Weight-loss drugs are changing what people in the West order, how much they eat, and where the restaurant sector's next margin dollar comes from - and the industry is only starting to figure out what that means for the business model.

A new McKinsey roundtable on the future of restaurants dropped this month, featuring five partners across the consultancy's global network in a wide-ranging discussion covering robotics, AI-powered personalisation and the "unbundling" of the traditional dining format.

But the sharpest near-term signal concerns something that isn't tech at all: GLP-1 meds.

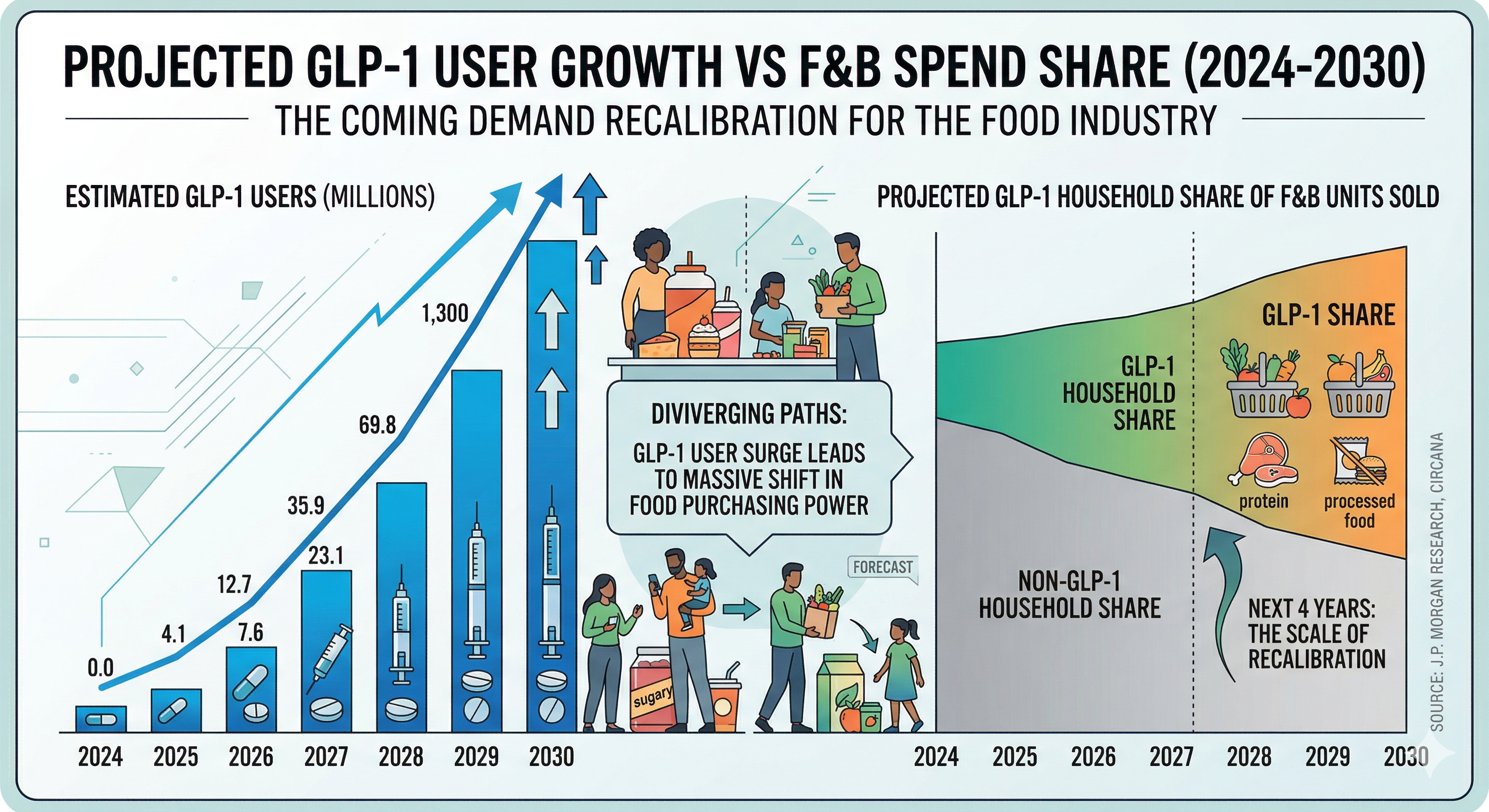

By 2025, 12% of all Americans had used some form of GLP-1 drug for weight loss, and the U.S. obesity rate fell for the first time in a decade.

J.P. Morgan estimates more than 30 million Americans could be on GLP-1 treatment by 2030, up from around 10 million in 2026, and Circana projects that households with GLP-1 users will account for 35% of all U.S. food and beverage units sold by that date.

The National Restaurant Association pegs the U.S. restaurant market at US$1.5 trillion, so those adoption numbers are not rounding errors.

What the drugs do to dining

The McKinsey panel tackled the GLP-1 question head-on, and the takeaway was more nuanced than the bears might expect.

"So much of dining at restaurants is about this indulgent, away-from-home moment and shared experiences," McKinsey partner Katharine Mattox said.

"Simply saying that goes away because the quantity of food consumed decreases is too simplistic an assertion."

Early data backs that up - to a point. GLP-1 usage doesn't appear to dent how often people eat out, but it does change what they order when they get there, with sides, apps and sugary drinks taking the biggest hit.

Dinner traffic among regular GLP-1 users has fallen 6%, according to Revenue Management Solutions, and brekkie has softened too, especially among higher-income users.

Within six months of starting treatment, households cut grocery spend by an average of 5.3%, with higher-income shoppers down 8%, according to Cornell University researchers.

Spending at QSR chains and coffee shops dropped around 8% as well.

But Circana's data tells a more complex story: while GLP-1 users have cut retail F&B purchases, their restaurant spend has actually risen.

Diners on the drugs are eating less overall but directing a bigger share of a smaller food budget toward eating out, favouring quality over quantity - and that reads as a margin story, not a volume collapse.

Who's already moving

The menu response is underway across major U.S. chains.

Shake Shack (NYSE: SHAK) debuted its "Good Fit Menu" nationwide in January, featuring lettuce-wrapped burgers packing up to 52g of protein and billing the range as GLP-1-friendly.

Chipotle (NYSE: CMG) rolled out a high-protein lineup with "Protein Cups" in late 2025, Olive Garden parent Darden (NYSE: DRI) added a lighter-portions offering, and Smoothie King went further still with a dedicated GLP-1 range.

Starbucks (NASDAQ: SBUX) unveiled protein lattes and protein cold foam aimed at users pulling back on sugary drinks, while McDonald's (NYSE: MCD) CEO Chris Kempczinski has flagged on earnings calls that GLP-1 user preferences are now factoring into new product development.

McKinsey partner John Moran framed the opportunity beyond portion tweaks.

"If you think about the trade-off we've always seen, where people want healthy food that tastes good, we've tended to prioritise the good-tasting part over the healthy part," Moran said.

He pointed to ethnic cuisines as primed for expansion, noting few successful chain Indian restaurants exist on the LSR end despite what he sees as clear potential.

"There have been a few, but why doesn't that have the potential to break through in a much bigger way?" Moran said.

Cava Group (NYSE: CAVA) has carved out the fast-casual health lane, with Med-style bowls that naturally skew toward the protein-heavy profile GLP-1 users gravitate to.

The stock has been choppy - down around 50% from its 2024 highs - as wider bowl fatigue and a tough consumer backdrop weigh on sentiment, but the chain crossed $1 billion in annual turnover for the first time in fiscal 2025, grew top-line sales 22.5% and opened 72 net new restaurants.

The Med chain expects up to 76 net new openings in 2026, with comp sales growth of 3% to 5%.

"As guests become more intentional with their spend, they are choosing brands like Cava that deliver real differentiation through bold flavours, healthy food and hospitality," co-founder and CEO Brett Schulman told analysts in February.

Sweetgreen (NYSE: SG) plays in similar territory but has had a far rougher run - comps fell 11.5% in Q4 2025 with a full-year net loss of $134.1 million, and the stock collapsed 80% over the past 12 months.

Further back in the value chain, Toast (NYSE: TOST) provides the restaurant tech stack that underpins much of the sector's digital transition.

The platform pulled in $6.15 billion in trailing revenue with a market cap around $16 billion, and recently added an AI-powered ops assistant Fast Company that turns inventory and sales data into actionable insights - the kind of data architecture McKinsey's panel flagged as a future competitive moat.

Toast now powers around 164,000 locations globally after adding a net 30,000 in 2025, and is launching its first drive-thru product this year to crack the QSR segment.

"All of our wins so far and the progress we've made, it's been in casual dining, it's been in sit-down," Toast CEO Aman Narang said on the company's most recent results call.

"Launching a drive-thru product is going to open up that market in a much bigger way than has been available historically," Narang said.

DoorDash (NASDAQ: DASH) rounds out the listed cohort as the dominant U.S. delivery platform, valued at around $66 billion.

As the restaurant format unbundles - splitting where food is made from where it's consumed - the aggregator platforms become more central to the economics, not less.

On the automation side, the landscape is mostly private.

Miso Robotics, maker of the Flippy fry-station bot, has raised $127 million to date and is targeting nationwide rollout in fast-food kitchens, while Hyphen, which builds automated BOH assembly lines, secured investment from Cava in 2024.

Chef Robotics and Bear Robotics are also in the mix, but none have hit public markets yet.

The restaurant of 2035 may not be a restaurant

The deeper argument in the McKinsey roundtable goes well beyond GLP-1 menus and protein counts, touching on a full rethink of how the dining model works.

Moran described what he calls the "unbundling" of the restaurant - the separation of ordering, cooking, consumption and payment into distinct functions that no longer need to happen under the same roof.

"We think about restaurants as a collection of activities that traditionally used to happen in the same place, but that's all come apart," Moran said.

McKinsey partner Xin Huang, based in Hong Kong, described how Chinese operators are already building demand via delivery data before committing capital to a physical site.

"They first look at how many people are placing online orders in an area, then know the population is there, and then open a shop," Huang said.

"It's a different way to open restaurants compared with traditional decision-making."

That changes the calculus on lease structures, franchise valuations, labour models and kitchen design.

If the FOH is optional and the BOH can serve multiple brands from a single location, the traditional restaurant footprint starts to look like an expensive legacy.

Mattox said the labour cost squeeze is speeding up that transition, noting operators can no longer keep jacking prices and will need to find efficiency elsewhere.

"Restaurants can't continue to take prices at the same levels, so they're going to have to start innovating and pulling from other areas, and labour is the next big bucket," Mattox said.

McKinsey senior partner Alex Rodriguez said the recruitment playbook has to evolve in tandem, as automation absorbs routine tasks and operators need to hire for skills AI doesn't replicate.

"If you can get those things off employees' plates, you can refocus them on what they do best: connecting emotionally, providing hospitality, and spending time with the consumer," Rodriguez said.

The timeline the McKinsey panel is working with is around 10 to 15 years, so most of this won't land in next quarter's earnings.

But the capital is already flowing, especially in China, and the operators building data and automation capability now are the ones most likely to set the pace when the rest of the industry catches up.