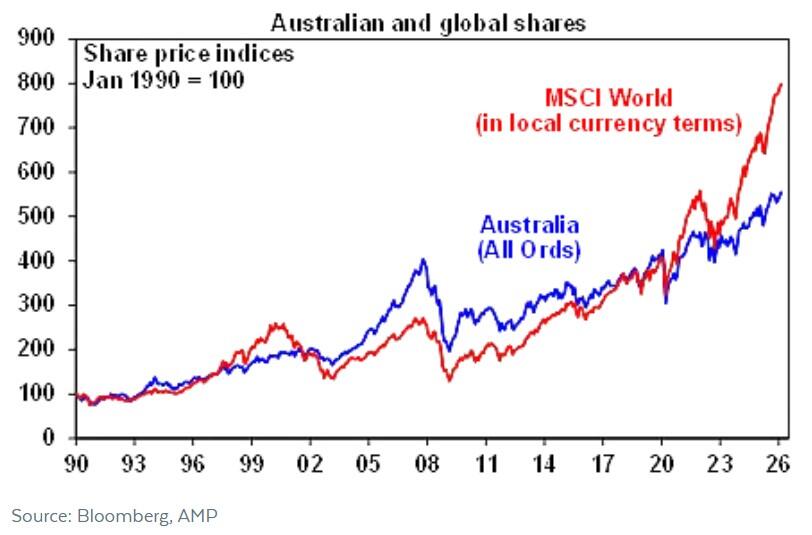

If the Australian share market were a Melbourne Cup starter, you wouldn’t - based on previous form - put an each-way bet on it to be a top-three finisher. Let’s not be coy, the ASX200 has struggled in recent years relative to its global peers.

As of February 2026, the main board of the Australian bourse has risen around 35.21% since February 2021, while the U.S. S&P 500 surged 79.41%, and Japan’s Nikkei 225 nearly doubled with a gain of 97.67% over the same period.

Underpinning the underperformance of Australian equities is its "old world" sector composition, - overly exposed to banks and miners - extreme sensitivity to both the Chinese economy and rising domestic interest rates.

Also adding to the ASX’s laggard moniker – relative to its peers - is the exodus of market-moving large-caps into the hands of private equity.

Is the tide turning?

Due to insufficient capital growth, compared to high-growth international sectors like U.S. technology, the ASX has delivered a total return of approximately 119% since 2008, while the S&P 500 has risen by 305% over the same period.

However, after years of being the perennial loser in the global performance stakes, there’s renewed optimism that the tide is finally turning for Aussie equities.

What’s getting some market commentators excited is the strong start to 2026 with the ASX 200 up 3.3% - and close to new-record highs - while U.S. shares are down 0.1% and global shares are up 1.6%.

Is the US downturn an aberration?

Sceptics may well argue that the recent outperformance of the ASX over the U.S. equities has more to do with the sorry state of the U.S. economy than anything meaningful that’s happening locally.

Much of the U.S. market decline appears to be driven by aggressive trade policies, shifting sentiment around artificial intelligence (AI), and, more recently, market uncertainty fuelled by the prospect of the U.S. government having to repay US$170 billion in trade tariffs.

In short, the aggressive investor sell-off of companies with a whiff of being potential "losers" in the AI revolution is materially impacting the U.S. market.

That’s because AI-related stocks – not unlike banks and miners on the ASX200 - dominate the U.S. equities market through extreme market cap concentration, massive capital expenditure, and outsized contributions to index returns.

As of February 2026, a handful of "Mega Cap" technology companies - led by NVIDIA, Microsoft, and Alphabet - account for a significant portion of the total U.S market value.

In other words, given that these stocks have been primary drivers of the S&P 500's recent gains, when they’re out of sorts, the impact is huge.

Is Australia’s underperformance over?

Despite a few false dawns for the end of the ASX’s underperformance in recent years, Shane Oliver, chief economist at AMP, foresees more upside for the Australian share market on a 12-month view and possibly some relative outperformance.

Firstly, looking purely at the numbers, Oliver can see some evidence that after more than 16 years of underperformance, the local share market eventually bottoms and outperforms for a few years.

He also expects the Australian share market to benefit from a rotation by global investors away from tech shares, with concerns of stretched valuations, excessive capex related to AI - and worries that AI will decimate software businesses - working against the tech-heavy U.S. share market.

Oliver also foresees the AI troubles coinciding with a new super cycle bull market for commodities driven by constrained supply after low levels of investment and electrification, and rising defence spending driving increased demand for metals.

“This will benefit Australia’s resource stocks. Iron ore is likely to feature less this time around partly reflecting slowing urbanisation in China and its property slump,” notes Oliver.

But it’s worth noting that copper is now a bigger contributor to BHP’s earnings than iron ore.”

Upside surprises

Finally, Oliver is also encouraged that after three years of falls, the latest reporting season suggests ASX-listed company profits are kicking up.

“… upside surprises have been surpassing downside surprises by almost two to one, which is the strongest since 2021, and more companies are reporting profits and dividends up on a year ago compared to what was occurring in 2023 and 2024,” he said.

Oliver also reminds investors that [ASX] consensus earnings expectations for this year have risen to 13%, with the turnaround largely coming from the mining sector.

Cautious optimism

Nevertheless, Oliver also reminds investors that markets never go up in a straight line.

He suspects the Reserve Bank’s (RBAs) hawkish bias, with the high risk of more rate hikes, could threaten – but not derail - the Australian economic and profit growth outlook.

However, despite the global uncertainty around tech stocks and any knock-on effect on Australian shares, he believes the outlook for Australian shares remains positive, especially with profits on the rise.

But given that the ride is likely to be bumpy, he reminds investors to stay well diversified.

“There is a good chance its relative underperformance of the last 16 years is at or close to over.”