Galan Lithium (ASX : GLN) has rejected a $240 million cash offer from China’s Zhejiang Huayou Cobalt Co and carmaker Renault for its Hombre Muerto West (HMW) and Candelas lithium brine projects in Argentina.

In terms of stock price, that's an offer of about 28c per share - a ~2.7x premium to the roughly 10-ish cents per share it was trading at when the bid came in.

On rejecting the bid, the near-term lithium producer said it was “opportunistic”, and undervalues the company’s key assets.

Its share price rocketed on that news yesterday, bouncing up 40% by market close, yet still very shy of the offer for the projects.

It’s a lucrative offer, and shareholders may wonder why the deal was rejected so quickly - the onus will be now up to the board, which collectively owns ~6% of the company, to create better shareholder value in a currently depressed lithium market.

Though perhaps management has a point in refusing the bid for its lithium ponds, as this time last year Galan shares were trading at 40c.

Galan is developing phase one of HMW which is pegged to produce up to 21,000tpa lithium chloride next year in an increasingly mining-friendly Argentina that has cut red and green tape for resources projects ever since electing its colourful and pro-Trump President Javier Milei.

While they have a pre-payment offtake deal for US$40 million with China’s Chemphys tabled already, though haven’t received the funds as yet to further developing the mines into production.

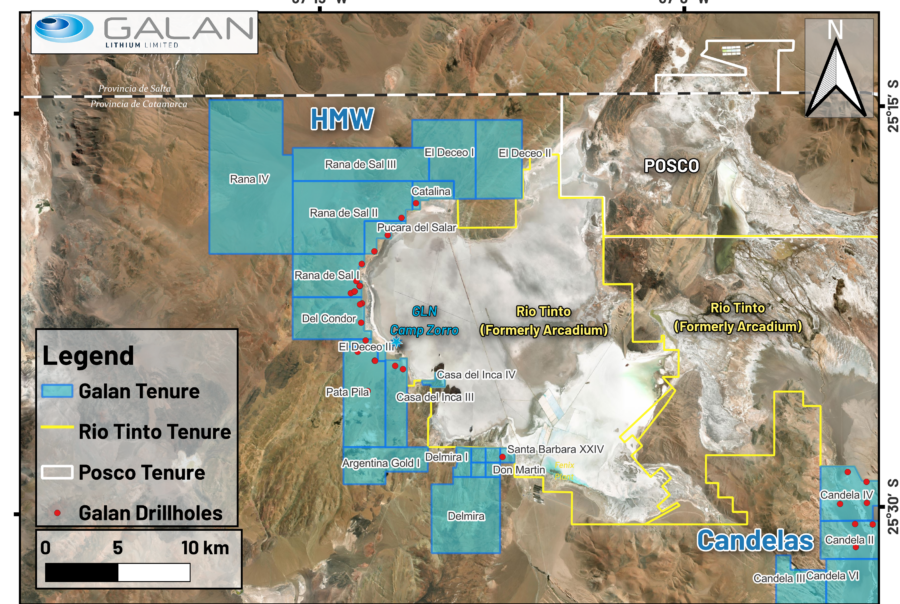

The HMW and Candelas salars surround Rio Tinto’s newy acquired lithium projects when it tookover Arcadium last year and could be primed for further takeover offers down the track.

Could this offer be an early sign of a turnaround for lithium?