Australia's economy grew at a slower-than-expected pace in the March quarter, with subdued household spending, weaker government consumption and weather-related disruptions weighing on activity despite strong investment in data centre infrastructure.

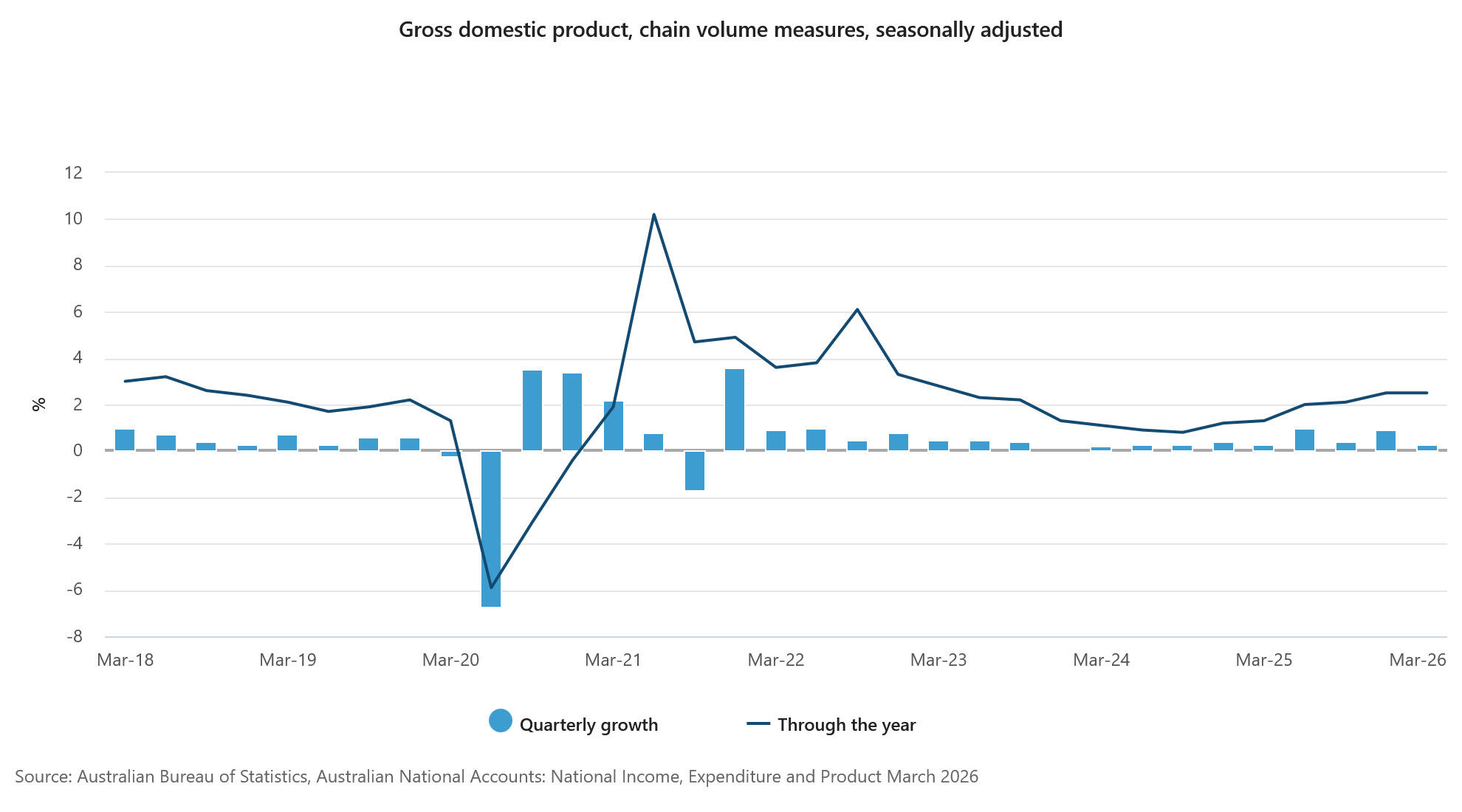

The Australian Bureau of Statistics (ABS) reported that gross domestic product rose 0.3% during the March quarter and 2.5% over the year, marking the softest quarterly growth rate since the June quarter of 2024.

Markets had expected quarterly growth of 0.5% and annual growth of 2.7%.

ABS head of National Accounts Grace Kim said: "Economic growth slowed in the March quarter, with modest household and public sector expenditure as well as cyclone disruptions to mining and export activities."

The result reflected a mixed economic backdrop in which strong private-sector investment offset weakness in other areas of the economy.

Investment in machinery and equipment for data centres was the largest contributor to growth during the quarter. However, because much of the equipment was imported, the positive contribution to economic activity was partially offset by a deterioration in net trade.

Nominal GDP rose 0.6% during the quarter, while the GDP implicit price deflator increased 0.3%.

Domestic prices continued to rise, driven by higher consumption and construction costs. Automotive fuel prices increased sharply towards the end of the quarter, contributing to higher vehicle operating costs, while construction prices remained elevated due to ongoing competition for labour and raw materials.

Australia's terms of trade rose 1.1%, supported by a 1.2% decline in import prices following the appreciation of the Australian dollar.

Lower import prices reduced costs across a broad range of imported services, consumer goods and capital equipment.

However, higher prices for fuels and fertilisers partly offset those declines as concerns over the Middle East conflict and the closure of the Strait of Hormuz disrupted supply chains.

Export prices slipped 0.1%, largely reflecting lower iron ore prices amid oversupply concerns. Higher prices for lithium and coal partly offset the decline, with growing demand from battery production and electric vehicle manufacturing supporting lithium prices.

Domestic final demand contributed 1.0 percentage point to overall GDP growth.

Private sector activity accounted for the bulk of that contribution, with private investment adding 0.7 percentage points and household consumption contributing 0.3 percentage points.

Public demand was broadly neutral, as a 0.9% increase in public investment was offset by a 0.2% decline in government consumption.

Westpac analysts noted that business investment outside the data centre sector remained subdued.

"Outside of data centres, new private business investment likely went backwards in year-ended terms. This is consistent with other investment classes being more mixed, with new building investment increasing 2.7%qtr, while new engineering construction offset this, falling 2.5%qtr."

Net trade detracted 0.8 percentage points from GDP growth as exports fell 1.1% while imports rose 2.1%.

Export volumes were affected by adverse weather conditions, particularly in the mining sector. Coal production was disrupted by Cyclone Koji, while inventories of coal and iron ore accumulated as transportation bottlenecks and softer export demand delayed shipments.

Inventory changes were neutral overall. Mining inventories increased due to weather-related logistics disruptions, while inventories in manufacturing and retail sectors declined.

Manufacturers reduced inventories as demand for gold and other primary metals increased. Retailers, particularly automotive dealers, lowered stock holdings in anticipation of weaker consumer demand, while food and fuel retailers reduced inventories amid stronger sales.

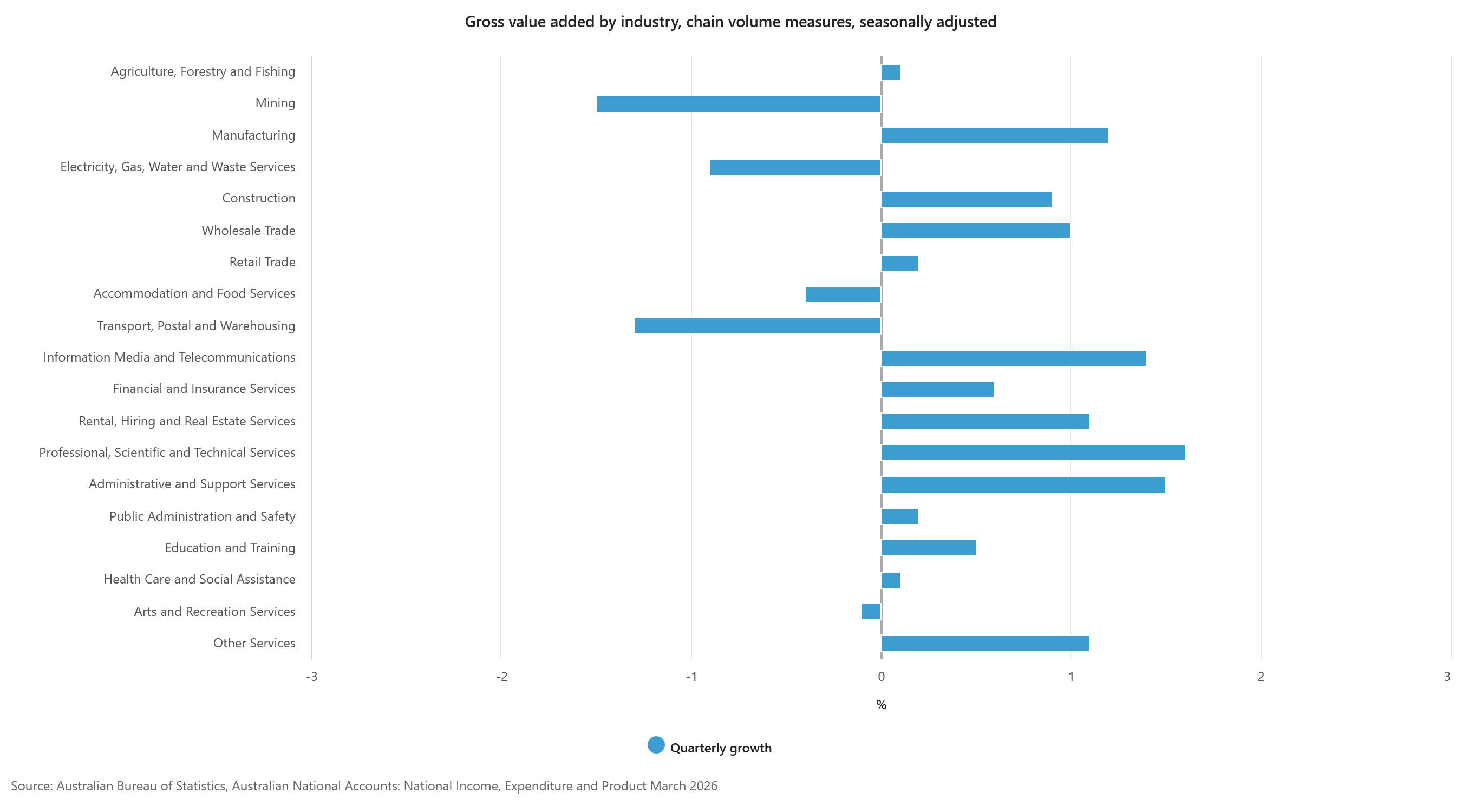

Gross value added increased in 14 of Australia's 19 industries during the quarter.

Business services were among the strongest contributors, supported by demand for engineering design services, information technology consulting and expanding data centre operations.

Construction activity also strengthened, driven by residential projects, apartment developments and data centre fit-outs.

Manufacturing output increased as demand for fertilisers and pesticides rose, while mining was the largest drag on growth due to cyclone-related disruptions to coal production.

Consumer-facing industries remained under pressure. Retail Trade, Accommodation and Food Services, and Arts and Recreation Services all recorded weaker activity as households continued to limit discretionary spending.

ANZ analysts said wage and inflation indicators within the national accounts suggested recent price pressures may prove temporary.

"The broad measure of wages contained in this release has moderated sharply and is running at around the same pace as the Wage Price Index (WPI).

"Given the differences between the two measures that’s relatively unusual. Nominal unit labour costs continue to trend lower and were 3.2% higher over the year to Q1 2026. The household consumption deflator was 3.1% higher over the year.

"While both remain above the RBA’s target band they nonetheless suggest that some of the increase in inflation since the second half of last year is likely to be temporary. That is also consistent with the recent trends in the monthly trimmed mean."

Separately, the ABS released experimental estimates examining illicit tobacco and nicotine consumption after growing public interest in the issue.

While illicit tobacco is not included in official national accounts figures, the ABS found that consumption from illicit sources appears substantial and increasing.

Grace Kim noted: "Experimental estimates based on wastewater analysis indicate that the share of tobacco and nicotine products consumed from illicit sources is substantial and growing, although it does not have a material impact on the level or growth of household consumption."