With skyrocketing capital city property prices resulting in more families housing multiple generations under one roof, it’s hardly surprising that granny flats are an increasingly common feature across our suburbs.

But beyond family matters, the housing affordability crisis also creates opportunities for those wanting to leverage the dormant value in their backyard through a “secondary dwelling”.

With rental returns reducing as property prices increase, the argument for building granny flats has clearly gained traction. However, to determine whether building one in your backyard makes investment sense means thinking through the complete picture properly, factoring in your personal financial situation and doing the all-important number crunching.

For starters, any comparison between a granny flat and an investment property must recognise that while the former is typically a yield play, the latter has greater capital growth potential.

Passive income for owner-occupiers

While it’s not investing per se, owner-occupiers who borrow more to build a granny flat could use the extra (rental) cash flow to reduce their non-deductible debt a lot earlier. The faster you pay down non-deductible debt, the sooner you can move forward financially, and for baby boomers this could mean passive retirement income.

If it costs you 5% to get a return of 10% plus, a granny flat can help you do this. It also helps mitigate risk if you’re planning to go from two incomes to one.

Based on a $120,000 investment, a 12% yield (about $300 in weekly rent) for a one-bedroom granny flat in a capital city looks highly achievable.

The risk of overcapitalising

Assuming you can command the yield you need, you need to honestly assess 1) why you’re attracted to a granny flat option, 2) whether you can achieve/maintain the necessary uplift in yield.

Similarly, if you’re an owner-occupier, ask yourself how comfortable you would be sharing your backyard with strangers.

It’s also important to remember that a granny flat may not be the best use of a backyard if your block has promising subdivision potential. While the granny flat won’t be worth much after 30 or 40 years, it’s the land value that will deliver future capital growth.

While a return of 12%-plus may look compelling, you also need to weigh up the risk of overcapitalising. For example, this could happen if a $100,000 granny flat – which you’ve borrowed against equity in your home to build – only achieves $50,000 in additional value.

Don’t create a backyard eyesore

Added further insult to a 50¢ return on every $1 invested, a clumsily conceived one-bedroom granny flat could also create an eyesore in the backyard. This eyesore could affect the resale potential of your quality four-bedroom home.

Assuming the original house is also tenanted, you could also have to reduce the rent if you’re suddenly taking away half of the backyard.

To avoid these outcomes, investors could contemplate buying a property with a granny flat or secondary dwelling that’s already been tastefully incorporated into it.

If you are considering a property with a granny flat, and looking for one on a corner block - where both dwellings have separate street access - might be the way to go.

Eyes wide open

Going into a granny flat investment with your eyes wide open means you have to be comfortable running a mini-business. When crunching the numbers with your accountant, it’s also important to recognise that market conditions can turn quickly.

As well as dealing with tenants, you should also allow for loss of income during vacancies, unexpected maintenance costs and the cost of hooking up the granny flat to the utilities.

Remember, if you’ve got $100,000 to spend on a granny flat, you could potentially generate a much better return by putting it towards an investment-grade property or asset.

New house vs Granny flat: tax considerations

While your granny flats will receive a depreciation deduction, you [as an investor] will also incur capital gains tax (CGT) when the property is sold, and this is one of many factors to consider.

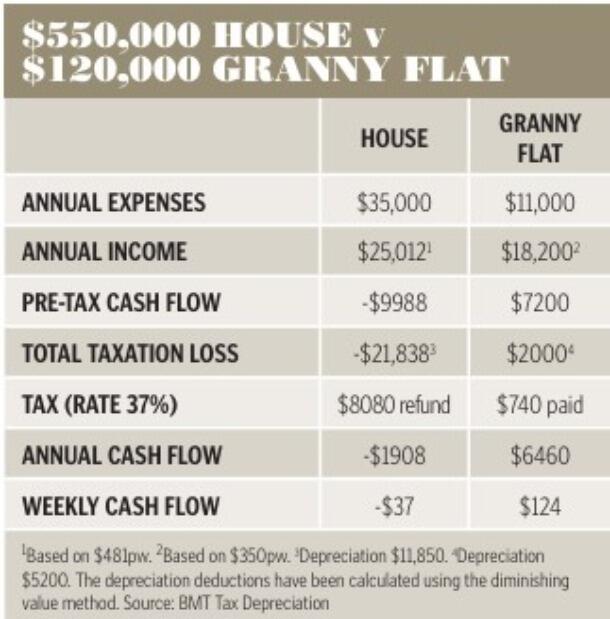

To illustrate how the numbers might work in practice, Azzet has constructed a real-life example that compares building a new house for $550,000 versus a granny flat for $120,000 on an existing property as an investment.

The investment house

Based on some preliminary research, within the area our fictitious investor is looking to buy, a new house will receive an annual income of $481 a week or $25,012 annually.

BMT Tax Depreciation estimates the expenses for the house, including interest on the loan, council rates, insurance, repairs and maintenance, at a total of $35,000 annually.

The granny flat

By comparison, the investor could expect to receive $350 a week in rent for a granny flat ($18,200 a year). As the borrowing amount on the granny flat is lower, estimated expenses for this property, based on BMT Tax Depreciation’s numbers, are expected to total $11,000 annually.

The investor will be able to claim around $11,850 in depreciation deductions for the house or $5200 for the granny flat.

The depreciation factor

It’s evident from the scenario that an investor’s tax situation will be quite different should they decide to build a granny flat compared with a new house.

In both scenarios, claiming depreciation will boost their weekly cash flow. By claiming depreciation on the house, the weekly cost of holding the property is reduced from $121 to $37.

In the granny flat scenario, the investor is able to reduce their taxable income and therefore the amount of tax they will need to pay on the property to just $740 for the year.

A weekly cash flow of $124 is therefore achieved for the granny flat. Based on these numbers, the investor will benefit from an additional $285 in cash flow by choosing to build a granny flat compared with a new house.

Cash Flow

In summary, the investor who opted for the new house is out of pocket $1908 annually, while the granny flat owner receives an after-tax cash flow of $6460 annually.

That’s a good outcome, but Bradley Beer CEO with BMT reminds investors that the capital growth on the future sale of the new house will invariably outperform the future sale of the property with the granny flat in the backyard.

Admittedly, depreciation will reach its maximum in the first five to seven years. But Beer also reminds investors that with deductions on structural elements continuing for 40 years, cash flow outcomes won’t change considerably.

But given that there are two sides to the cash flow recipe, it’s important to remember that while a granny flat on the right property in the right area will contribute to capital growth, the opposite is also true.

On the wrong property you could potentially be cutting out a percentage of your future market when it comes to selling and if you rely on depreciation to support this cash flow, you’re also rolling the dice if future tax laws change.

That’s why you should always do your numbers on a cash-in or cash-out basis, in before-tax dollars, and allowing for a vacancy rate of 20% is also a good idea.

What a granny flat looks like

Despite jurisdictional nuances, granny flats, regardless of location typically have the same basic requirements:

A) Separate entrance.

B) Own bathroom, kitchen, bedroom/s, laundry area and living space.

C) Built on a property zoned for residential use and at least 450 square metres in size.

D) The only granny flat on the property.

E) Owned by the same person who owns the primary dwelling.

F) A maximum living space of around 60 square metres.

G) Have separate and unobstructed pedestrian access.