Imagine a tax structure that allows income earned by one person to be split across multiple taxpayers - typically within a family, to one partner with a lower marginal tax rate - to reduce the total tax paid by the household.

Similar structures already exist within European economies like France and Germany, and if the recently elected Nationals leader Matt Canavan has his way - it will become part of the Australian tax system.

Germany’s [tax] system focuses on married couples or civil partnerships, regardless of children, whereas in France - which considers the household as one tax unit - the total income is not taxed directly; instead, it is divided by a number of "shares" or "units" based on the family structure.

Canavan is proposing that there are significant benefits in taxing families as opposed to individuals, but it would come at a cost.

According to Parliamentary Budget Office estimates, it would cost the federal budget around $70 billion over the decade.

Family-friendly tax

While this may explain why there’s no current appetite or policy intent to introduce general family income splitting, Canavan argues that the change would make the tax system more “family-friendly” by recognising that many families share resources and financial responsibilities.

The Nationals’ new leader argues that by encouraging parental bonds, a tax system that allows income-splitting would remove the current reliance on childcare.

“Our tax system should encourage parental bonds not penalise them by not treating families as a team,” said Canavan.

“Childcare works for some but not all. Providing more choice will [benefit] all parents because it will take the pressure of our straining childcare system.”

In 2024–2025, the national average for long-day care in Australia was around $129.15 per day before subsidies, with around 40% of employed parents using professional childcare for some or all of their children.

What is income splitting?

Income splitting allows income earned by one person to be distributed across multiple taxpayers, typically within a family.

Given that Australia taxes people using progressive income tax rates, spreading income across one or more people effectively reduces the total tax paid by a household.

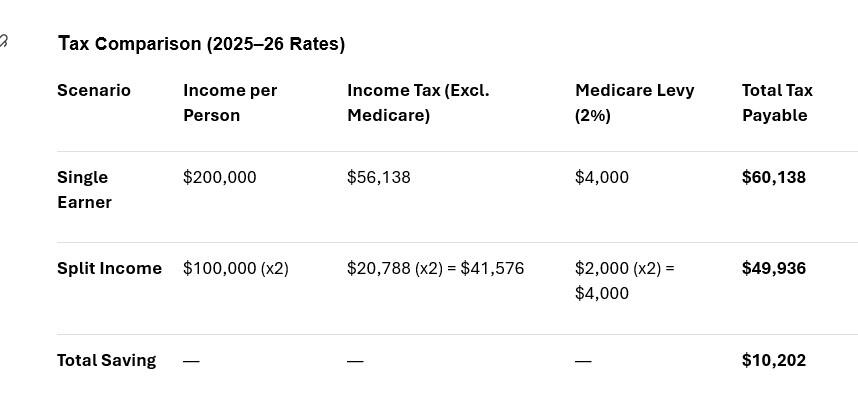

In other words, by splitting an Australian resident taxpayer’s earnings of $200,000 annually between two people, each earning $100,000, the total tax paid reduces.

In the FY25–26 financial year, splitting $200,000 equally between two people results in a total tax saving of around $10,202 compared to one person earning the full amount.

Other structures

While Australia does not formally allow couples to split income, there are legal structures that deliver similar outcomes.

For example, within a family trust, the trustee, typically parents or a nominated company, manage assets or income for beneficiaries, such as a spouse or children.

Under Australia’s family trust provisions, income is typically taxed in the hands of the beneficiaries who are entitled to it.

Given that beneficiaries can include spouses or adult children, trust distributions often spread income across family members and produce tax savings.

However, the Australian Taxation Office (ATO) recently stepped up its scrutiny of trusts or business structures used with the expressed purpose of distributing income to family members on lower tax rates.

Levelling the playing field

Canavan is by no means alone in his call for income-splitting, with independent MP Allegra Spender arguing within her tax white paper that wealthier households already have access to income-splitting strategies while wage earners are shut out.

This is the case where the main wage earner is engaged in a profession such as law, accounting and most trades, and creates an incentive to be self-employed.

Across the political aisle, Liberal frontbenchers Melissa McIntosh and Matt O’Sullivan have also flagged the benefits of income-splitting and want their party to give it serious consideration.

As it currently stands, Australia’s tax system contains rules designed to stop income being shifted simply to reduce tax.

These include rules to:

- discourage diverting income to children under the age of 18. In these circumstances, the beneficiary is usually subject to a higher tax rate.

- restricting certain benefits or entitlements where income mainly comes from someone’s own labour, such as a contractor.