While the big-four ASX banks maintain strongish operational performance, lingering concerns over lofty valuations – relative to key metrics - suggests the likelihood of shares unravelling in 2026 is disproportionately high.

As of February 2026, FN Arena broker consensus suggests the Big Four’s 12-month target prices are heading for a necessary 6% to 27% correction.

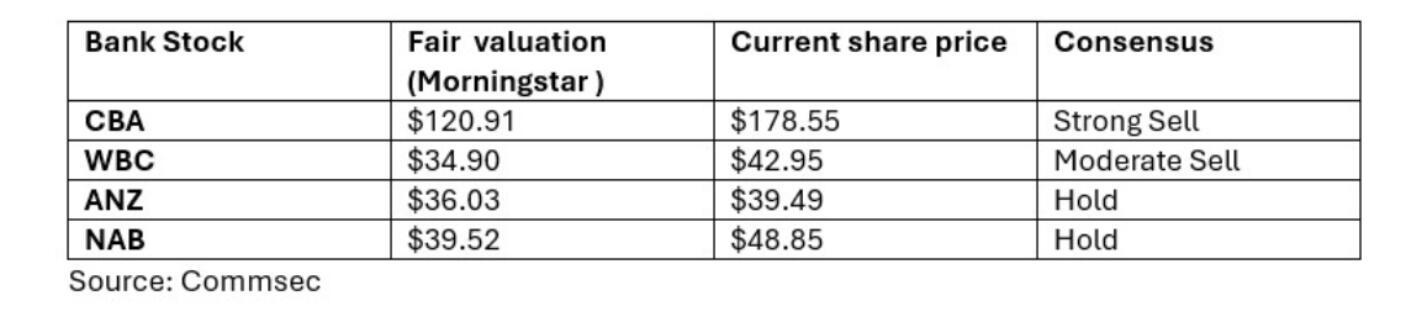

While Commonwealth Bank (ASX: CBA) faces the most bearish outlook with a 27% implied fall to target, ANZ Bank (ASX: ANZ) is considered closest to fair value, requiring only a 6% decline.

Unjustified valuations

Despite posting combined profits of $11.3 billion and resilient capital during the latest reporting period, analysts believe the average forward P/E of around 21x - nearly 43% above the 10-year historical average – is looking increasingly unjustified.

While lingering concerns over valuations are by no means new, the Big Four continue to push higher after surpassing consensus cash earnings forecasts by 4–11% in their February 2026 reporting.

Over the last 12 months share in Commonwealth Bank (ASX:CBA), which trade at the most lofty valuations - forward P/E ratio as high as 26x to 31x – has jumped 16%, while shares in Westpac (ASX: WBC), ANZ Bank (ASX: ANZ) and National Australia Bank (ASX: NAB) are up 37%, 35% and 38% respectively.

Share price outpaces fundamentals

What continues to irk analysts is the degree to which share prices have outpaced fundamental earnings growth.

Unless these banks deliver significant earnings-per-share (EPS) upgrades through 2026, analysts suggest that current prices – which, with the exception of ANZ, have posted further gains since announcing their interim or quarterly updates throughout February - offer a slim margin for error.

The following table shows the level of disconnect between retail appetite for bank stocks and broker expectations; even on Wednesday, while consensus on ANZ is Hold, buyers were outnumbering sellers.

Why is bank performance struggling?

The bank’s golden era of 2023, which saw record profits from rising interest rates, has largely given way to a squeezed era.

Nowhere is that squeeze more evident than in net interest margin (NIM) and return on equity (ROE) - two of the most critical benchmarks for Australia's big four bank stocks.

Meanwhile, the average return on equity ( ROE) for these bank majors was around 10.7% in 2025 - a slight decrease from the previous year – and well below the historical averages of between 15–17%.

By failing to achieve these levels, the Big Four signal to analysts that they’re not effectively using shareholder funds to generate profit, and this can negatively impact future dividend growth.

NIM slide

Signalling high profitability, usually achieved through a low cost of deposits, high-yielding loans, and efficient asset management, a good net interest margin (NIM) for a bank generally ranges between 3% and 4% in a stable environment.

By comparison, the most recent reported NIM results for the Big Four are:

- CBA: Reported a NIM of 1.99% for the full year 2024, an 8-basis point decrease from the previous year. More recent data indicates a NIM of 2.04% as of late 2025.

- Westpac: Reported a NIM of 1.94% for the first quarter of 2026 (ended 31 December 2025), a slight 1-basis point decline from the second half of 2025. Its full-year 2024 NIM was 1.93%.

- NAB: Reported a NIM of 1.80% for the first quarter of 2026 (ended 31 December 2025), reflecting a 2-basis point increase. Its full-year 2025 NIM was 1.74%.

- ANZ: Reported a NIM of 1.56% for the first quarter of fiscal 2026, an improvement of 2 basis points. For the first half of 2024, its NIM was also 1.56%, down from 1.65% in the prior half.

In summary, while margins held up better than expected in recent results, analysts expect downward pressure to intensify [on NIM] through 2026 and 2027 due to aggressive competition in the mortgage market and a shift toward higher-cost term deposits as customers seek better returns.

The decline of NIM by the big-four from their recent peaks - continuing a broader multi-decade downward trend – remains an overhang for their current valuations.

Meanwhile, the Reserve Bank’s (RBA) rate cuts later in 2026 and 2027 are also expected to reduce profit margins by between 5–8 basis points.