Oracle reports its Q3 earnings to Wall Street after the bell - carrying more than US$100 billion in leverage, negative free cash flow, and the distinction of being the only hyperscaler bankrolling the AI buildout with borrowed money.

Consensus expects roughly US$16.9 billion in revenue - a 20% jump and a clear acceleration from 13% growth in the first half of FY26 - yet the balance sheet tells a different story.

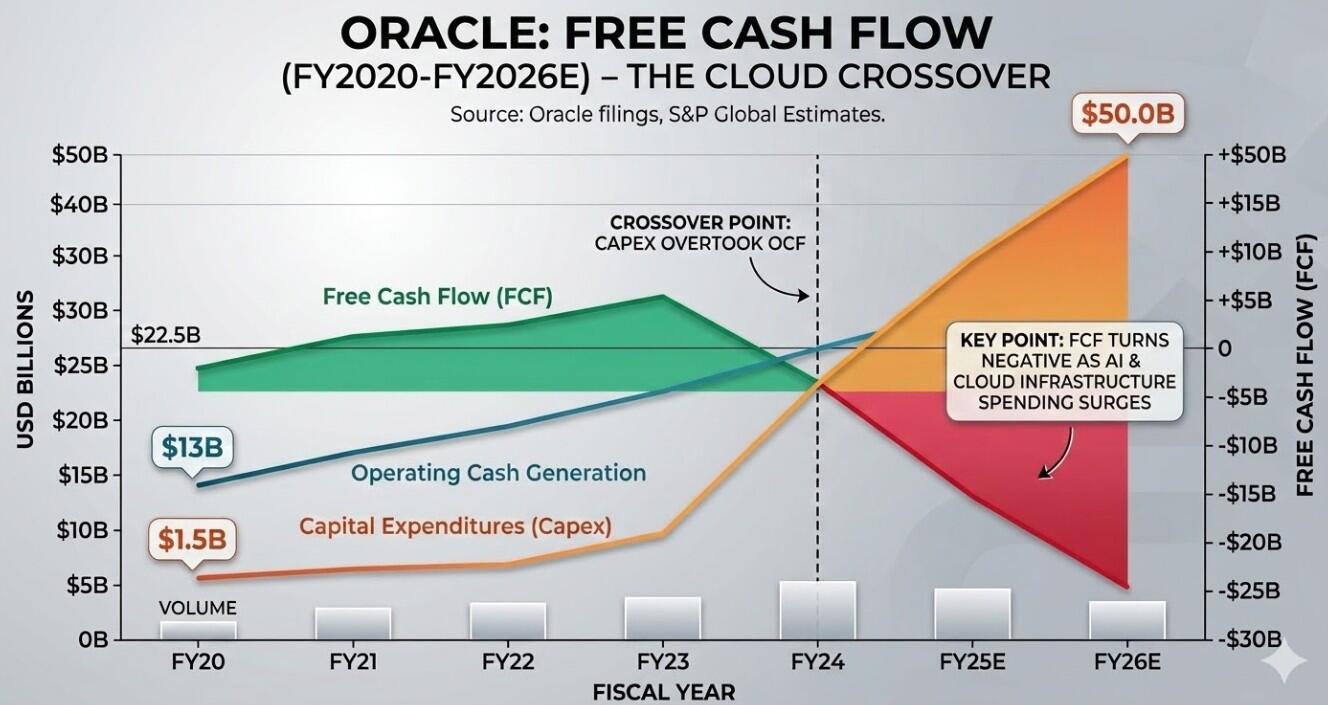

And the company is carrying $113 billion in total debt to finance a compute buildout that has already tipped its free cash flow negative.

Analysts project a full-year cash burn of around $23 billion, and management plans to raise another $45 billion to $50 billion through fresh bonds and equity this calendar year alone.

Google, Amazon, and Microsoft are spending at a comparable scale on AI compute, but capitalising it from operating cash flow, but Larry Ellison's outfit is the only one writing IOUs.

Familiar sequence

Anyone who covered the late-1990s telecom buildout will recognise the shape of this trade.

In the five years after the U.S. Telecommunications Act of 1996, telecom companies poured more than $500 billion - mostly leveraged - into laying fibre optic cable, on the thesis that internet traffic would grow exponentially and bandwidth demand would follow.

The thesis proved correct, which turned out not to matter very much for the people who underwrote it.

Global Crossing laid more than 100,000 miles of undersea fibre, reached a market valuation of $47 billion, and never posted a profitable year before collapsing into Chapter 11 in January 2002 with $12.4 billion in liabilities.

By 2004, analysts estimated only about one-tenth of installed fibre was actually lit.

The glass stayed in the ground and ultimately became the backbone of the modern internet, long after the shareholders who paid for it had been zeroed out.

When chips move faster than concrete

Oracle faces a version of that mismatch, with an added problem - the silicon inside the facilities is obsolescing faster than the facilities themselves can be completed.

Nvidia now ships a new generation of data centre GPUs every year, each delivering a step-change in performance and efficiency.

Vera Rubin, unveiled in January, offers around 5X the inference throughput of its Blackwell predecessor.

Compute campuses take years to permit, construct, and power up.

That gap became difficult to ignore last week when OpenAI walked away from expanding the flagship Stargate facility in Abilene, Texas - a site the company spent billions equipping with Blackwell chips - because it wants Vera Rubin at new locations instead.

Financier Blue Owl Capital has separately pulled back from backing an additional project, and the firm is reportedly preparing to cut 20-30,000 jobs - up to a whopping 18% of its workforce - to free up an estimated $8-10 billion in liquidity.

That's not the hallmarks of a company trimming fat for efficiency. That's a company swapping headcount for hardware and hoping the silicon holds its value longer than Nvidia's product cycle suggests it will.

In comparison, Microsoft generates around 5X the top line on 1.4 times the headcount.

The bull case

AI compute demand is growing and supply-constrained, and the contract book reflects it.

Remaining performance obligations stood at $523 billion last quarter - up 433% YoY - spanning OpenAI, Meta, Nvidia, and xAI.

Oracle CEO Safra Catz has guided for OCI turnover scaling from $18 billion this fiscal year to $144 billion within four years, and if that trajectory holds, the borrowings pay for themselves.

Whether the ramp arrives before the leverage catches up - and whether the GPUs being racked today will still earn their keep by the time it does - is what tonight's numbers need to start answering.

And remember, Global Crossing's fibre was viable plumbing… and it did not save Global Crossing.