Oracle Corporation shares fell in extended deals on Wednesday (Thursday AEST) due to worries about the scale of its artificial intelligence (AI) investment and despite the company reporting stronger-than-expected earnings for the fourth quarter of the 2026 financial year (Q4 FY26).

The shares dropped US$12.26 (6.09%) to $189.00 in after-hours trading after the software and cloud-computing giant revealed that capital expenditure (capex) was $55.7 billion in FY26, more than its $50 billion target.

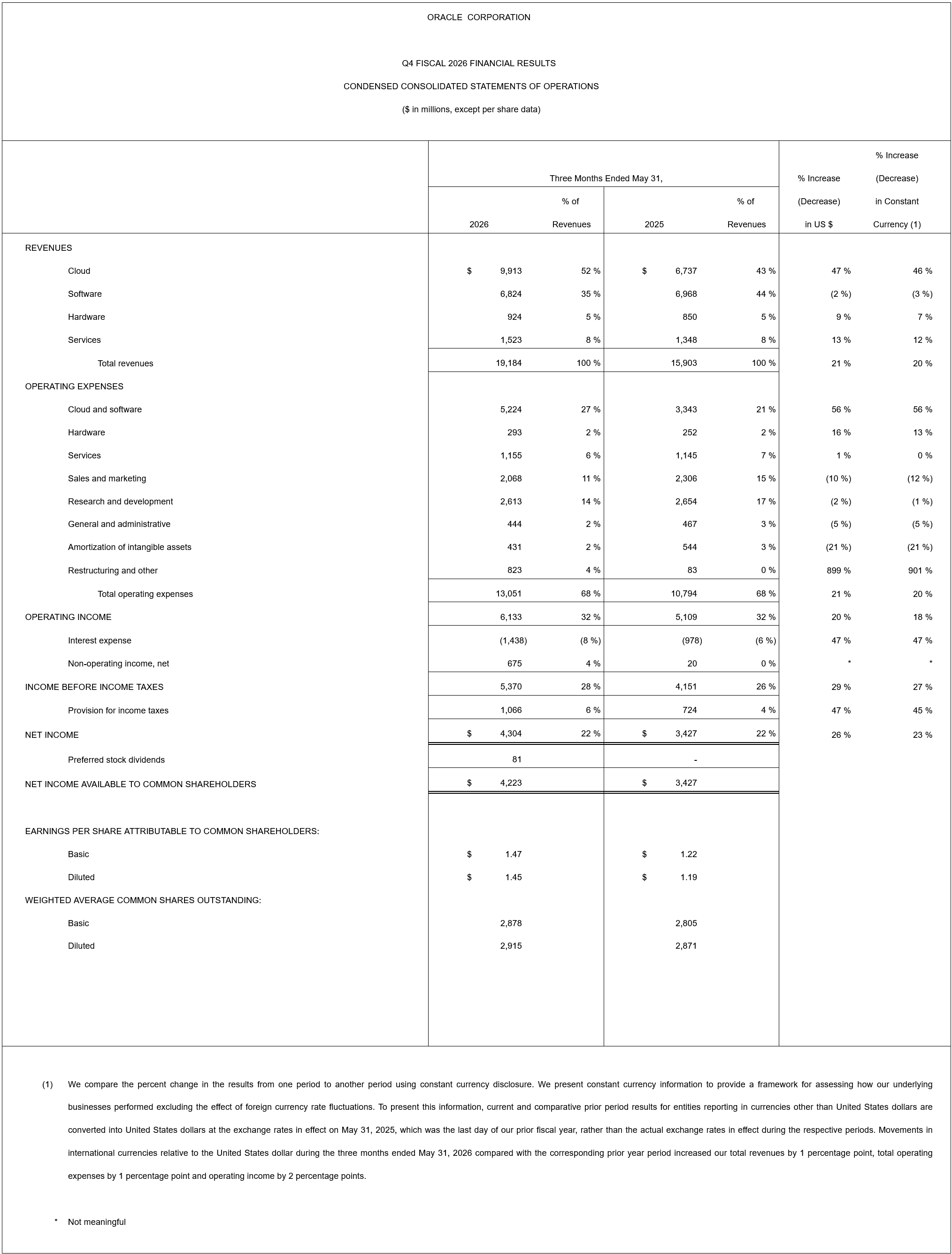

Earlier, the company reported a 26% lift in net income to US$4.304 billion (A$6.15 billion) for the three months ended 31 May 2026.

Diluted earnings per share (EPS) grew 21% to $1.45 on revenue, which rose 21% to $19.2 billion in the latest quarter, while adjusted EPS of $2.11 beat estimates of $1.96, but investors were more concerned about the cost of building data centres and AI infrastructure.

The results were driven by continued strength in Oracle's cloud business, where revenue surged 47% to $9.9 billion in Q4, with cloud infrastructure revenue climbing 93% to $5.8 billion.

For FY26, net income surged 37% to $17.087 billion and diluted EPS rose 34% to $5.83 on revenue, which was 17% higher at $67.4 billion.

Prior to the announcement, the stock had closed $4.55 (2.21%) lower at $201.26, capitalising the company at $478.83 billion.

Oracle also said it would raise almost $40 billion in debt and equity in 2027 to construct its AI infrastructure as competition heats up among technology companies to secure the computing capacity to meet surging demand for generative AI services.

"The demand is real with cloud infrastructure revenue and backlog growing fast. But the funding question is getting harder, not easier, with capex coming in well above estimates and free cash flow still negative," eMarketer analyst Jacob Bourne was quoted as saying in a Reuters article.

The company reiterated its target of $90 billion in revenue in FY27 and lifted its adjusted EPS guidance to $8.05.

The cloud business growth more than compensated for weakness in Oracle’s traditional software business, where revenue dipped 2% in Q4 as customers migrated their on-premises software to the cloud.