The largest coordinated infrastructure program in peacetime history is colliding with every critical input shortage at once - and most investors, governments, and pundits are tracking just one.

The tech industry is attempting to spend US$700 billion on data centres this year alone - individually exceeding the gross domestic product (GDP) of the United Arab Emirates, Singapore and Israel. Bonkers.

That figure ($700 billion) is the combined 2026 capital expenditure commitments from Amazon, Google, Meta and Microsoft, and is underpinned by binding purchase orders for chips, cooling systems, concrete and power, making it the most concentrated infrastructure buildout in modern economic history.

It's also devouring cash at an unprecedented pace.

Bank of America calculates that the five largest hyperscalers will funnel roughly 90% of their operating cash flow into capex this year, up from 65% in 2025, leaving virtually nothing for buybacks, dividends or non-AI ventures.

Amazon faces projected negative free cash flow; Alphabet's is forecast to plummet roughly 90% to $8.2 billion.

And the whole edifice is running headlong into five simultaneous supply squeezes that, individually, would each be sufficient to slow the program, and together constitute a systemic chokepoint the market has not priced because it keeps dissecting each constraint in a silo.

The energy floor just cracked

AI data centres are on track to consume electricity roughly equivalent to Japan's entire national demand this year - more than 1,000 terawatt-hours, per the IEA, double the 2022 figure.

Servicing that load was already the sector's tightest bottleneck before the U.S.-Israel war on Iran began on 28 February.

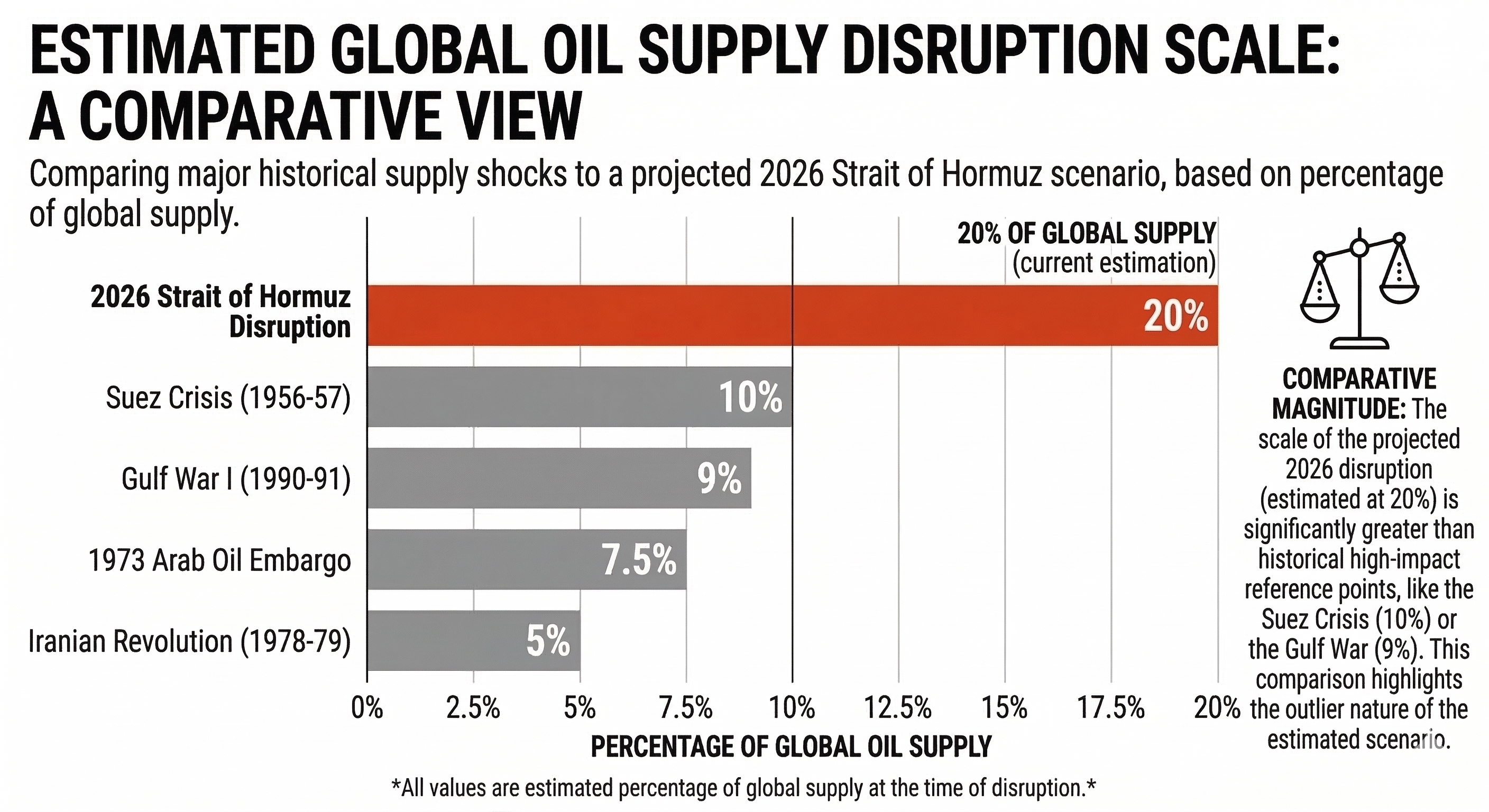

Since then, roughly 20% of global crude and natural gas supply has been suspended - the largest disruption in the history of the oil market, per Rapidan Energy - with Brent crude briefly vaulting past $120 a barrel and the Strait of Hormuz effectively sealed to commercial tanker traffic.

The IEA convened an extraordinary meeting on Tuesday after G7 energy ministers discussed a coordinated release of up to 400 million barrels from strategic reserves - the largest stockpile drawdown in the agency's 52-year history.

That has the hallmarks of a stopgap, not a remedy.

Morgan Stanley projects the U.S. will face a 49-gigawatt power shortfall for data centres by 2028 - equivalent to the electricity needs of roughly 33 million American households - and Microsoft's CEO has conceded that GPUs sit idle in inventory because the company lacks the electricity to install them.

Goldman Sachs estimates U.S. electricity prices rose 6.9% in 2025, more than double headline inflation, and forecasts further increases through the decade as compute-driven load growth compounds the strain.

The war has accelerated a trajectory that was already untenable at pre-conflict energy prices.

Memory has already run out

All three major HBM producers - SK Hynix, Samsung and Micron - have sold out their entire 2026 output slate, with Micron abandoning the consumer memory market altogether to prioritise AI clients.

That's not a temporary allocation blip; it's a permanent rewiring of the semiconductor supply chain.

HBM fabrication devours roughly three times the wafer capacity of standard DRAM per gigabyte, and yields hover between 50% and 60%, meaning every AI-grade chip produced effectively cannibalises the capacity of three to four conventional PC memory modules.

Bank of America characterises this as a "supercycle similar to the 1990s", forecasting the HBM market will reach $54.6 billion this year, up 58%.

The knock-on effects are savage: Nvidia is reportedly slashing gaming GPU production by 30-40%, IDC projects the global smartphone market will contract nearly 13% - the steepest annual decline on record - and Apple's Tim Cook has warned the crunch will compress iPhone margins.

Samsung's global marketing president acknowledged in January that the company can't insulate even its own products from the price surge, calling it "an industry-wide reality."

Relief isn't arriving soon - new mega-fabs from Samsung and SK Hynix won't reach volume output until 2027 at the earliest, and Micron's new facility in upstate New York won't contribute materially until 2028.

The industry shorthand is "RAMmageddon", and the underlying mechanics justify the label.

The rare earth ceasefire expires

China controls 94% of global sintered permanent magnet production - the magnets embedded in every compute-facility cooling pump, EV drivetrain and precision-guided munition on the planet - a share that has nearly doubled from 50% two decades ago.

In October 2025, Beijing imposed its most far-reaching export controls yet, requiring government approval for any product containing as little as 0.1% Chinese-origin rare earth material, even if manufactured entirely outside China.

Those controls were suspended until November 2026 under the Busan trade deal, but the legal architecture was frozen in place rather than torn down - reactivation requires no new legislation.

It's worth noting what the October rules actually entailed: an extraterritorial "deemed export" regime modelled on Washington's own Foreign Direct Product Rule, an automatic denial for defence end-users, and a prohibition on Chinese nationals supporting overseas rare earth projects without state approval.

With the Iran conflict reshuffling Chinese energy import costs, diplomatic positioning, and equity flows simultaneously, the conditions for a snap reinstatement are well within range.

The consensus among compliance advisers: treat the next eight months as a preparation window, not a reprieve.

Gold's repricing

Gold is trading above US$5,200 per ounce (oz) after touching a record $5,417/oz in early March, while silver has surged approximately 150% year-on-year and the gold-silver ratio has compressed to 58.2.

The surface-level read frames this as a wartime haven bid, and that's part of the picture, but central banks were accumulating well before the first strike on Tehran - the People's Bank of China has extended purchases for a 15th consecutive month, and Uganda launched a domestic gold-buying program this month.

What the price action telegraphs, beyond the geopolitical premium, is sovereign de-risking from dollar-denominated reserves at a juncture when the U.S. fiscal trajectory, Fed independence and foreign policy stance are all shifting concurrently.

Markets have priced three Fed rate cuts this year, the gold-silver ratio has narrowed to levels many physical investors regard as historically compelling for silver, and the persistent bid from official-sector buyers shows no sign of abating at $5,000-plus prices.

Gold at these levels isn't discounting a conflict - it's discounting a tectonic realignment in how central bank reserves are composed.

K-shaped reckoning

Nvidia guided $78 billion for Q1 FY2027, clearing consensus by more than $5 billion, yet the muscularity at the apex of the AI supply chain coexists with deteriorating conditions almost everywhere else.

U.S. unemployment has drifted to 4.4%, and a Pew Research survey from February recorded 72% of Americans holding a negative economic view.

In Virginia, where compute-facility density is the highest in the country, residential electricity rates have climbed 20-30% since 2022 - and an NPR investigation found the cost of grid expansion to serve those facilities is being distributed across all ratepayers, a dynamic one industry watchdog labelled a "massive wealth transfer."

A Goldman Sachs economist warned in February that a stock market correction now represents the single largest risk to the economy via the reverse wealth effect, at a moment when the AI capex cycle is funnelling outsized gains to a narrow band of the market while the broader consumer base absorbs the input-cost burden.

That asymmetry - record hyperscaler spending financed increasingly by debt, record chip guidance, record gold, and a consumer base already stretched by three years of cumulative inflation - isn't stable.

It's a formula that works until it doesn't.

The feedback loop nobody is paying attention to

These five pressure points aren't discrete; they're interlocking.

A prolonged Strait of Hormuz closure drives up power costs for compute facilities, compresses margins for memory fabricators, and reinforces Beijing's hand on critical minerals.

Rising input costs erode the sustainability of the AI capex cycle, which undermines the equity valuations anchored to it, which in turn drags on consumer confidence - a self-reinforcing loop rather than a series of parallel inconveniences.

The base (or bull) case holds that the Iran conflict resolves itself before a full-scale energy crisis materialises, memory capacity loosens by late next year as new fabs up their volume, and the rare earth truce survives through the American midterms.

The bear case though - where two or more of these binds tighten concurrently and persist longer than consensus expects - isn't a fringe scenario but a plausible one.