A dating app, a healthcare insurer, a frozen chip maker and a payroll software firm walked out of the S&P 500 on Monday, replaced by Vertiv Holdings, Lumentum, Coherent and EchoStar - three AI hardware suppliers and a satellite comms operator.

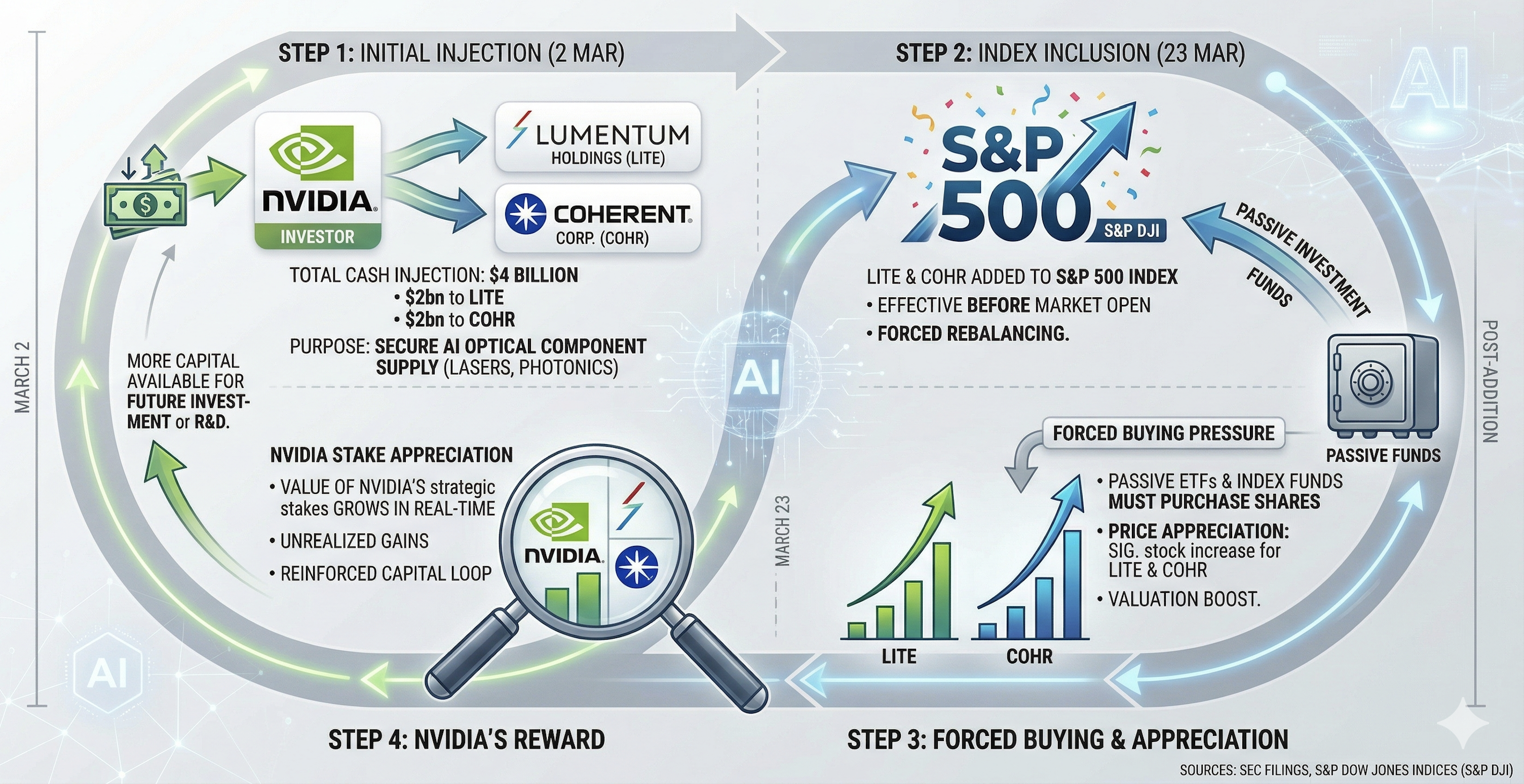

Back at the start of this month, NVIDIA invested US$2 billion in Lumentum Holdings and another $2 billion in Coherent Corp - multi-year strategic deals bundling purchase commitments with future capacity rights for advanced optics and silicon photonics, the connective tissue inside AI training clusters.

Three weeks later, on 23 March, both entered the S&P 500 as part of the quarterly index rebalance, alongside Vertiv Holdings and EchoStar.

Here's where it gets mechanical: trillions of dollars in passive funds track the S&P 500, and when a name enters the index, those funds must buy it - regardless of price, timing or thesis.

That mandatory buying bids up the share prices of Lumentum and Coherent, in which NVIDIA already holds freshly acquired stakes worth $4 billion combined.

The chipmaker effectively funded two stocks into the benchmark and stands to gain as passive capital marks up its positions.

It isn't an allegation of intent - it's a description of how cap-weighted indexing and strategic investment interact when one firm is large enough to move the plumbing.

The loop is bigger than one trade

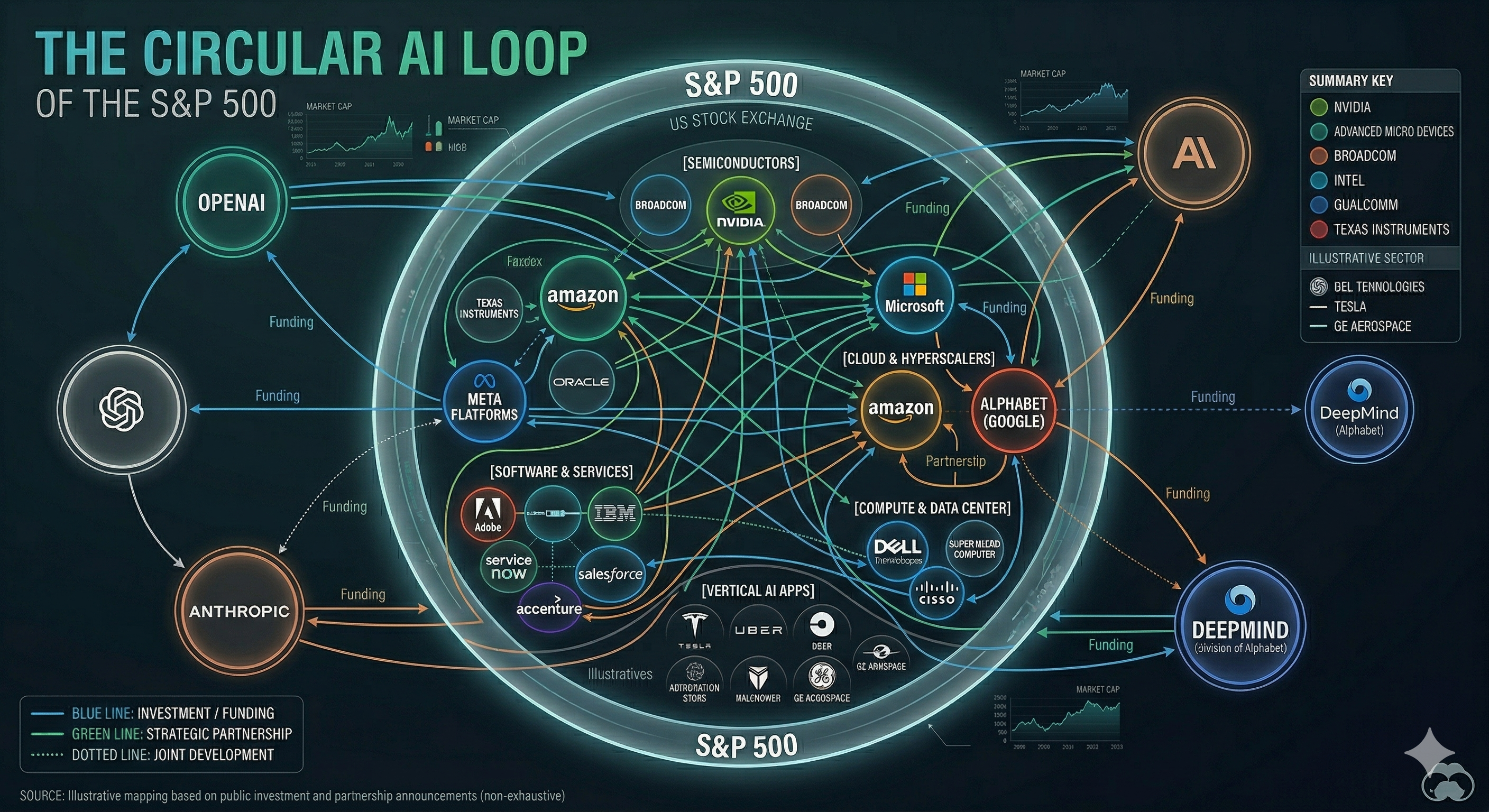

NVIDIA's optical investments aren't an isolated circuit.

Elsewhere in the index, Microsoft has sunk >US$13 billion into OpenAI and depends on the start-up for its Copilot revenue, Amazon, Google and NVIDIA have all bankrolled Anthropic, and practically every AI firm on the planet runs on NVIDIA silicon.

NVIDIA sells the chips, invests in the suppliers that make those chips work, and all of them sit in the same cap-weighted index where size begets more size.

So who's the customer - and who's the supplier? The answer, increasingly, is both - and the S&P 500 is the ledger that books it all.

How big the loop has become

The top 10 constituents now command >40% of the entire S&P 500, up from ~19% in 1990, with tech stocks alone making up more than a third of the composite.

The cap-weighted index has outpaced its equal-weight counterpart by ~32% over three years, per the same RBC research - the widest gap on record, eclipsing even the late-90s tech bubble.

In 2025, the top tech names alone drove an eye-whopping 53% of the index's total return.

These aren't abstract stats - they describe the mechanics of a self-reinforcing loop: capital pours into passive vehicles, those vehicles hoover up whatever's biggest, and the biggest holdings are the ones funnelling hundreds of billions into AI capex, which circles straight back to other constituents supplying that buildout.

The S&P 500 isn't merely tracking the AI trade; it's underwriting it - and all roads lead to NVIDIA.

An awkward comparison

The buy side defaults to the dot-com parallel, but that framing flatters the present - today's dominant firms are genuinely profitable, NVIDIA throws off enormous FCF, and Apple, Microsoft and Alphabet carry net-cash balance sheets that Pets.com could only have dreamt of.

The structural concentration hazard, though, is arguably worse now than in 2000, when the top 10 weighting peaked at ~27% before the unwind, vs today's >40%.

A sharper parallel is the railway mania of the 1840s, and not just because the tech worked, but the returns didn't - British railway firms bought each other's bonds and stock, creating an interlocking web of mutual obligations that amplified the bust when passenger traffic fell short of projections.

The mechanism is the same: circular investment inflates valuations on the way up and accelerates liquidation on the way down, because every participant's balance sheet depends on every other participant's share price.

The question for AI isn't whether it works - it plainly does - but whether >$1 trillion in committed capex generates earnings sufficient to justify current multiples.

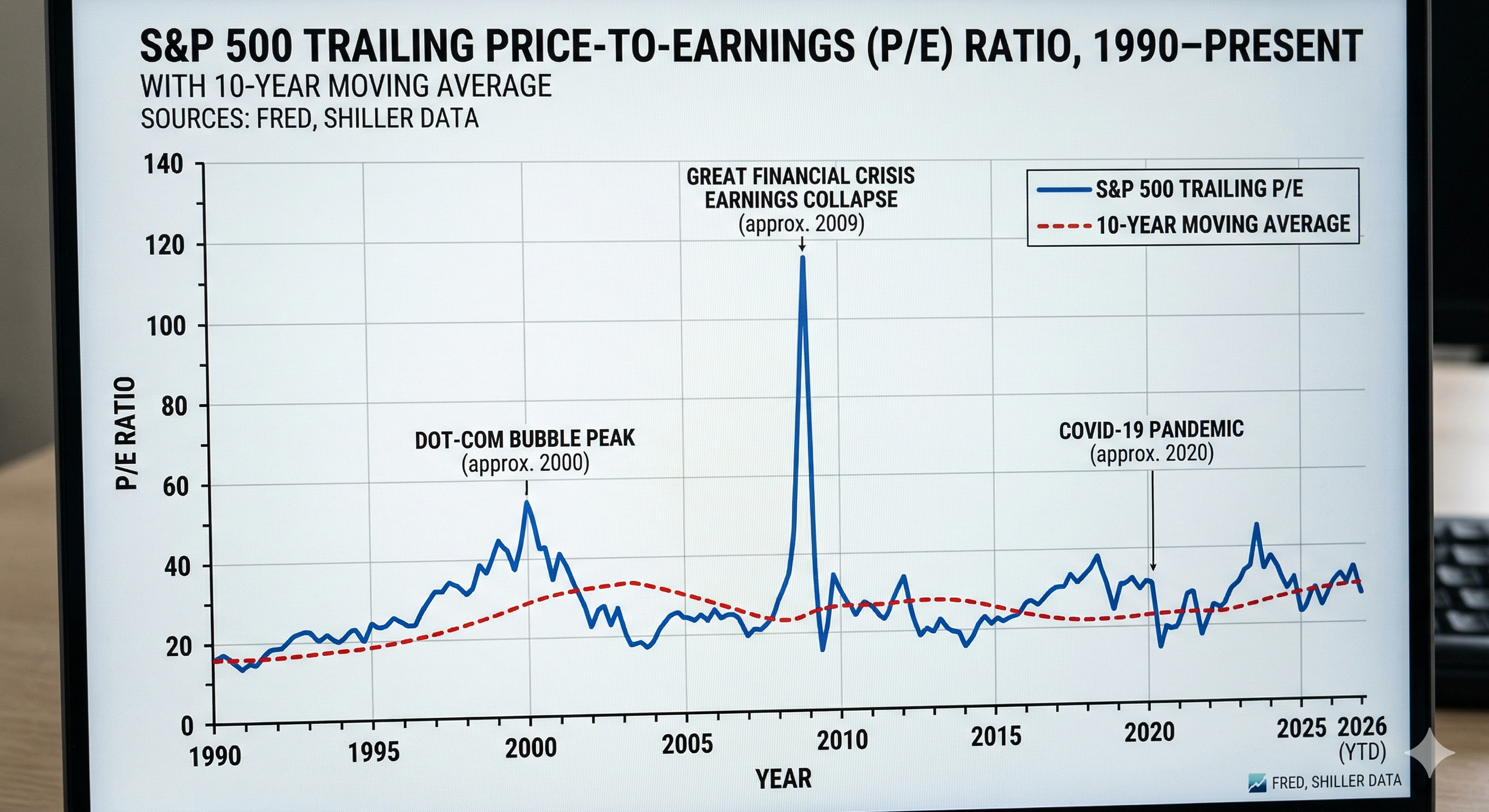

Trailing P/E ratios on the S&P 500 sit between 26.5x and 28.5x, well above the 10yr average of 18.9x.

Running the numbers and a 20% correction in tech, applied to a 34.6% sector weight, would mechanically drag the S&P 500 down ~7% even if every other sector held steady.

What breaks the loop

If AI ROI disappoints, the loop runs in reverse.

Valuations drop, passive funds mechanically sell, NVIDIA's stakes in its suppliers decline, and the names it helped fund toward index eligibility begin losing the weight that justified their inclusion.

The virtuous circle becomes a vicious one, and every participant's drawdown compounds every other's.

JPMorgan's head of global markets strategy, Dubravko Lakos-Bujas, put it bluntly in a note to clients last week, warning the gauge was fragile well before crude prices entered the picture.

"The S&P 500 was already contending with a raft of concerns prior to the oil shock, including fears around private credit, lower consumer affordability, and a weakening AI story," Lakos-Bujas wrote.

"Investors have been mostly hedging rather than de-risking, with gross leverage still near highs."

The bank has trimmed its year-end target to 7,200 from 7,500, warning that if the gauge breaches the 200-day MA near 6,600, support may not materialise until the 6,000-6,200 range - and as of Friday 20 March, the S&P 500 sat at 6,506.

So what if, now, the benchmark has become a trade where the largest player funds its own suppliers into the index, passive capital bids them up, and the whole structure holds together only as long as capex keeps converting to earnings.

One resonating and repeating question this journalist asks is: Is this healthy?