Save a prayer till the morning after: The strains of this immortal 1980s Duran Duran classic could be aptly applied to the global economy the day after the United States-Israel war with Iran finally peters out. While markets will clearly bounce on the news that the war is over, there’s growing speculation over exactly how long it could take for the global economy to resemble anything close to normalcy.

U.S. President Donald Trump’s plans for having his “mission accomplished” moment appear all but dashed, especially given Iran's unwillingness to give up now, resembling the Black Knight scene from the 1975 film Monty Python and the Holy Grail, which mocks the limbless, unstoppable, stubborn warrior.

By all accounts, the Iran war will end sooner rather than later, as Trump faces huge political pressure in an unpopular war and the Iranian capability that is rapidly degrading.

However, that could still be weeks away, and oil prices could still go higher before they come down.

Aftershocks

While the [Iran] war coming to an end is one thing, getting the global economy back on track is quite another matter.

Shane Oliver, chief economist with AMP, suspects that post-war aftershocks (aka slow-thaw recovery) – notably deep-seated disruptions in energy markets - could be big and potentially require some sort of long-term military presence to keep the Strait of Hormuz open.

Assuming that happens, he won’t be surprised if a risk premium is priced into the oil price for a long period after the war ends.

“Beyond that it means more defence spending, increased demand for metals, another push along for renewables and more onshoring of supply chains – all of which keeps the world and Australia more inflation prone," he told Azzet.

In the last few weeks, central banks have become more attentive to inflation risks, and the Reserve Bank of Australia (RBA) is no exception.

Like Oliver, Australian Prime Minister Anthony Albanese also expects the aftershocks to be felt both here and abroad even if the war ended today.

“It will have a long economic tail just as the impact of covid followed by the Russian invasion of Ukraine have both had an impact on your industry and on the lives of everyone right around the world,” Albanese told Australian Automotive dealers yesterday.

“The war in the Middle East is disrupting supply chains, it’s pushing up oil prices, and it's adding to pressure on inflation here and right around the world.”

Lingering inflationary pressures

Meanwhile, central bankers and economists have already flagged the impact of lingering inflationary pressures on retail prices and growth forecasts.

Last week, the International Monetary Fund managing director, Kristalina Georgieva, suggested that even a 10% increase in energy prices over one year would push up global inflation by 40 basis points and slow global economic growth by 0.1-0.2%.

While the scale and persistence of the energy shock will ultimately determine the macroeconomic impact, Neil Shearing, group chief economist at Capital Economics reminds the market that crises such as this one have a habit of revealing chokepoints that were previously hidden.

For example, Qatar produces 40% of the world’s helium, which is used in the production of semiconductors.

The region is also a significant producer of ammonia and nitrogen, which are key ingredients in many synthetic fertiliser products.

The real transmission channel, though, is energy.

Shearing also reminds investors that when happens when energy prices rise, income is transferred from energy-importing countries to energy exporters.

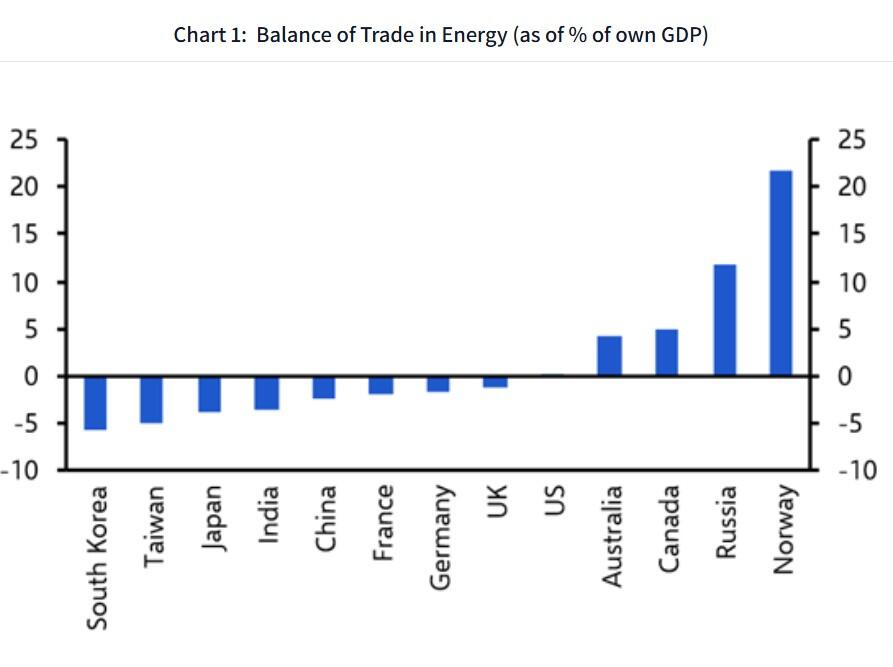

Winners and Losers

Unsurprisingly, obvious winners, adds Shearing are large net energy exporters outside the Gulf whose ability to sell abroad is unaffected.

While the Middle East will face a much slower recovery - where regional GDP could fall by more than 10% - advanced economies (especially the U.S.) are more resilient due to domestic energy production.

“Countries such as Norway, Russia and Canada stand to benefit the most from higher energy prices,” he said.

“At the other end of the spectrum sit economies where energy imports account for a large share of GDP. This group includes countries such as South Korea, Taiwan, Japan, India and China, as well as most European economies, including France, Germany and the UK.”

Assuming the Iran war is short-lived and providing there’s no lasting damage to energy production facilities; Shearing expects the recent spike in oil prices to above US$100 per barrel to prove temporary.

Assuming that is the case, he expects most advanced economies to absorb the shock without significant disruption.

Staying the course

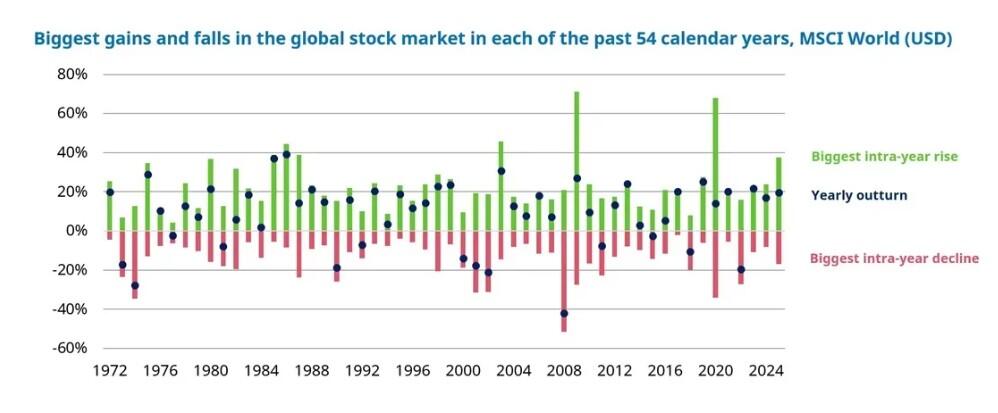

Assuming disruption fades quickly, history suggests that price spikes driven by geopolitical tension start to fade once uncertainty begins to ease.

Historically, financial markets tend to bottom out within an average of 20 days after a geopolitical crisis and fully recover within 43 days.

While periods of heightened geopolitical turmoil may tempt investors to retreat to the sidelines, Duncan Lamont, head of strategic research at Schroders, reminds investors that it can be an expensive mistake.

Even though markets can experience major downturns over the course of a year, he also reminds investors that in the past, the average gains made during the year have more than offset the losses.

History provides some reassurances that knee-jerk reactions aren’t necessary in times of turmoil.

For example, Schroders' data suggests that for the past 50-plus years, stocks, on average each year, have fallen by 15% and risen by 23%.

“In periods of uncertainty or shock, markets can often sell off indiscriminately. Good companies are sold alongside bad ones, becoming mis-priced,” he said.

“Staying invested makes sense. Experienced, ‘active’ investors might even go further and find buying opportunities within the turmoil.”