The semiconductor industry has spent the first quarter of 2026 bracing for an escalation that has nothing to do with Iran, and will put Taiwanese and South Korean chipmakers firmly within the Trump administration's crosshairs.

On 14 April, the United States Trade Representative and Commerce Department must deliver a report to President Trump on the status of negotiations with key chip-producing nations under Section 232 of the Trade Expansion Act.

That report will determine whether Washington moves to Phase Two - broader tariffs on semiconductors "at a rate of duty that is significant", according to the January proclamation.

Phase One, which took effect on 15 January, was deliberately narrow: a 25% tariff on a small category of advanced computing chips not intended for use in the United States.

The practical target was high-performance AI accelerators like Nvidia's (NASDAQ: NVDA) H200 and AMD's (NASDAQ: AMD) MI325X that were being routed through U.S. facilities and on to China.

The broader semiconductor supply chain was left untouched while the White House negotiated investment commitments from Taiwan, South Korea and Japan.

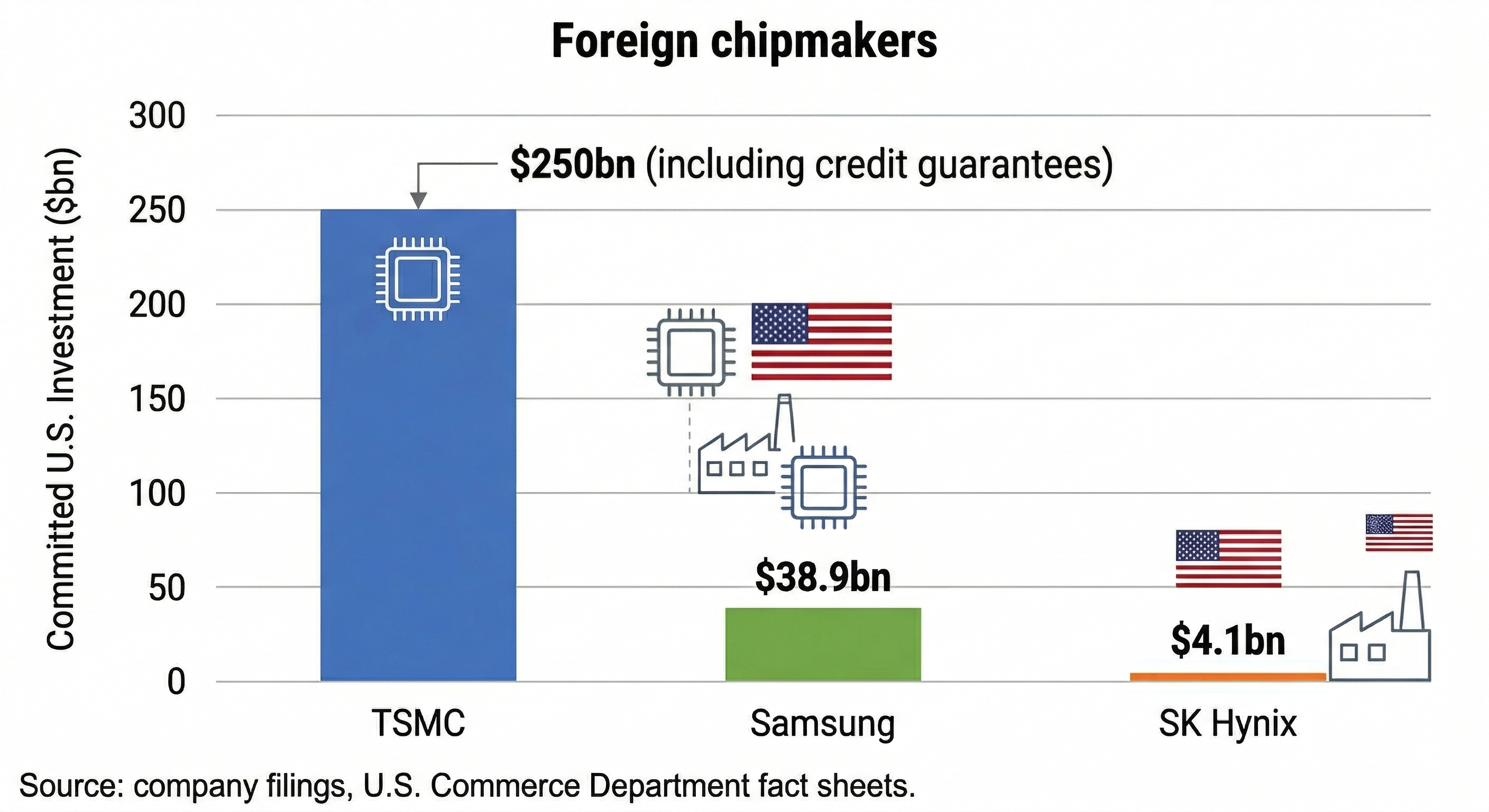

Taiwan moved first, with TSMC (NYSE: TSM) at the centre of a US$250 billion investment commitment announced alongside the tariff proclamation.

The terms were generous for companies willing to build on American soil: Taiwanese firms constructing new fabs can import up to 2.5x their planned capacity tariff-free during the build-out phase, dropping to 1.5x once production begins.

Commerce Secretary Howard Lutnick made the alternative plain enough, warning that companies choosing not to build in the U.S. face tariffs "likely to be 100%".

That formula has put South Korea in a difficult position, with Samsung Electronics (KRX: 005930) committing approximately $38.9 billion in U.S. investment and SK Hynix (KRX: 000660) roughly $4.1 billion.

To match TSMC's terms, the Korean chipmakers would need to find another $122 billion - a figure that would strain even their balance sheets.

Seoul has invoked a "no less favourable" clause from its existing trade framework, but there is a meaningful difference between a diplomatic assurance and a tariff schedule.

The 14 April deadline is not the final word - the proclamation gives the President broad latitude to impose Phase Two tariffs immediately if negotiations are deemed insufficient, or to extend the timeline if talks are progressing.

What the report will signal, however, is whether Washington views allied investment pledges as adequate or merely as a starting point for further leverage, and that distinction will set the tone for every semiconductor procurement decision in the second half of 2026.

Three scenarios

The first is an extension with conditions, which remains the path of least disruption, given that negotiations with South Korea and Japan are clearly unfinished and imposing broad chip tariffs on allied manufacturers during an active Middle East war would compound an already precarious inflation picture.

A 60-to-90-day extension, paired with explicit investment benchmarks, would buy time without conceding ground.

The second is a selective Phase Two rollout, in which Washington broadens the tariff base to cover additional semiconductor categories - logic chips, memory or packaging - while preserving exemptions for companies with verified U.S. investment plans.

This approach would pressure laggards without punishing firms already building American capacity, and Samsung, which has struggled in foundry and faces separate headwinds from the software sell-off's impact on enterprise chip demand, would be the most exposed name on either side of the Pacific.

The third is the maximalist scenario: a blanket 100% tariff on non-U.S.-produced semiconductors, as Lutnick has floated, representing the most aggressive industrial policy action since the original CHIPS Act.

It would accelerate reshoring timelines but also spike hardware costs for every AI company, cloud provider and data centre operator in the country - precisely the constituency the White House has been courting for investment announcements.

The timing makes all three scenarios harder to read, because the Iran war has already pushed inflation expectations higher, with Goldman Sachs (NYSE: GS) projecting PCE inflation at 2.9% by year-end.

Layering semiconductor tariffs on top of triple-digit oil could hand the Federal Reserve its worst policy cocktail since the early 1980s.

For the chip sector, 14 April is when the negotiating phase ends, and the pricing phase begins.