gross domestic product (GDP), up more than 2x since 2022.

These funds typically fund relative-value trades through short-term repo deals, much of it at zero haircuts that let the biggest players borrow against nearly the full value of their collateral.

BIS modelling puts the odds of a Treasury-market stress event on the scale of the 2008 crisis at roughly 3.8% over any three-month window when public debt is high, against 0.3% when it is low.

"More frequent and sharper drops in sovereign bond values," Frank Smets, acting head of the BIS monetary and economic department, said, describing the likely result.

Public finances feel the squeeze

Public debt sits near post-war highs across advanced economies, with cyclically adjusted primary deficits averaging 1.9% of GDP since 2022, nearly double the 1.1% of the previous two decades.

Debt-servicing costs are climbing too, with the IMF projecting interest payments will cover more than half of the rise in nominal public debt between 2025 and 2030.

The gap between bond yields and nominal GDP growth has also flipped positive in many countries, meaning governments can no longer lean on growth alone to stabilise their debt ratios.

What to watch:

- Third-quarter 2026 hyperscaler earnings, when aggregate cash capex is projected to overtake operating cash flow for the first time.

- Remaining 2026 bond issuance from Oracle, Amazon, Meta, Microsoft and Alphabet, and how investment-grade spreads absorb it.

- U.S. Treasury refinancing auctions, and the share absorbed by leveraged funds versus real-money investors.

- Progress on "congruent regulation" of NBFIs at G7 and G20 level.