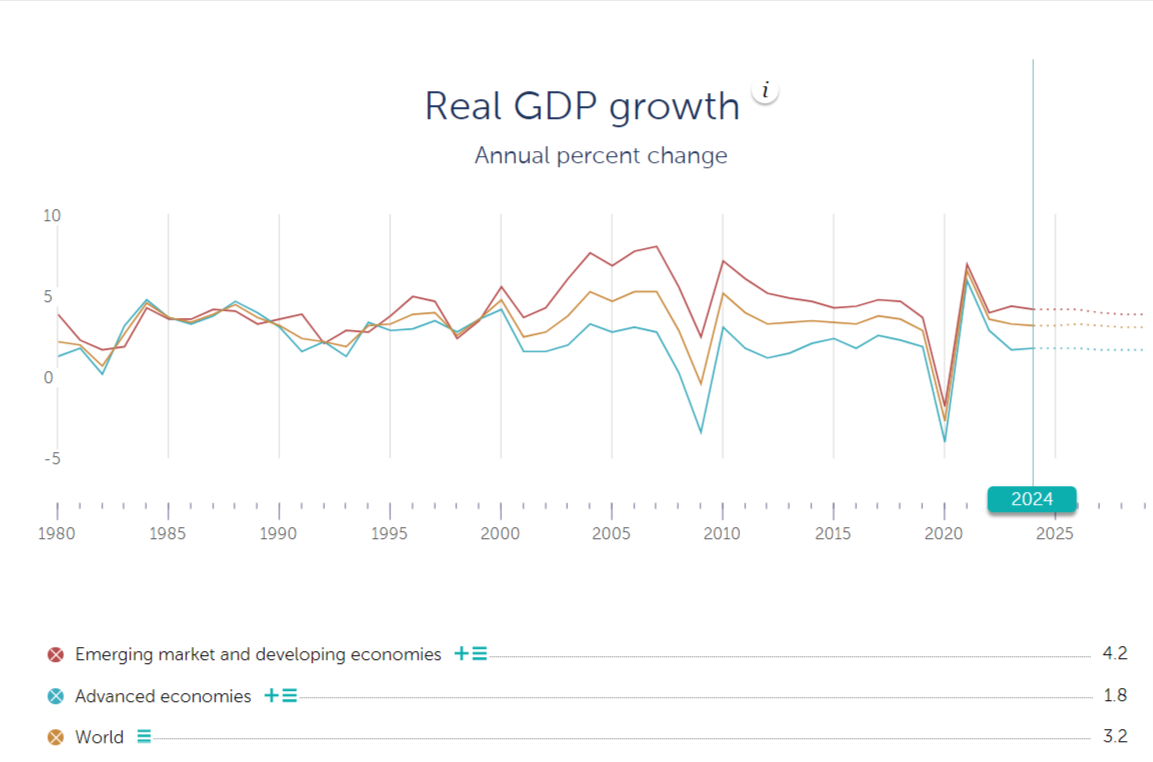

Global economic growth this year is forecast at 3.2% by the International Monetary Fund (IMF).

During its annual meeting in Washington DC, the IMF and World Bank released the 2024 World Economic Outlook report.

According to IMF Director, Research Department, Pierre-Olivier Gourinchas, risks are increasing to the downside due to global economic uncertainty.

Global growth will remain modest, according to the IMF's latest assessment.

There have been notable revisions under the surface since April 2024, however. U.S. forecasts have been upgraded, whereas forecasts for other advanced economies, notably the largest European economies, have been downgraded.

Middle East and Central Asia and sub-Saharan Africa have been revised downward as a result of disruptions to production and shipping of commodities — especially oil — conflicts, civil unrest, and extreme weather events.

As a result, emerging Asia forecasts have been upgraded. A significant investment in artificial intelligence has bolstered semiconductor and electronics demand, a trend supported by substantial public investment in China and India. The global economy will grow 3.1% in five years - a modest performance compared to pre-pandemic levels.

According to the report, Australia will grow by just 1.2% this year, down from 2.1% in 2023, before rising to 2.1% by 2025.

Consumer prices in Australia will remain steady at 3.3% for both years, according to the IMF.

Transcript of World Economic Outlook October 2024 Press Briefing

Gourinchas: "The battle against inflation is almost won. After peaking at 9.4% year on year in the third quarter of 2022, we now project headline inflation will fall to 3.5% by the end of next year, and in most countries, inflation is now hovering close to central bank targets.

"Now, inflation came down while the global economy remained resilient. Growth is projected to hold steady at 3.2% in 2024 and 2025. The United States is expected to cool down, while other advanced economies will rebound. Performance in emerging Asia remains robust, despite the slight downward revision for China to 4.8% in 2024. Low‑income countries have seen their growth revised downwards, some of it because of conflicts and climate shocks.

"Now, the decline in inflation without a global recession is a major achievement. Much of that disinflation can be attributed to the unwinding of the unique combination of supply and demand shocks that caused the inflation in the first place, together with improvements in labour supply due to immigration in many advanced countries. But monetary policy played a decisive role, keeping inflation expectations anchored.

"Now, despite the good news, on inflation, risks are now tilted to the downside. This downside risks include an escalation in regional conflicts, especially in the Middle East, which could cause serious risks for commodity markets. Policy shifts toward undesirable trade and industrial policies could also significantly lower output, a sharp reduction in migration into advanced economies, which can unwind some of the supply gains that helped ease inflation in recent quarters. This could trigger an abrupt tightening of global financial conditions that would further depress output. And together, these represent about a 1.6% of global output in 2026.

"Now, to mitigate these downside risks and to strengthen growth, policymakers now need to shift gears and implement a policy triple pivot.

"The first pivot on monetary policy is already underway. The decline in inflation paved the way for monetary easing across major central banks. This will support activity at a time when labour markets are showing signs of cooling, with rising unemployment rates. So far, however, this rise has been gradual and does not point to an imminent slowdown. Lower interest rates in major economies will also ease the pressure on emerging market economies. However, vigilance remains key. Inflation in services remains too elevated, almost double prepandemic levels, and a few emerging market economies are seeing rising price pressures, calling for higher policy rates. Furthermore, we have now entered a world dominated by supply shocks, from climate, health, and geopolitical tensions. And this makes the job of central banks harder.

"The second pivot is on fiscal policy. It is urgent to stabilise debt dynamics and rebuild much‑needed fiscal buffers. For the United States and China, current fiscal plans do not stabilise debt dynamics. For other countries, despite early improvements, there are increasing signs of slippage. The path is narrow. Delaying consolidation increases the risk of disorderly adjustments, while an excessively abrupt turn toward fiscal tightening could hurt economic activity. Success requires implementing, where necessary, and without delay, a sustained and credible multi‑year fiscal adjustment.

"The third pivot and the hardest is toward growth‑enhancing reform. This is the only way we can address many of the challenges we face. Many countries are implementing industrial and trade policy measures to protect domestic workers and industries. These measures can sometimes boost investment and activity in the short run, but they often lead to retaliation and ultimately fail to deliver sustained improvements in standards of living. They should be avoided when not carefully addressing well‑identified market failures or narrowly defined national security concerns.

"Economic growth must come, instead, from ambitious domestic reforms that boost innovation, increase human capital, improve competition and resource allocation. Growth‑enhancing reforms often face significant social resistance. Our report shows that information strategies can help improve support, but they only go so far. Building trust between governments and citizens and inclusion of proper compensation measures are essential features.

“Building trust is an important lesson that should also resonate when thinking about ways to further improve international cooperation to address common challenges in the year that we celebrate the 80th anniversary of the Bretton Woods Institutions.”